Three Reasons It’s Time to Add High-Yield Bonds

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsBelow are three reasons high-yield bonds look attractive—and one reason to seize the day.

Reason 1: Strong long-term fundamentals.

When credit conditions tighten and demand slows, corporations can struggle to secure cheap and adequate funding. That struggle is a function of a company’s creditworthiness at the start of the slowdown: A company that’s already overstretched will run into problems very quickly when the spigot dries up.

At the brink of most slowdowns, corporate fundamentals are typically already weak. But today’s high-yield bond issuers are in much better shape financially than issuers entering past recessions, thanks in part to an extended period of uncertainty surrounding the coronavirus pandemic.

This uncertainty led companies to manage their balance sheets and liquidity conservatively over the past two years, even as profitability recovered. As a result, leverage and coverage ratios, margins, and free cash flow have improved. This relative strength in balance sheets means corporate issuers can withstand more pressure as growth and demand slow.

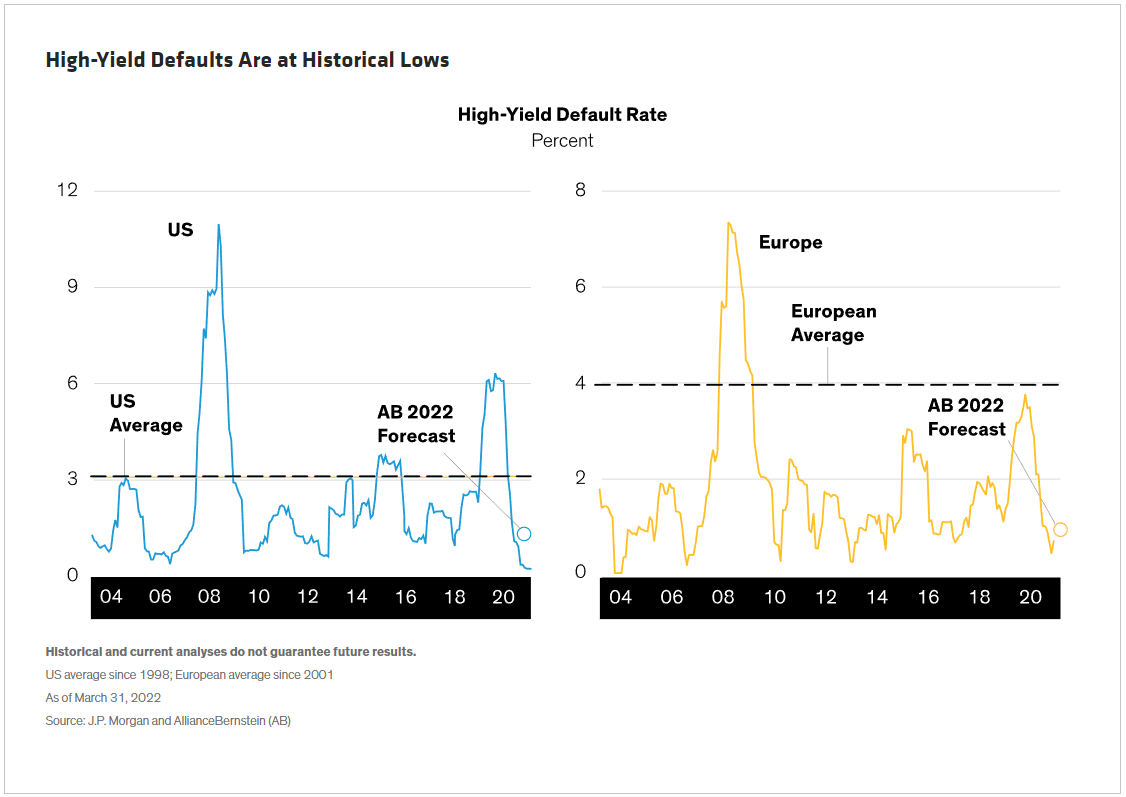

Prudent fiscal management isn’t the only reason the corporate universe is well positioned to weather a storm. The default cycle trigged by the pandemic—with defaults peaking at 6.3% in October 2020—effectively cleaned up the sector. The weakest companies at the time went ahead and defaulted and are now no longer part of the investable universe. The surviving companies were the strong ones.

That was less than two years ago, and since then, there simply hasn’t been enough time for the survivors to develop unhealthy financial habits. As a result, we expect the default rate to remain low for 2022—around 1% for Europe and 1% to 2% for the US—even if we tip into recession (Display).

The recent wave of defaults and downgrades also strengthened the quality of the high-yield market. At the same time that many of the lowest-rated high-yield bonds defaulted and fell out of indices, many of the lowest-rated investment-grade bonds fell into the high-yield market as fallen angels.

