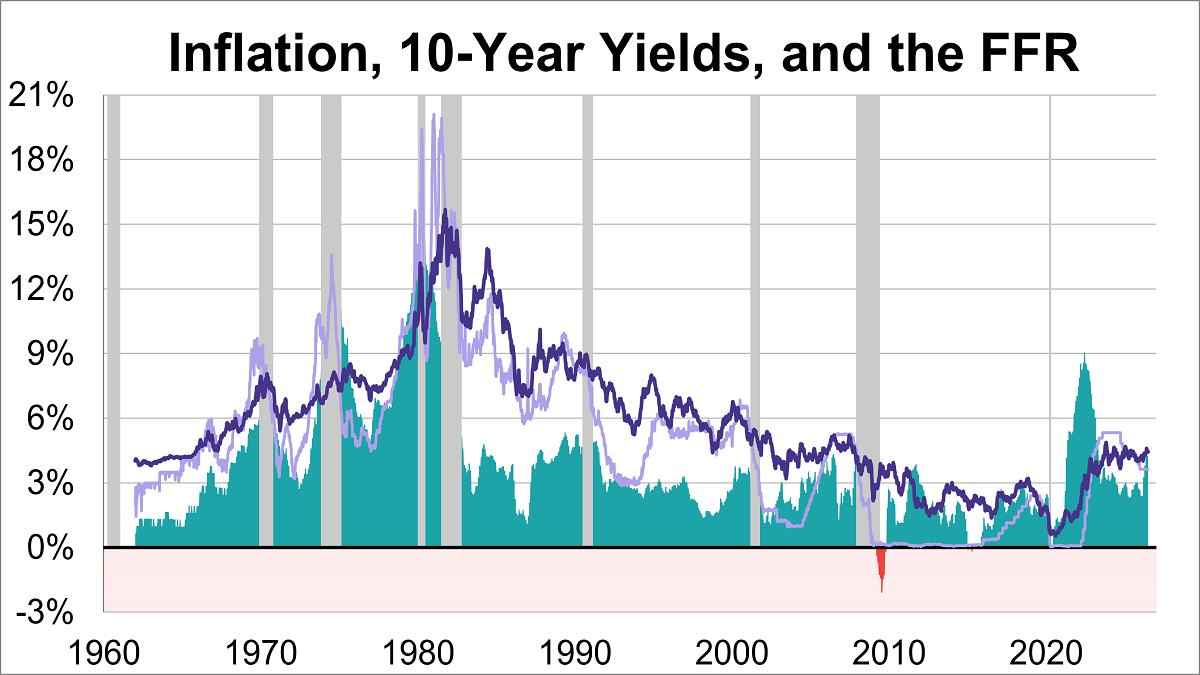

The 10-year Treasury yield has experienced dramatic fluctuations, ranging from a peak of 15.68% in October 1981, during the height of the Volcker era, to a historic low of 0.55% in August 2020, amidst the economic uncertainty of the pandemic. At the end of June 2026, the weekly average stood at 4.44%.

As growth stumbled, the S&P 500 Momentum Index captures a 7.5% gain in June and a 44% gain in the second quarter.

