Today the minutes of the April 27-28, 2023, Bank of Japan meeting were released. Below in italics are the top ten highlights generated by our AI engine.

- The Bank of Japan (BoJ) has been conducting purchases of various financial instruments and providing funds without setting an upper limit. This includes Japanese government bonds, ETFs, Japanese real estate investment trusts, CP, and corporate bonds.

- The pace of recovery in overseas economies has slowed, with the exception of China and Europe. The U.S. economy is on a slowing trend, and exports have slowed, particularly of IT-related goods.

- Japan’s economy has picked up and is expected to recover moderately by mid-2023. Despite the slowdown in overseas economies, exports and production are expected to return to an uptrend.

- Private consumption has increased moderately and is expected to continue increasing, supported by household savings. The employment and income situation has improved moderately.

- Japan’s financial conditions have been accommodative, with firms’ demand for funds rising moderately and issuance conditions for corporate bonds favorable.

- The Policy Board discussed the current economic situation and agreed that there are high uncertainties surrounding global inflationary pressure and the course of monetary policy in each economy.

- The Bank of Japan should continue to impose low-interest rates and monitor price and wage developments, but it should also consider whether households, firms, and financial institutions are well prepared to deal with future changes in interest rates.

- Members agreed that risks to economic activity and prices were balanced for fiscal 2023, but negative for fiscal 2025.

- The Bank of Japan decided to continue with large-scale JGB purchases and make nimble responses for each maturity by increasing the amount of JGB purchases and conducting fixed-rate purchase operations, and keeping 10-year JGB yields at around zero percent.

- The Bank of Japan has been implementing monetary easing measures to achieve price stability for 25 years but has decided to conduct a broad-perspective review of monetary policy.