The recent wave of defaults and downgrades also strengthened the quality of the high-yield market. At the same time that many of the lowest-rated high-yield bonds defaulted and fell out of indices, many of the lowest-rated investment-grade bonds fell into the high-yield market as fallen angels.

Today, the quality of the high-yield market is the highest it’s been in more than a decade, with BB-rated bonds currently comprising 52% of the market, compared with an average of 46% over the past 10 years. There’s even scope for companies’ appetite for borrowing to fund mergers and acquisitions or increase returns to shareholders to grow, without impinging on ratings.

Reason 2: Extended maturity runways.

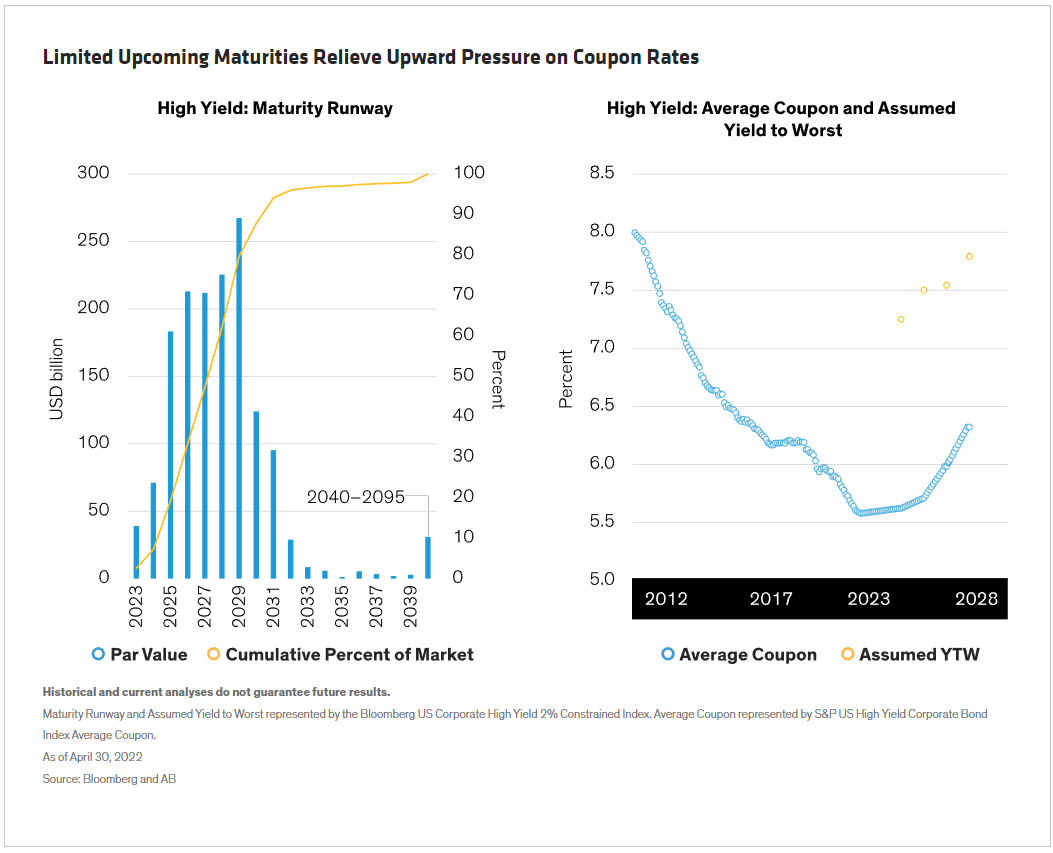

What’s more, companies have been focused on extending their maturity runways since the start of the pandemic. That means there’s no approaching maturity wall, where a large share of bond issues matures and issuers are compelled to procure new debt at prevailing rates. In fact, only 20% of the market will mature by the end of 2025, with the lion’s share of maturities coming between 2026 and 2029.

This is akin to opening a pressure valve as yields rise, because gradual and extended maturities will slow the impact of higher yields on companies (Display). Today, the average high-yield coupon is 5.7%—significantly lower than the current yield to worst. Even if we assume that yields continue to rise and remain high for the next four years, coupon rates won’t return to pre-COVID levels north of 6% until January 2026.

In other words, companies will enjoy low coupons for many years to come.

Reason 3: High yield that’s truly high.

High-yield valuations are far more compelling today than a few months ago, with yields and spreads at multi-year highs. Either the market is dramatically overestimating default risk, or—rather than being overly concerned about defaults—it’s demanding an elevated premium for elevated volatility. We think the latter is most likely because we expect continued elevated volatility too.

