One of the most surprising things to come out of the first half of 2022 was the walloping fixed income investors received from bonds. The Bloomberg U.S. Aggregate Bond Index posted its worst 12-month return in its entire history, which caused many investors to shed exposures, particularly longer-term sectors.

Valuations help investors gauge the downside risk and upside potential in a stock or market. At the same time, assessing liquidity conditions, including technical analysis, defining short term trends help with investment timing and asset selection.

With central banks tightening aggressively to beat down inflation, growth is beginning to slow—and the risk of recession is ticking higher. Historically, creditworthiness has soured when growth slows. But instead of bracing for a wave of downgrades and defaults, we think income-seeking investors should embrace the high-yield corporate bond sector.

U.S. equities are seeing solid gains, as the bulls look to sustain the rise today after failing to do so yesterday.

Last month I advised abandoning stocks and bonds in favor of inflation-protected alternatives. That hasn’t worked out. I have not changed my mind. Interest rates will increase and cause losses in stock and bond markets.

If you were considering taking the family on a European vacation, now may be a good time, as the U.S. dollar and euro achieved parity this week for the first time in 20 years.

With investors wondering whether we are finally through the worst of the selloff, our latest Strategic Income outlook tries to answer the question, “Are we there yet?”

As if another inflation shock and earnings drama at big banks weren’t enough for stock investors, Friday brings a critical moment where many option traders must decide their next move on hedging.

For all the volatility whipsawing the US bond market, traders are showing increasing confidence that the alarm bells warning of a recession will only get louder.

Many of the participants in the short-term credit market use it as a place to deploy cash while waiting for higher risk opportunities.

While the situations in the U.S., Europe, and Japan are different, all three are paying the price for years of fiscal and monetary tomfoolery. Using monetary policy to ensure low-interest rates encouraged unproductive debt growth. As liabilities grew faster than GDP, their ability to service debt became harder without continually having to administer lower interest rates and more QE.

US inflation accelerated in June by more than forecast, underscoring relentless price pressures that will keep the Federal Reserve on track for another big interest-rate hike later this month.

In a continuation of the first quarter, stocks and bonds struggled to find any sort of traction in the second quarter, leading to one of the roughest six-month starts to a calendar year on record.

Though risks are rising, strong hiring and purchase activity suggest that the economy can keep growing.

If your digital currency is sitting on an exchange, is it really yours?

After one of the sharpest selloffs in history during the first half of 2022, yields in US fixed income have increased markedly. Learn how Bramshill maintained defensive positioning during this correction and is now poised to allocate to sectors with attractive yields and total return potential.

We believe index funds have immensely contributed to investors by permitting them to capture beta inexpensively.

US corporate bonds are posting one of their worst selloffs since the financial crisis and could deteriorate further if recession predictions prove accurate.

New research shows that screening for “green” environmental, social and governance (ESG) criteria has led to positive risk-adjusted returns for corporate bonds. High demand among investors for those bonds contributed to the outperformance, raising the question of whether it will be sustained.

Buying individual bonds takes more work but is usually worth it in the long run.

The primary benefits offered by municipal bonds are generally well known to investors.

For the better part of the last decade, interest rates have been near zero and leverage has driven asset prices higher.

As the latest report showed, predictions of the economy’s imminent demise have been greatly exaggerated.

Rough water is ahead, but equity markets may sail higher over the next 12 months...

Markets are slumping. Crypto has cratered. Yet one corner of the financial world continues to offer investors strong, low-risk returns: Humble I bonds.

A rally in risk assets this week is sending traders to some of the most speculative corners of the technology sector, where gains in beleaguered stocks are more than double those of Nasdaq 100’s advance.

Markets were exceptionally volatile during the first half of 2022, foreboding poor capital market returns. Here is a quick review of nine areas of heightened risks.

The bond market is weird, but it’s full of clues. We have 8.6% inflation, but the highest interest rates have gone recently is about 3.4%, meaning real rates were still negative to the tune of 5%. This is confusing to me and a lot of other people.

Why did the bond market make its latest swerve? In the current febrile environment, data that are generally regarded as distinctly second-tier can have a big impact.

Lao Tzu wrote, “A journey of a thousand miles begins with a single step.”

The Federal Reserve's pledge to curb inflation appears to have resonated with the market.

As an old saying states that statistics do not lie, but statisticians are darn liars.

