Municipal Bonds, Powered by Tax-Exemption, Earn Renewed Appeal

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsThe high-quality nature of the municipal asset class often has investors overlooking munis for more volatile asset classes with higher return potential. As fixed income yields have reached near-decade highs, and as higher taxable fixed income rates, along with higher tax rates, have led to potentially larger tax implications associated with fixed income investing, we believe it is time to take a closer look at after-tax return potential afforded by the tax-exempt asset class.

Why Bonds? Fixed Income, Again Offering Income

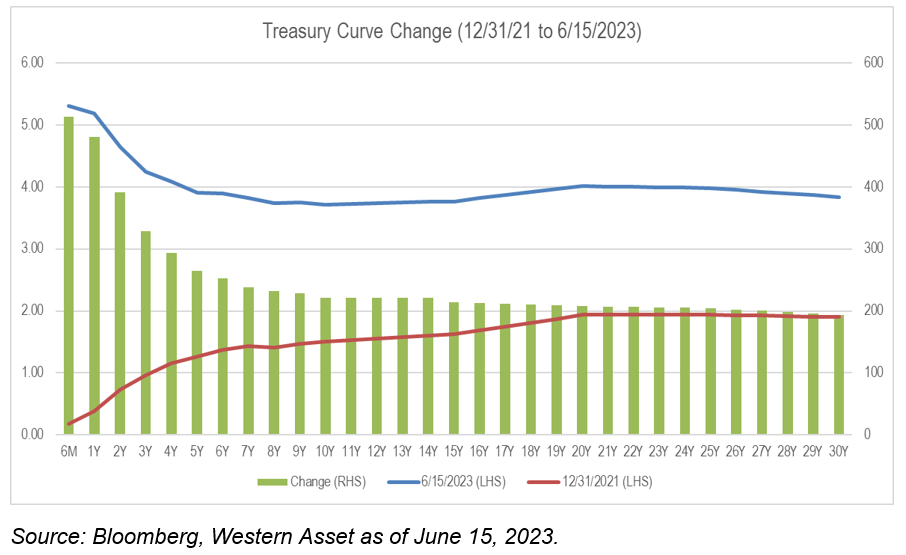

For the first time in a long time, fixed income is paying investors to diversify their asset allocations from more volatile asset classes. Yields have reached highs not seen in many years as central banks around the world raised interest rates over the past 18 months. With the U.S. Federal Reserve’s most recent decision on June 15 to forgo another rate hike, the fed funds rate remains at 5.00%-5.25%, up 5.00% from the start of 2022; it now stands at the highest level since September 2007, resulting in higher levels of income across the curve.

Why Munis? Above Average After-Tax Return Potential, with Downside Protection

As investors consider the long-term benefits of fixed income, munis shouldn’t be ignored in the conversation

The power of tax-exempt income can provide for after-tax return advantages. Considering a top effective marginal tax rate of 40.8%, which includes the top federal bracket of 37%, as well as a Medicare surcharge of 3.8%, this is almost half of the income generated by a taxable fixed income investment.

This tax burden can be even greater for individual states with high personal income taxes. Considering California and New York’s top rates of 13.3% and 10.3%, respectively, effective tax rates for top tax payers can exceed 50%. With certain provisions of the 2017 Tax Cuts and Jobs Act expiring in 2025, and election season around the corner, we expect tax rates could move higher and further increase the appeal of tax-efficient total returns offered by municipals.

With potentially over half of a taxable bond yield consumed by federal and perhaps even state taxes, for high taxpayers, it becomes very difficult for a comparable high-quality taxable fixed income security to offer the same appeal as munis. Since 2018, 10-year AAA rated munis offered 46 basis points (bps) of average yield pick-up versus after-tax Treasuries. Moving down the credit spectrum to comparable corporates, an index of A rated muni bonds offered a yield pick-up of 54 bps versus the index of A rated corporate bonds, and BBB munis offered an after-tax yield pick-up of 81 bps versus similar BBB corporates. As fixed income yields moved higher in sympathy with these Fed rate movements, so has the tax liability for those in top tax brackets in taxable instruments, which makes the muni tax exemption much more appealing.

Because the tax exemption becomes more valuable at higher rates, munis also offer relative downside protection during periods of rising rates as the magnitude of yield increases is typically less than that seen in comparable taxable asset classes. For every 100 bps of taxable yield increase, the municipal yield would only need to increase 59 bps to offer the same after-tax yield pick-up for someone in the top bracket. Because munis move higher at a lower rate in rising rate environments, the price decline associated with rate increases is lower, which drove outperformance of the asset class across a rising yield environment in 2022.

All told, the ability for municipals to perform on an after-tax basis in both strong and weak market conditions has led to favorable outcomes for investors. From 2009 to the present, a period which included market stresses associated with the so-called taper tantrum as well as the Puerto Rico and Detroit bankruptcies, the municipal market has delivered higher after-tax returns than other fixed income asset classes, typically with lower volatility.

More recently, despite the sharp economic turmoil of the past few years, which was bookended by the pandemic and subsequent inflation pressures, municipals have held their value proposition within a well-diversified portfolio, providing downside protection and diversification from equities while still providing tax-advantaged income opportunities. In fact, the average after-tax return of the asset class outpaced Treasuries and corporate bonds by more than 8% and 10%, respectively.