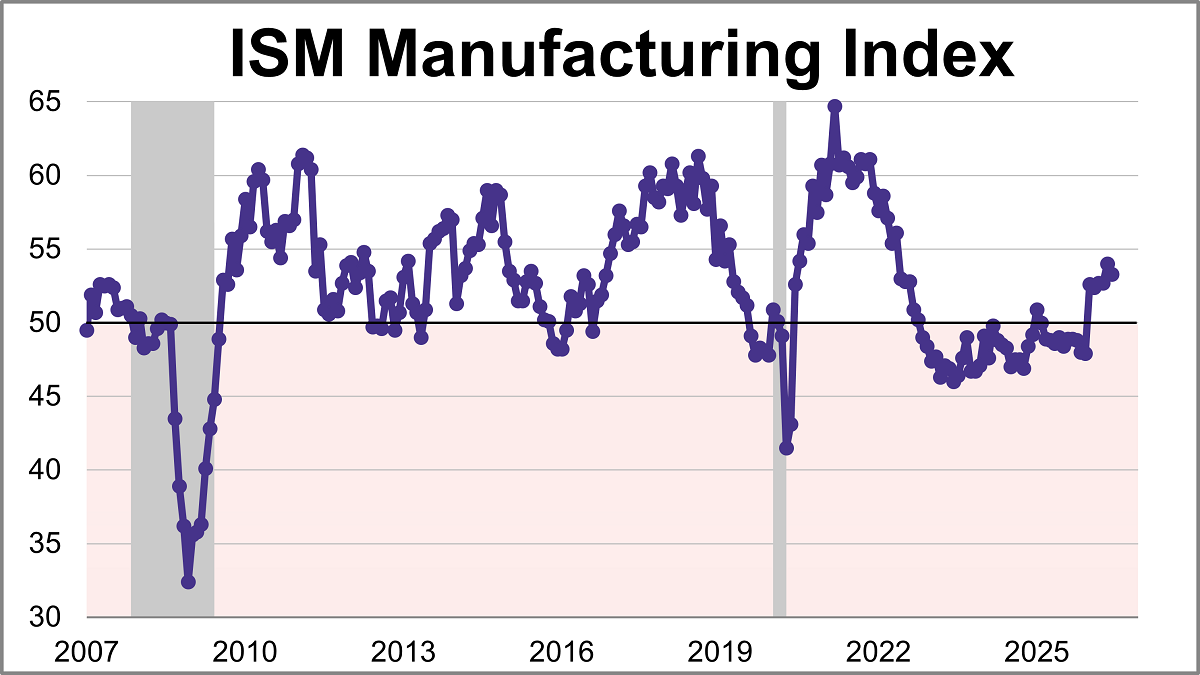

The Institute for Supply Management (ISM) manufacturing purchasing managers index (PMI) came in at 53.3 in June, down from 54.0 in May, marking slightly slower growth. The latest reading was just below the 53.8 forecast and is the index's sixth straight month in expansion territory.

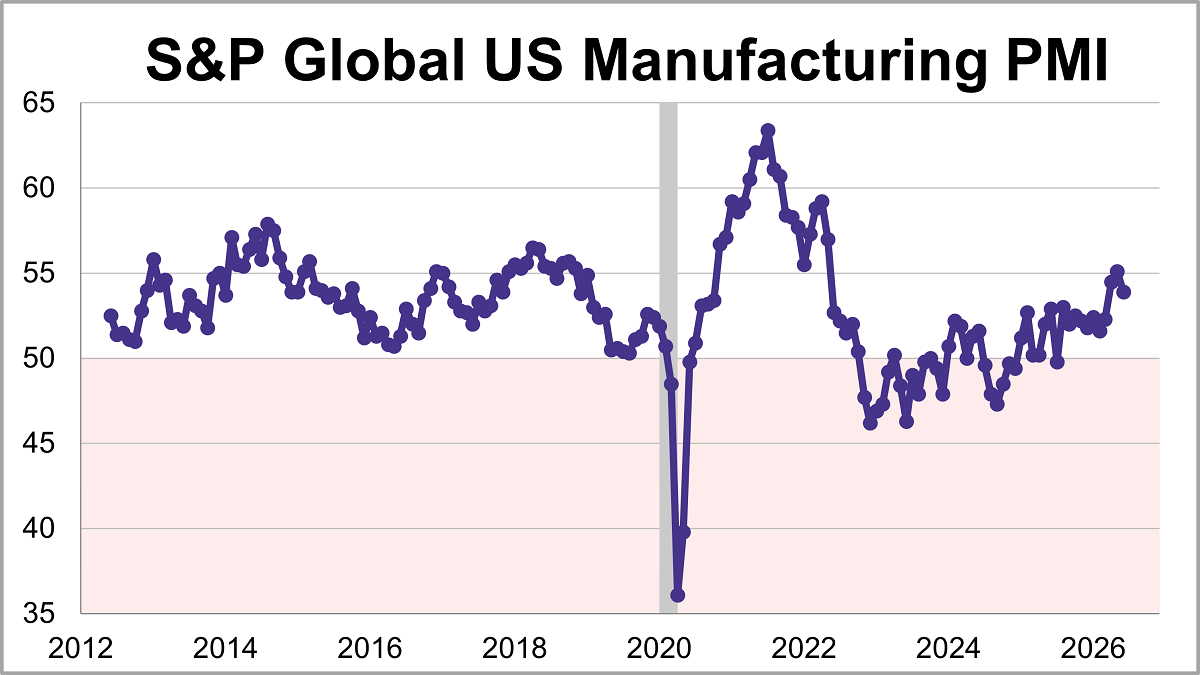

U.S. manufacturing expanded for an eleventh straight month in June but the growth eased to its lowest level in three months. The S&P Global PMI fell 1.2 points to 53.9 last month, falling short of the 55.7 forecast.

The firms that operate rigorous vendor evaluation will compound two advantages simultaneously: They buy the right tools now, and their advisors trust them when the next generation of AI arrives. In a decade that will be defined by the industry's capacity to do more with fewer people, that trust is a strategic asset.

July is a great time to buy stocks. In fact, it’s been the best month for the S&P 500 Index in the past two decades. Bulls are finding comfort in that history ahead of what stands to be an eventful stretch.

At the start of the regional war in February, Wall Street banks were grappling with the prospect of a protracted slowdown in the Middle East. Three months in, many firms are rushing to add bankers after local investors largely looked past the conflict and doubled down on dealmaking.

A strong quarter across major indexes. The second quarter is winding down and what a quarter it has been with the S&P 500 up 12.6% quarter to date, while the Nasdaq-100 and Russell 2000 are both up over 20%. Despite some twists and turns, the path of least resistance for stocks broadly remained up and to the right for much of the last three months.