In this case, when market volatility declines from today’s levels, so too will spreads; conversely, if market volatility increases, spreads will likely widen. We expect high volatility to persist for an extended period, keeping spreads wide. In this environment, “carry”—essentially, clipping the bond’s coupon—rules the day.

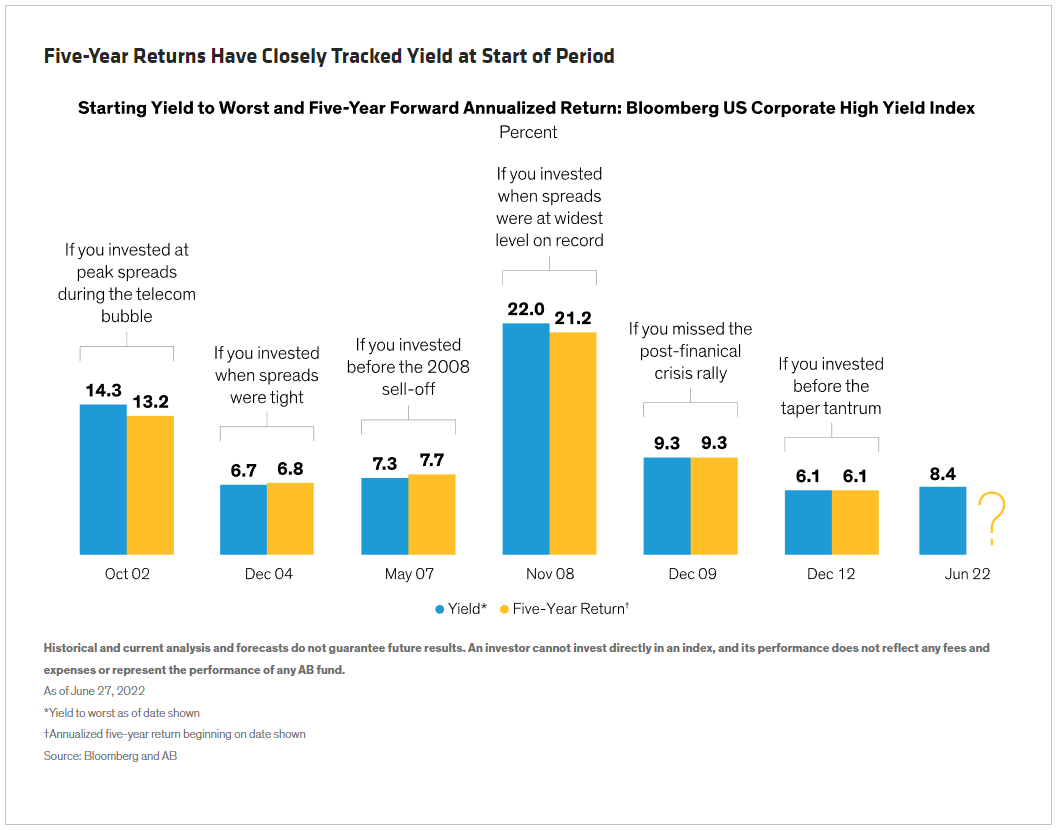

What’s more, history shows that the US high-yield sector’s yield to worst has been an excellent proxy for its return over the following five years. In fact, US high-yield bonds have performed predictably, even through rough markets (Display).

The relationship between yield to worst and future five-year returns held steady even during the global financial crisis, one of the most stressful periods of economic and market turmoil on record. If an investor had bought high yield in May 2007 at a yield to worst of 7.3% and held onto that investment for the next five years—riding out a 36% drawdown in the high-yield market—that investor would have earned 7.7% in total return on an annualized basis.

Why? High-yield bonds supply a consistent income stream that few other assets can match. And when high-yield issuers call their bonds before they mature, they pay bondholders a premium for the privilege. This helps compensate investors for losses suffered when some bonds default.

What does all this mean for today’s investors? High yield may experience some near-term volatility, but investors with a longer-term lens can ride out short-term drawdowns.

Bonus Reason: Opportunity Cost

Despite these favorable factors, many investors remain leery of jumping on the high-yield bandwagon while yields are still rising. But sitting on the sidelines can be a costly mistake. High yield is among the most resilient asset classes and tends to rebound quickly after downturns, thanks to its consistent, high income. On average, since 2000, high yield rebounded from peak-to-trough losses exceeding 5% in just five months.

And when it did rebound, it went big. Over the 12 months following such losses, the global high-yield market returned 26% on average, and the US high-yield market averaged a whopping 27%. Shy investors missed out.

That’s why, in our view, income-seeking investors should seize the opportunity to add high-yield bonds to their portfolios today.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All