What’s in a name? Sometimes, a lot. Economists often avoid using the term “recession,” preferring milder variants like “downturn,” “reset,” or “correction.” But the use of alternative terms doesn’t make the news any sweeter.

We have lately been inundated with questions and speculation about an imminent recession, or even one that is already underway. The combination of high prices, rising interest rates and falling markets are leaving many with a sinking feeling. But in our view, the expansion is still afloat and is likely to keep its head above the water line. This article will attempt to explain our point of view.

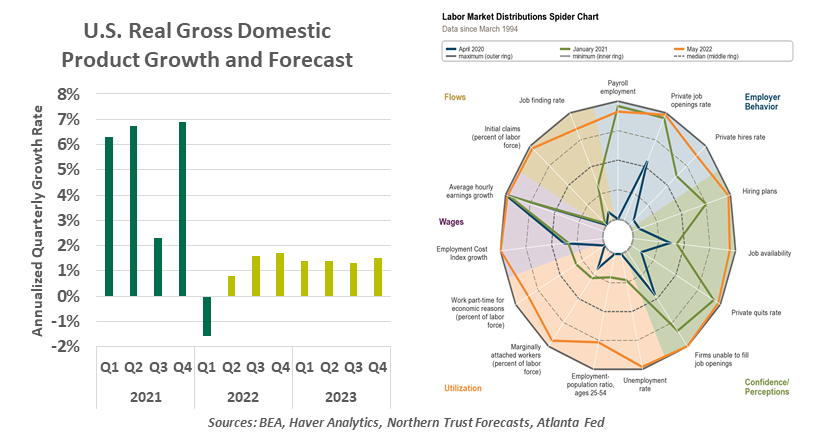

Recessions are informally understood to mean two quarters of economic contraction. U.S. real gross domestic product (GDP) fell during the first quarter of the year, and data for the second quarter suggest the possibility of a repeat performance.

But in the U.S., a group within the National Bureau of Economic Research (NBER) makes the official determination of when business cycles begin and end. The NBER evaluation is more nuanced, defining a recession as “a significant decline in economic activity that is spread across the economy and that lasts more than a few months.” Following are the indicators they focus on most intently during their deliberations, along with our thoughts on where things currently stand.

-

Employment: By nearly all measures, the labor market remains strong. Payrolls have grown continually since January 2021, and job openings stand at a level nearly double the number of unemployed workers. Labor force participation was slow to recover last year, but has improved in 2022, albeit unevenly. Some recent metrics, like job openings and managers’ hiring intentions, suggest this hot market may have started to cool, but only slightly.

Employment is especially important to track, as every recession has featured substantial job losses. Each Thursday, the Department of Labor reports on unemployment claims. Initial claims have moved up slightly from record lows seen earlier this year, but are still holding at low levels that were typical of the latter years of the prior growth cycle. The monthly unemployment rate will be crucial to judge a downturn: The Sahm Rule teaches us that a gain of a half-point in the three-month moving average unemployment rate is a highly reliable recession signal.

-

Industrial production: This measure of output in the manufacturing, mining and utility sectors shows a broad recovery, with the headline measure holding at a record high in the past two months. Despite labor and supply chain challenges, production has been robust. The Institute for Supply Management’s Purchasing Managers’ Index (PMI) has fallen but still shows expansion in the manufacturing sector.

|

The current strength of the job market is not consistent with recession.

|

-

Real manufacturing and trade sales: Retail, wholesale and manufacturing data are combined to track real purchasing activity. The index has held at an elevated level since 2021; though it has likely passed its peak, it shows more ongoing activity now than before COVID. Rebuilding depleted inventories will keep some momentum in wholesale trade, though a recent slowing of consumer spending suggests that final demand is falling while supply recovers.

-

Real personal income: Though nominal wages are growing, aggregate income has been flat this year, adjusted for inflation. Stimulus measures supported brisk income growth, and a flattening now is to be expected. Real personal consumption in May showed a similar cooling. Of the key measures that define recessions, this is the weakest link at present.

In sum, current indicators show growth has persisted. But the risk of weakening in the months ahead is certainly present. How can we tell if today’s malaise is evolving into a proper downturn?

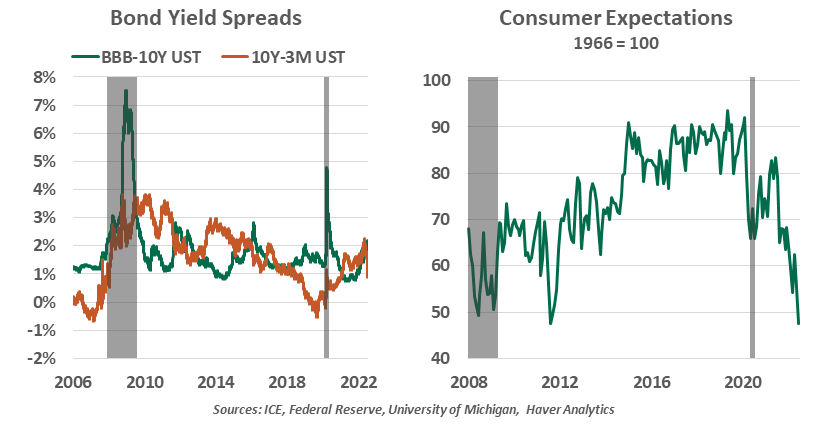

Bond markets can yield useful insights. Every past recession has included a widening of corporate bond spreads (the yield on bonds relative to risk-free government debt). Note that higher interest rates alone are not a sign of stress; they may actually suggest an economy performing above its potential. Thus far, investment-grade spreads have grown from their very low levels seen last year. While they do not yet indicate stress, a rising trend will be risk consideration.

We will also keep an eye on the spread of yields across tenors of U.S. sovereign debt. An inversion (higher yield on shorter-term debt than long-term bonds) can be a reliable recession signal when it is across the full yield curve. Thus far, 10-year notes have held a yield comfortably higher than the 3-month bill; however, if the Fed continues to hike aggressively, the short end could be pushed well above the long-end yield.

Worries come through clearly in consumer sentiment surveys. These can be noisy and are imperfect; for the past year, consumers’ assessment of current conditions has been falling, even during last year’s unambiguously thriving economy. Surveys also ask about consumers’ future economic expectations, and they are also gloomy. If the national mood does not improve, a recession could become a self-fulfilling prophecy.

|

If labor and activity measures hold their current levels, the economy can avoid contraction.

|

Stock markets have been a primary source of recession fear. Equity investors have had a difficult year, with losses reaching levels not seen in any first half since 1970. However, the stock market does not reflect the full economy, and equity drawdowns are not reliable recession indicators. Selloffs in 2011, 2015, 2016 and 2018 only set the stage for rallies to follow. Volatility has risen this year but is still within its historical norms. Similarly, high energy prices are an economic headwind, but the economy has grown through intervals of high costs in the past.

Today’s economy is still marked by high employment, continued spending and investment, and well-functioning financial markets. None of the past signals of recession are present, and yet, some appear ready to talk themselves (and the rest of us) into a contraction. They protest too much, wethinks.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2022 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.

© Northern Trust

Read more commentaries by Northern Trust