Benchmarks are broken. That was the premise established in a conversation with Samarth Sanghavi, head of fixed income index product at TMX VettaFi, when the problem was first addressed in a previous article. TMX VettaFi creates innovative index solutions, and with the premise established that benchmarks are indeed broken, here is the fix.

The US Securities and Exchange Commission is signaling a potential rethink of how it oversees exchange-traded funds after a recent wave of filings for prediction-market ETFs prompted fresh scrutiny of the existing regulatory framework.

For decades, financial advisors have built strong relationships by helping clients manage IRAs, taxable accounts, and rollover assets after they leave an employer. Meanwhile, a significant, often the largest pool, of client wealth has quietly remained out of reach: assets inside workplace retirement plans.

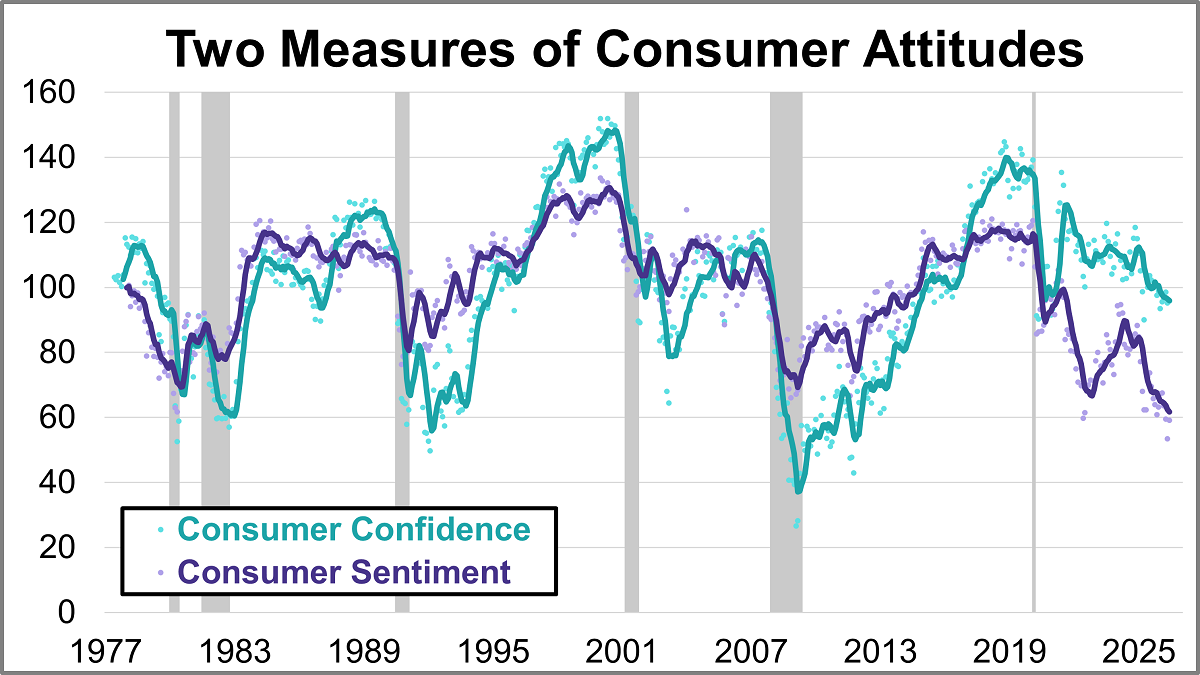

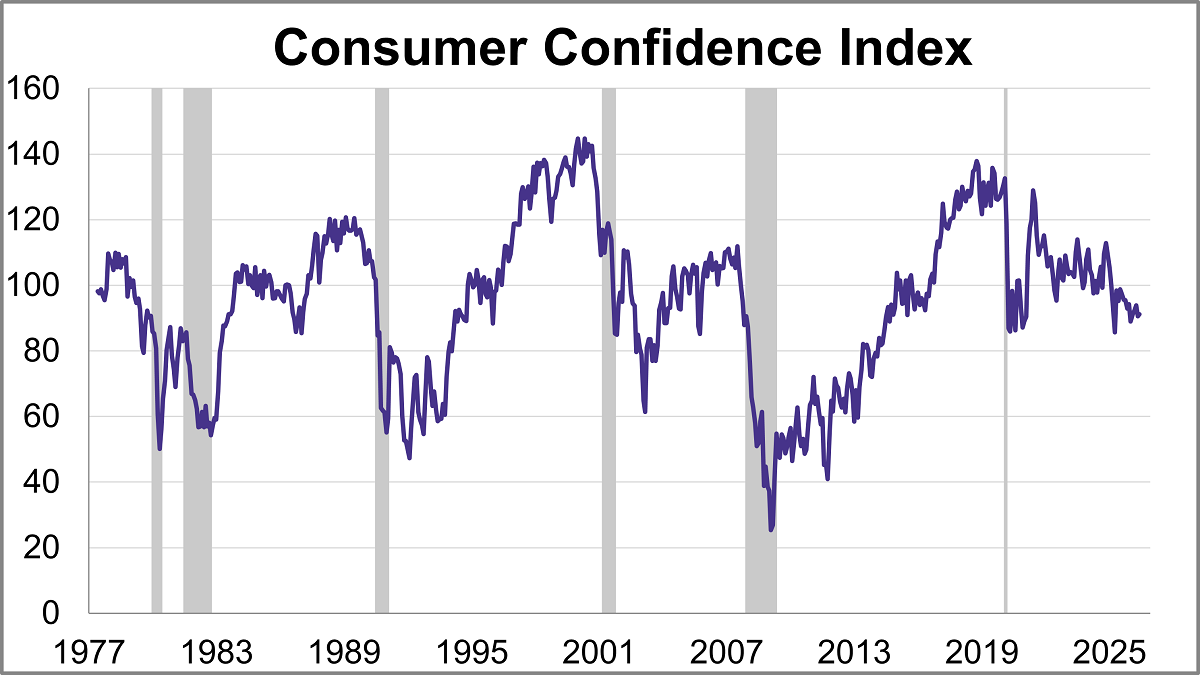

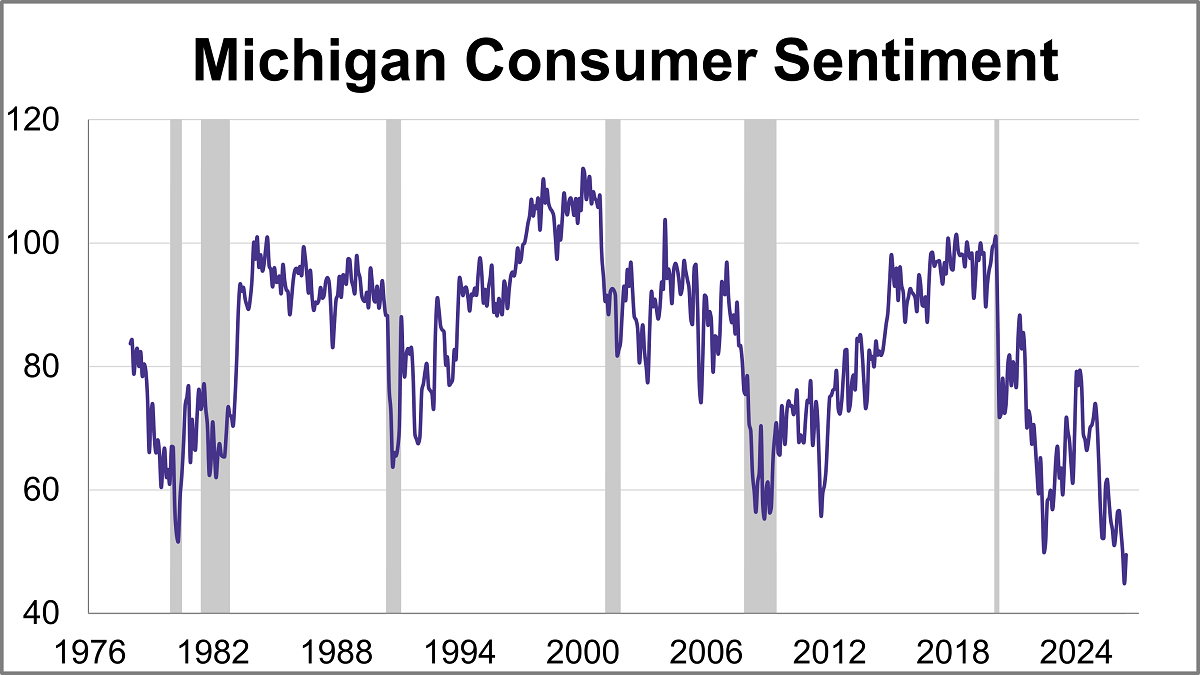

What are consumers thinking about the economy? Their collective mood offers crucial clues for businesses, investors, and policymakers alike. In June, the two leading benchmarks, the University of Michigan’s Consumer Sentiment Index (MCSI) and the Conference Board’s Consumer Confidence Index (CCI), offered similar views with both showing slight improvement despite ongoing inflation concerns.

The OBBBA created something the industry rarely gets: a defined planning window without a hard deadline attached. Exemptions are historically high, the law has no sunset, and there's a real body of existing work that needs revisiting. The advisors who treat this as an opportunity, rather than waiting for a client to ask, will drive much stronger outcomes compared to those who don’t.