Why Now? There Are Three Reasons

- Decade-high yields bring new opportunities for those seeking increased income

With nominal yields at their highest level in a decade, we believe investors have a potentially fleeting opportunity to lock in long-term levels of tax-exempt income. Following the rate increases of the past year, the overall bond market has begun to find its footing since October as key inflation metrics moved lower. Although the Fed announced its rate pause on June 15, markets are still pricing in multiple potential cuts into 2024, meaning income seekers may want to consider acting.

As fixed income investors continue to lick their wounds from 2022, many are negotiating the decision to extend out into the intermediate-to-long maturities of an inverted yield curve, particularly when facing the decision of giving up the appeal of a 5% yielding ultra-short money market fund. If the Fed comes close to or meets its goal of reigning inflation, short-term yields again fall and the curve normalizes, then the opportunity to lock in attractive levels of tax-exempt income could fall to the wayside. From 2017 to 2020, we estimate income seekers bought over $300 billion of municipals at an average yield of 1.5%. With yields and income opportunities now more than double this level, we believe income seekers should consider moving out the curve before the opportunity slips away.

- Long-term supply and demand challenges could challenge future entry points

The supply and demand mechanics that have challenged income opportunities over the past decade are likely not going away.

From a supply perspective, long-term municipal supply could be harder to come by. While the Treasury and corporate bond markets have increased 225% and 65%, respectively, since the global financial crisis (GFC), according to the Securities Industry and Financial Markets Association (SIFMA), the municipal asset class has not grown materially, increasing just 5% in the intervening 14 years. We attribute this to the lack of growth associated with austerity measures following the GFC, rising pension liabilities and limited federal infrastructure incentives. Considering the political landscape, we do not see a major catalyst that would ignite recent lackluster new-issue supply, particularly in today’s higher rate environment.

Meanwhile, from a demand standpoint, demographic shifts should further improve the number of income seekers as the U.S. population ages. According to the U.S. Census Bureau, 10,000 Baby Boomers reach the age of 65 daily, with the full Baby Boomer generation expected to reach 65 by 2030. We expect demand for fixed income, along with the municipal asset class, to increase as these individuals shift their asset allocations to safer fixed income instruments in retirement.

- Strong quality getting stronger, despite economic headwinds

Muni bonds are issued by states, cities, counties and other governmental entities to fund their long-term capital projects, such as water treatment systems or public schools. As such, most issues have long benefited from monopolistic pricing power for essential services, which has contributed to relatively high credit quality. The average five-year municipal default rate since 2012 is 0.1%, according to Moody’s Investors Service in a study of U.S. municipal bond defaults and recoveries between 1970 and 2021. “In contrast, the average five-year global corporate default rate was 7.2% since 2012 and 6.8% since 1970,” Moody’s noted.

The resiliency of municipal credit quality was highlighted by pandemic volatility over the past three years. During the height of Covid, there were concerns about the fiscal stability of municipalities stemming from regional shutdowns and potential migration from metropolitan to rural areas. Despite these initial concerns, the federal government’s support of a strong labor market kept taxpayers paying income and property taxes, and state and local revenues climbed to record levels despite pandemic conditions.

While inflation was another notable credit concern, a strong consumer, along with rising goods prices, was supportive of sales tax collections. All told, according to Census state and local revenue estimates, 2022 state and local tax collections were up 29% from 2019 pre-pandemic levels. These greater-than-anticipated tax collections, in addition to direct federal stimulus measures, have provided record cash levels for state governments, which equaled a record 15% of state budgets, according to the Pew Research Center. In prior economic downturns and recessions, reserve balances supported municipal credit, and we expect these record cash levels to also be supportive of the downturn that may lie ahead over the foreseeable horizon.

Opportunity for Active Management: Concentrated Demand for a Fragmented Market Offers Pockets of Value

The municipal market – with its one million securities and 50,000 obligors – offers a plethora of opportunities for municipal investors across a variety of sectors and maturity structures. With such a large market, securities can be mispriced and relative value can be constantly assessed.

These value opportunities can be particularly appealing when there is concentrated demand for a certain vehicle or part of the muni market. Currently, considering investors’ flight to quality as well as concentrated demand in separately managed accounts, the highest-rated securities with maturities of 10 years or less don’t appear to offer much value relative to Treasuries with the same ratings and duration.

However, the after-tax relative yield pick-up less traveled down the credit spectrum is much more appealing. BBB municipal credits offer over 120 bps of excess yield versus corporates (which is about 50% of the five-year average). We believe successfully navigating this area requires an experienced active manager to assess the evolving macro and credit conditions. But, over time, long-term municipal investors could be rewarded with attractive risk-adjusted after-tax returns.

While economic uncertainty remains high, this may be the time for investors to rethink the role of muni bonds which, at higher yields, can offer more after-tax return potential in a variety of economic environments.

Sam Weitzman is a product specialist with Western Asset Management in New York. Western Asset Management is an asset management firm with over $400 billion in client assets.

A message from Advisor Perspectives and VettaFi: To learn more on this and other topics, check out our full schedule of upcoming CE-approved virtual events.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All