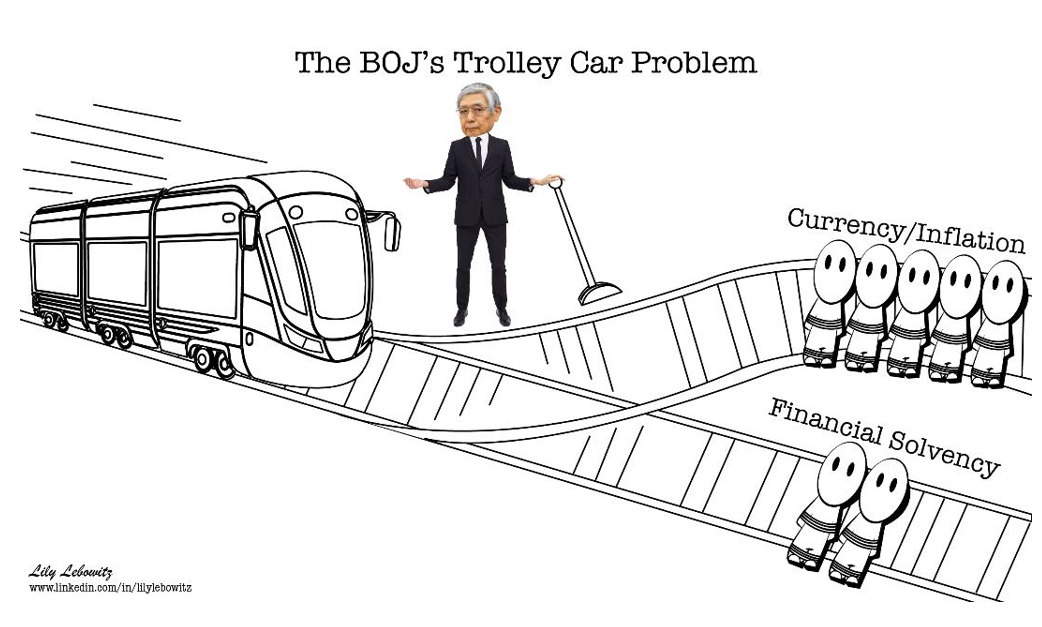

The trolley car problem is a well-known ethical question that forces one to choose between two poor consequences. For the Fed, it is whether to allow inflation to fester or to force the economy into a recession.

Week after week of on-the-fly calculations about the intensity of inflation and the likelihood of a recession are preventing markets from finding equilibrium.

Where can investors turn when the markets are a riddle? Raymond James CIO Larry Adam seeks advice from antiquity.

U.S. stocks are seeing pressure in early action following the long holiday weekend, with global recession concerns weighing on sentiment.

New research shows that the significant outperformance of ESG-driven investing over the last decade was due to a sharp increase in concern among investors for climate-related issues. Whether that outperformance continues will depend on even more heightened concerns over the environment.

Treasuries began the second half of the year on the front foot Friday as concerns continued to mount that Federal Reserve rate hikes will lead to a recession.

The first half of 2022 brought a brutal selloff to emerging markets, but also fueled hope for the second half: stocks, bonds and currencies have begun to outperform their peers in the US.

Things can only get better for the $4 trillion muni market in the second half of the year, according to Wall Street strategists.

No doubt about it, this has been a very challenging market environment to navigate, and we look to be in for more of the same. The Fed will continue to tighten monetary policy, and the longer the conflict in Ukraine persists, the longer we’ll likely feel the pressure from elevated gas prices.

In an inflation-lashed world where bonds are posting record losses, Wall Street issuers are betting investors hungry for income will instead lavish their millions on ETFs that ride stocks in order to deliver payouts.

The crypto investing front has taken another barrage of body blows, pushing Bitcoin to test the $19,000 per coin level once again.

It’s official: Chinese equities are once again in vogue, after months of regulatory crackdowns, deleveraging and stringent virus curbs wiped trillions of dollars off benchmark gauges.

Skeptics have long made a sport of predicting that the decade-long rally in technology stocks was destined to reverse. At the halfway point of 2022, it seems like this is the year when they will be proven right.

Now is the time to engage in risk management to retain your competitive advantage once the economy emerges from the slowdown.

A pair of exchange-traded funds that seek to capitalize on the tendency for US stocks to log the bulk of their gains when the cash market is shut are set to launch Tuesday.

The good news is that yields in US Treasury securities may be near their peak. The bad news is that makes the recession I’ve been forecasting since February more likely.

Recession fears and central-bank tightening are driving market volatility.

We examine key themes from our review of advisor fixed income portfolios over the past year.