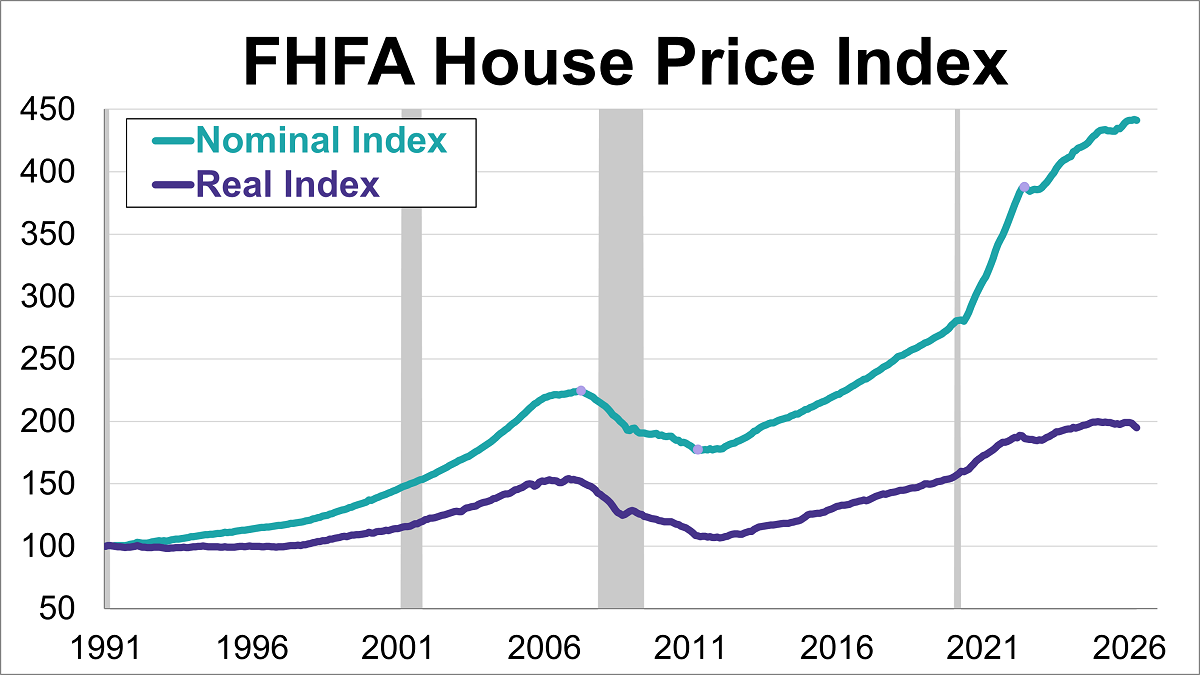

The Federal Housing Finance Agency (FHFA) House Price Index (HPI) retreated in April, falling 0.1% from the previous month's record high to 441.4.

The Conference Board's Consumer Confidence Index® inched up in June, rising 0.6 points to 91.2. Despite the improvement, the index came in below the forecast of 94.4.

These are dark days for free-market economists when one of the few areas of bipartisan consensus is for a terrible idea: Both Vice President JD Vance and Senator Bernie Sanders want the federal government to take an explicit stake in AI firms.

The ETF ecosystem is always changing and growing. Thanks to the ETF’s flexibility, transparency, and tradability, it can help investors achieve plenty of bespoke goals. That even includes investing with an eye towards philanthropic causes as with philanthropic ETFs ASD and DUTY.

Oil headed for the biggest quarterly decline since the pandemic as flows through the Strait of Hormuz accelerated following progress on a peace deal, with Morgan Stanley warning of a potential glut ahead.

Chip stocks are heading for their best quarter ever, extending an extraordinary start to the year driven by insatiable demand for artificial intelligence equipment. But after recent jitters sent the stocks tumbling, investors are wondering how much further the rally can go.

A sharp rise in the dollar may emerge as one of the biggest “pain trades” in the second half of the year, according to HSBC Holdings Plc.

Meme mania swept through Wall Street in 2021. Retail investors gathered on social media and coordinated trading strategies to short squeeze high-profile hedge funds.

The money is REAL. The question was never whether it exists. It’s who’s spending it, and what they borrowed to do it. When the wall of cash and the bottom half finally commit to risk at the same moment the Fed turns hawkish, that’s not the start of something. That’s the part of the cycle where the careful investor gets paid to be careful.

Ten years ago this week, the world watched the United Kingdom vote to walk away from the European Union. While the political class was clutching its pearls and every talking head on television was promising Armageddon by Christmas, I told you something different.

Chris Galipeau discusses high-conviction insights that go beyond media headlines.

What has started to stand out more recently is not the opportunity itself, but the behavior forming around it. The conversation has shifted. It is no longer centered on understanding what is being built or how it will be monetized over time.

The top 10 active ETFs YTD by fund flows show some intriguing trends and successful names that may pique the interest.

