Inflation is currently the number one driver of equity markets. Its stickiness at high levels is weighing on consumer disposable income and corporate margins, along with complicating the Federal Reserve’s (Fed) situation as it attempts to bring inflation under control within a slowing economic backdrop. We believe that inflation has likely peaked (on a year-over-year basis) and can moderate over the back half of 2022 and into 2023, as the supply/demand imbalance for goods and labor normalizes. But the stakes are high, and investors have grown impatient with consecutive hiccups in inflation’s trajectory – i.e., the COVID-19 delta variant last fall, the omicron variant, the Russia/Ukraine war, and China COVID lockdowns.

The longer high inflation persists, the higher the odds that the Fed will need to overtighten monetary policy – potentially to the point of economic contraction – in order to bring inflation down. The degree to which inflation is able to moderate over the coming months should have a significant influence on the path ahead for the Fed, resulting in a wide range of potential equity market outcomes over the next six to twelve months.

Finding the bottom

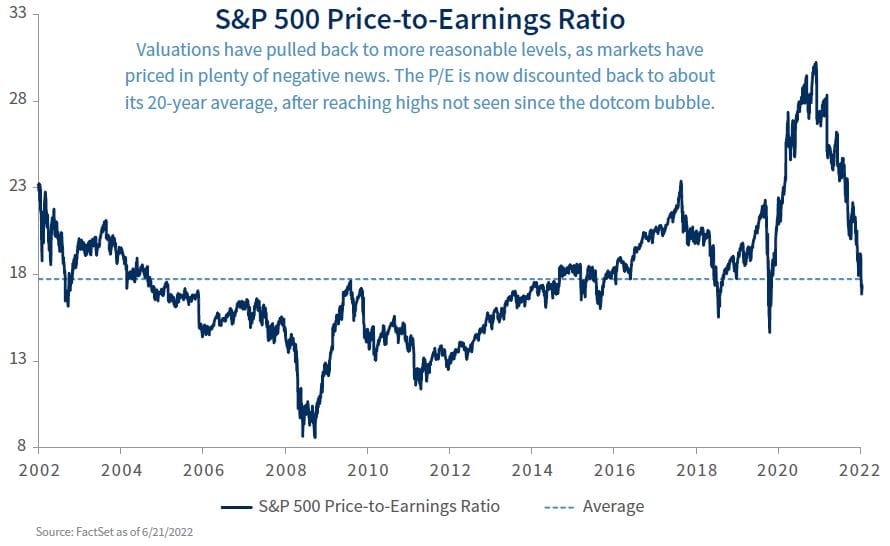

This elevated uncertainty is reflected in market volatility. At its recent lows, the S&P 500 had pulled back -23.6% from its early January highs. Whereas enormous stimulus through the pandemic fueled lofty valuation multiples, the Fed shrinking its balance sheet and swiftly hiking interest rates this year has resulted in valuations pulling back to more reasonable levels. Plenty of negative news is priced in at those valuations in our view, and the 39% P/E reduction is in line with that seen in bear markets historically. Investor sentiment has also gotten overly bearish, which often takes place near lows (contrarian indicator). However, numerous timing indicators we monitor, along with market internals in the relief rally, have not reached levels often consistent with durable lows. Unless Russia ceases aggression against Ukraine or China ends lockdowns, it will be difficult for equities to sustainably move to the upside without better inflation data in our view.

While we believe that the market may remain challenged with additional weakness in the coming weeks and months, we also believe equities will be higher over the next 12 months given our belief that inflation moderates as the year progresses. Thus, we recommend long-term investors use the market downdrafts as opportunities to accumulate high quality, favored stocks. The S&P 500 found a bottom at ~14 to 16x P/E during the last several severe market downturns (i.e., 2015/16 U.S. manufacturing recession, 2018 trade war, 2020 COVID shutdown).

Regardless of when or where equities ultimately find a bottom during the current volatility, we do not want to lose sight of the inevitable elongated rally we believe stocks will see on the other side of the current weak trend. Timing is difficult in bear markets with equities often bottoming before the negative headlines; and, when sentiment and positioning become "washed out," the rallies can be very sharp. On average, the S&P 500 has gained roughly 15% in the first 30 days out of bear markets historically. Diversification is paramount in weak trends, as is finding the right balance of ‘defense’ for the current trend and opportunity for the eventual recovery.

Positioning amid volatility

Market weakness has been most acute in the higher-valuation growth style, whereas value has held up relatively well. This is a good example of managing the present, while keeping an eye on opportunity within portfolios. Value is likely to outperform if the current weak trend persists, but growth could also see the sharpest rally in the eventual recovery. This bear market is likely to end with convincing improvement in inflation, which is likely to correspond with a moderation in bond yields – in turn removing the headwind on growth valuation multiples. So, while we would continue to tilt portfolios in favor of value for now, we recommend using the downdrafts as opportunity to accumulate growth – increasing our conviction once momentum builds and/or the economic picture improves.

We believe small-cap equities are another area likely to provide opportunity in a recovery. If the economy moves into recession, and the market moves to new lows, small caps are likely to underperform. However, small caps are likely to outperform on the other side of this bear market as well. For now, we lean toward large-cap equities but look to accumulate small caps when opportunity presents itself.

Within sectors, there are clear winners and laggards in the current environment. Energy is the clear leader right now – buoyed by high oil prices and capital discipline, resulting in strong fundamentals. The more defensive sectors such as utilities have also held up relatively well through the market’s volatility. While these groups may continue to outperform the longer market weakness persists, they are unlikely to outperform when the economic backdrop improves. On the flip side, the consumer discretionary sector has come under intense pressure with high energy prices and input costs weighing on margins. Additionally, sharply higher interest rates have weighed on technology’s high valuations, though fundamental trends remain solid. Finding the right portfolio balance is important for managing the current environment.

At the stock level, valuation has become more compelling across sectors. We see plenty of companies trading near or below pre-COVID prices, while earnings are significantly above early 2020 levels – resulting in attractive valuations, particularly for companies with stable or improving fundamental outlooks. Valuation can be a poor timing indicator, but it matters for potential returns over the long term, presenting a more favorable setup once the dust settles on this bear market. And while these stocks can get cheaper before the downside pressure abates, earnings often win out over the long term.

The tide will turn

In sum, we believe it will be difficult for the market to move sustainably higher without an improvement in inflation. We do believe that inflation will moderate over the next six to twelve months, and that equities will be higher than current levels over the next year. But this progress is unlikely to occur quickly, and stocks may ultimately need to move lower before all is said and done. The trajectory of inflation will remain a large influence on Fed policy and the economy, in turn being a key impact on equity market trends moving forward. With that said (and given the S&P 500 is already down 24% from its highs), we believe investors should manage the current environment with an eye on opportunity for the other side of this bear market. We recommend long-term investors use the market downdrafts as opportunities to accumulate favored areas – increasing conviction as inflation and/or technical momentum improves.

All expressions of opinion reflect the judgment the author, the Investment Strategy Committee, or the Chief Investment Office and are subject to change. Past performance may not be indicative of future results. There is no assurance any of the trends mentioned will continue or forecasts will occur. The performance mentioned does not include fees and charges which would reduce an investor’s return. Dividends are not guaranteed and will fluctuate. Investing involves risk including the possible loss of capital. Asset allocation and diversification do not guarantee a profit nor protect against loss. Investing in certain sectors may involve additional risks and may not be appropriate for all investors. The indexes mentioned are unmanaged and an investment cannot be made directly into them. The S&P 500 is an unmanaged index of 500 widely held securities.

© Raymond James

Read more commentaries by Raymond James