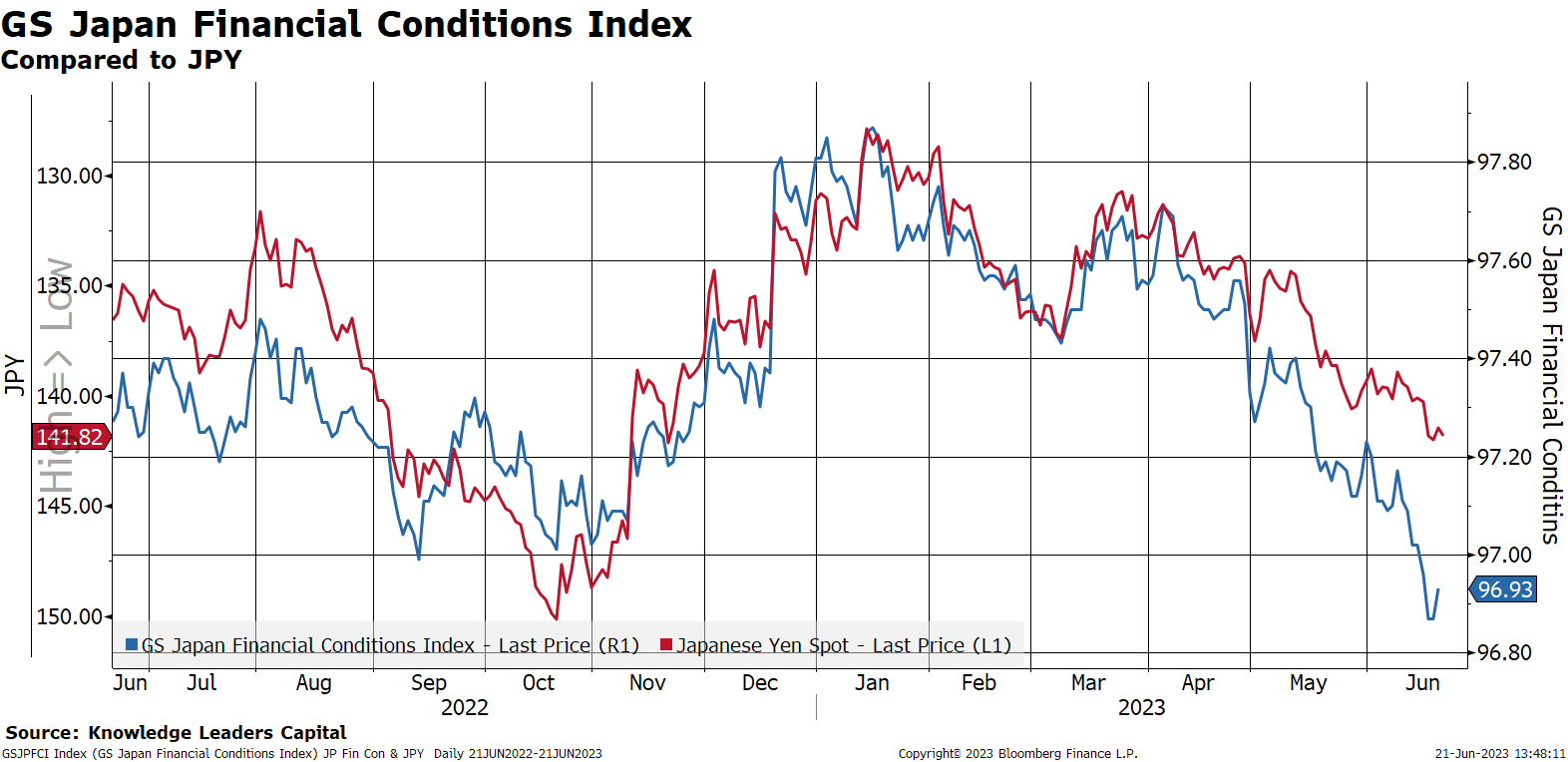

The net of the meeting suggests the BoJ sees every reason to continue with accommodative monetary policy. In anticipation of the release of these minutes, the JPY broke through 140, where it held for the last month.

This accommodation has served as a detriment to the value of the Yen. Current easy financial conditions suggest we may retest the 150 level on the Yen.

The saving grace for the Yen here may be item #10, where the BoJ states that it has decided to do a comprehensive review of its monetary policy. I think one can read this as Japan is thinking about abandoning yield curve control. Should traders begin to discount that prospect, the Yen could have a powerful reversal as Japanese citizens bring capital home.

According to a recent Nikkei Asia article, Japanese citizens engaged in 12 quadrillion Yen ($87.3 billion) in 2022, the highest level ever. “Mrs. Watanabe” accounts for 28% of global FX trading according to the article. Any change to BoJ policy that encourages capital to return home would seem to have a significant impact on global capital and FX markets. But for now, the BoJ continues to take it easy.

Disclosures

The information presented here is for informational purposes only and is not to be construed as an offer to sell, or the solicitation of an offer to buy securities. Some investments are not suitable for all investors, and there can be no assurance that any investment strategy will be successful. Hyperlinks may be included in this message that provides direct access to other internet resources, including websites. While we believe these links are to reliable sources, Knowledge Leaders Capital (“KLC”) has no control over the accuracy or content of information contained on these sites. Although we make every effort to ensure such links are accurate, up-to-date, and relevant, we have no control over pages maintained by external providers. The views expressed by these external providers on their own web pages or on external sites they link to are not necessarily those of Knowledge Leaders Capital.

The information provided on this blog is for illustrative or example purposes only and should not be construed as KLC’s opinion or investment outlook. As of the most recent quarter-end, the named companies may have been held by KLC. For full information including additional policies and full disclosures, please visit our website: KnowledgeLeadersCapital.com.

Any reference to Index performance does not represent the performance of any investment product offered by Knowledge Leaders Capital, LLC. An investor cannot invest directly in an index. The performance of the client account may vary from the Index performance. Index returns shown are not reflective of actual investor performance nor do they reflect fees and expenses applicable to investing.

Companies are selected for “Spotlights” based on high levels of innovation activities in their respective industries and illustrate innovation being employed across all sectors and geographies. Spotlight selection is separate from stock selection by the investment team. Spotlights are not necessarily representative of investment opportunities and can be selected regardless of investment performance or inclusion as a KLC holding.

A message from Advisor Perspectives and VettaFi: To learn more on this and other topics, check out our full schedule of upcoming CE-approved virtual events.

© Knowledge Leaders Capital

Read more commentaries by Knowledge Leaders Capital