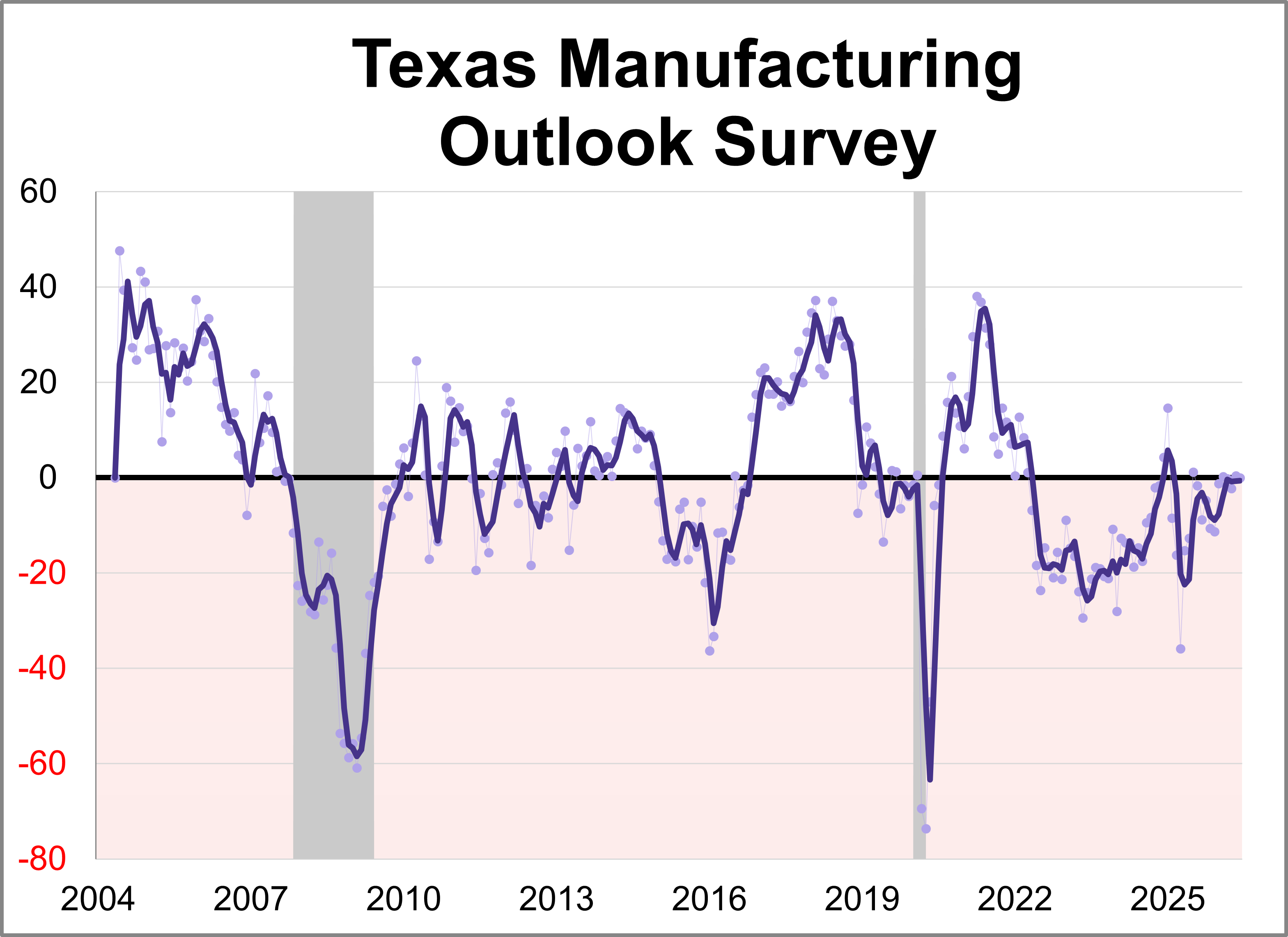

The Dallas Fed released its Texas Manufacturing Outlook Survey (TMOS) for June. The general business activity index fell 0.4 points to 0.0, indicating slower growth of manufacturing activity and stable business conditions perceptions.

Microsoft Corp. shares are heading for their worst month in years as investors continue to fret about how the software giant will fare in a world marked by artificial intelligence.

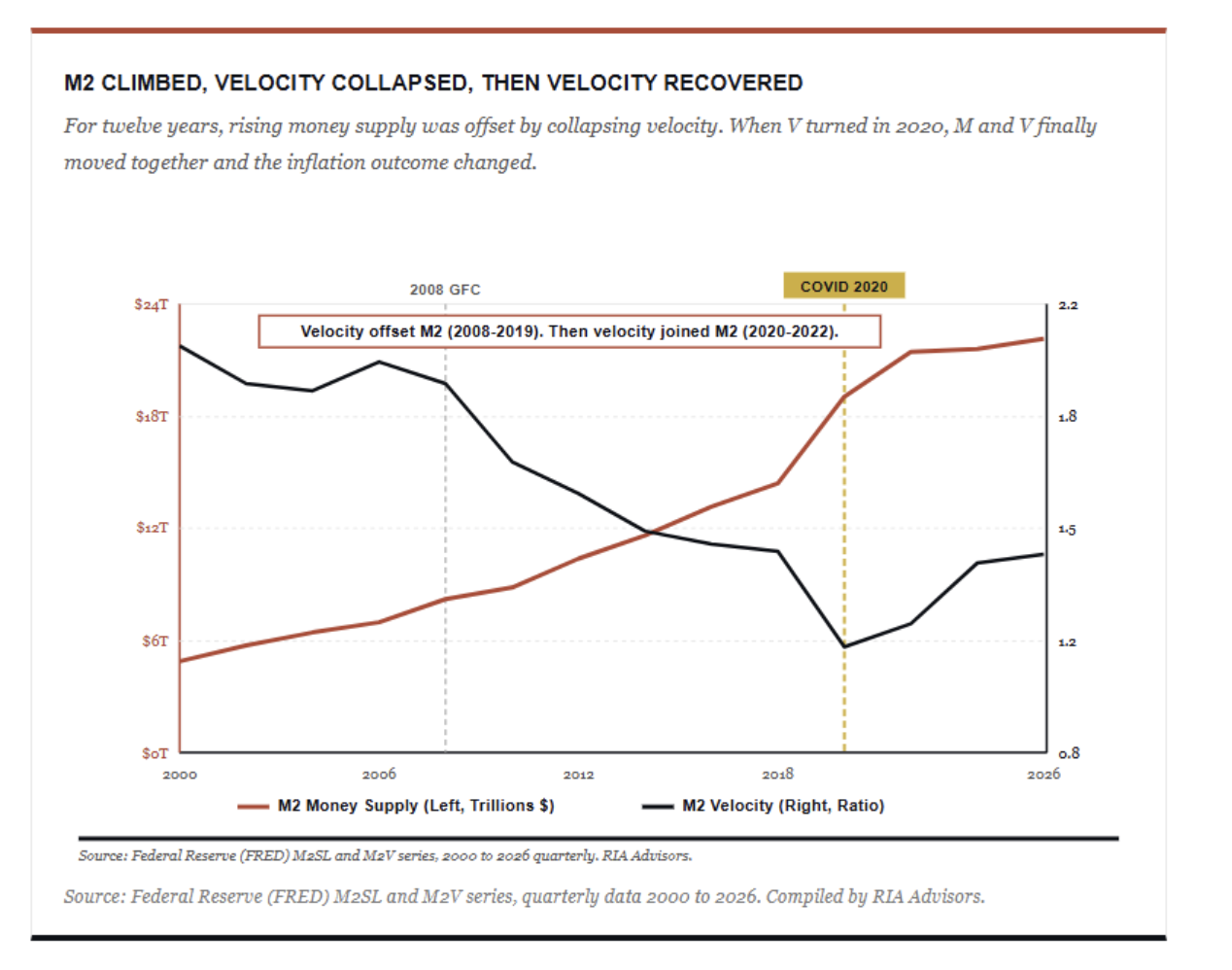

Friedman was reasoning from the equation of exchange, MV = PQ. Money times velocity equals prices times real output. It’s an identity, not a theory. Where it gets interesting is when you ask which variable does the work.

Markets have been hyper-focused on AI, crypto and buffer ETFs, but REIT ETFs have quietly staged an impressive comeback. The REIT terrain has shifted rapidly over recent years, and forward-looking investors and advisors have taken notice.

During the past month, the ETF market has seen a wave of excitement surrounding a concentrated group of companies. While investors still want exposure to the tech giants that have dominated the past few years, the successful launch of SpaceX in early June created widespread anticipation for planned IPOs like Anthropic and OpenAI.

Last week’s data reaffirmed that inflation pressures remain the defining narrative across the economic landscape.

Before your firm starts using AI across operations, client service, reporting, or advisor workflows, there’s one basic question leadership needs to answer: what kind of AI are we talking about?

Investors now have more optionality when looking for Nasdaq 100 exposure. State Street Investment Management (SSIM) just launched the State Street SPDR Portfolio Nasdaq 100 ETF (QNDX). It will invariably go heads up with the Qs, namely the Invesco QQQ ETF (QQQ) and the Invesco NASDAQ 100 ETF (QQQM).

GraniteShares and VettaFi are coming together for a state-of-the-category briefing: the flow data behind the surge, the structural reasons advisors are making room in income sleeves, how the category has held up across different rate and volatility regimes, and the diligence questions worth asking before adding it to a model.

Consumer sentiment improved for the first time in four months as gas prices eased but remains historically low amid ongoing inflation concerns. The final June reading for the University of Michigan Consumer Sentiment Index came in at 49.5 marking a 10.5% (4.7 points) increase from April and beating the expected reading of 48.9.

This roller-coaster week for tech stocks from Seoul to New York fueled by extreme investor positioning and worries over chip demand is sending a strong signal: the case for the artificial-intelligence trade is still strong, but the days of everything going up in a straight line appear to be over.

The dollar is wrapping up one of its best months in a year as a raft of Wall Street banks see a turnaround of fortunes for the US currency.

Bitcoin’s collapse is forcing crypto veterans to confront the question every bear market eventually asks: when does mass panic create a buying opportunity? The answer, according to many of the investors and analysts who have lived through previous boom-and-bust cycles, is: not yet.

Private credit is having a moment in the headlines. Higher interest rates and a pullback in certain types of bank lending have pushed more financing activity into private markets. Investors may be left with a simple question: What exactly is private credit?

AI is both a foundational technology and the ultimate replacement product, which we believe explains why it has attracted unprecedented levels of capital and why the investment opportunities are so compelling.

New Fed Chair Kevin Warsh is already reshaping policy communication by reducing forward guidance, questioning the dot plot’s future and emphasizing real-time data, potentially increasing Treasury market volatility.

Halfway through 2026, this market perspective is harder to write with confidence than most. That’s not a phrase I use lightly. Over four decades of markets, there have been plenty of uncertain moments, but the number of significant, unresolved issues I’m watching right now is unusually high.

The ETF landscape includes plenty of exciting ETFs. Not all, however, can claim to combine high current income and outperformance. The ProShares Russell 2000 High Income ETF (ITWO) has done just that so far this year with its innovative approach to covered calls.

VettaFi currently has index products tied to ETFs issued by American Century, Victory Capital, and ALPS ETFs, but the addition of RAFI products issued by Invesco and PIMCO that are fundamentally weighted is really exciting, according to Rosenbluth.

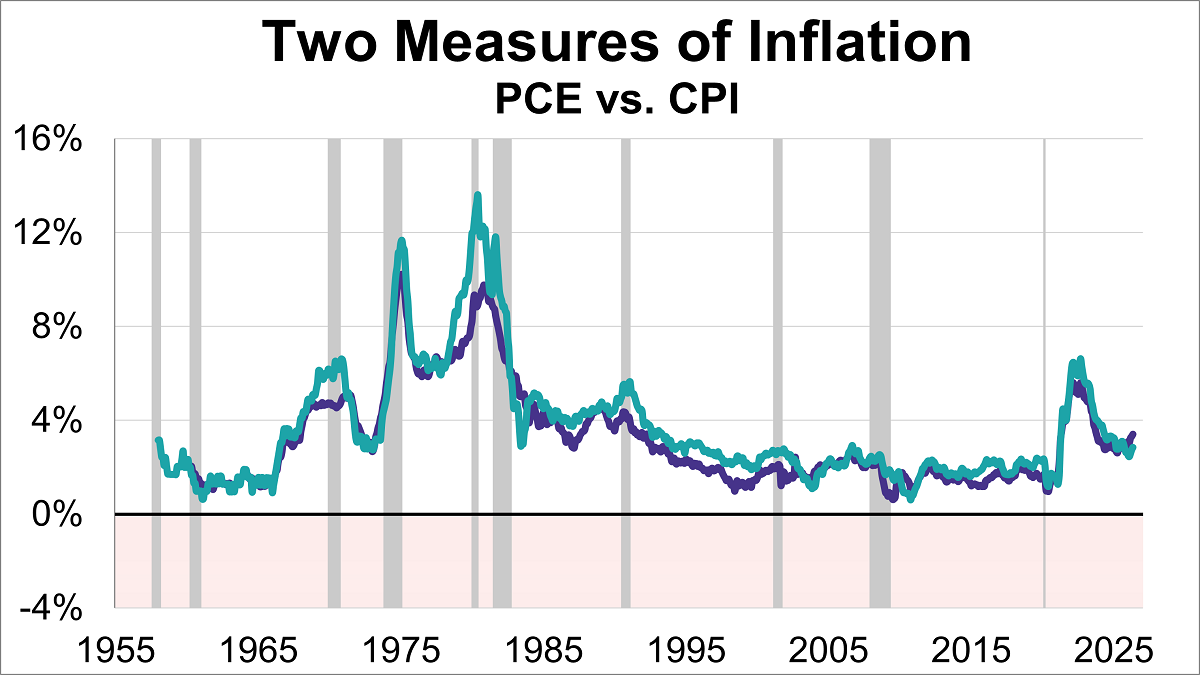

Inflation remains a hot topic, directly impacting everything from your grocery bill to interest rates. As of the latest data, two key inflation gauges — the Personal Consumption Expenditures (PCE) Price Index and the Consumer Price Index (CPI) — show that prices are still above the Federal Reserve's 2% target, with the core PCE at 3.4% and core CPI at 2.9%.

What if the debt crisis investors have feared is not still ahead, but already here, unfolding in plain sight? In his June insight, Richard Bernstein, Global Head of Macro & Customized Investing, makes the case that the market may already be penalizing U.S. fiscal excess, not through a dramatic collapse, but through a slow burn with real consequences for investors and the broader economy.

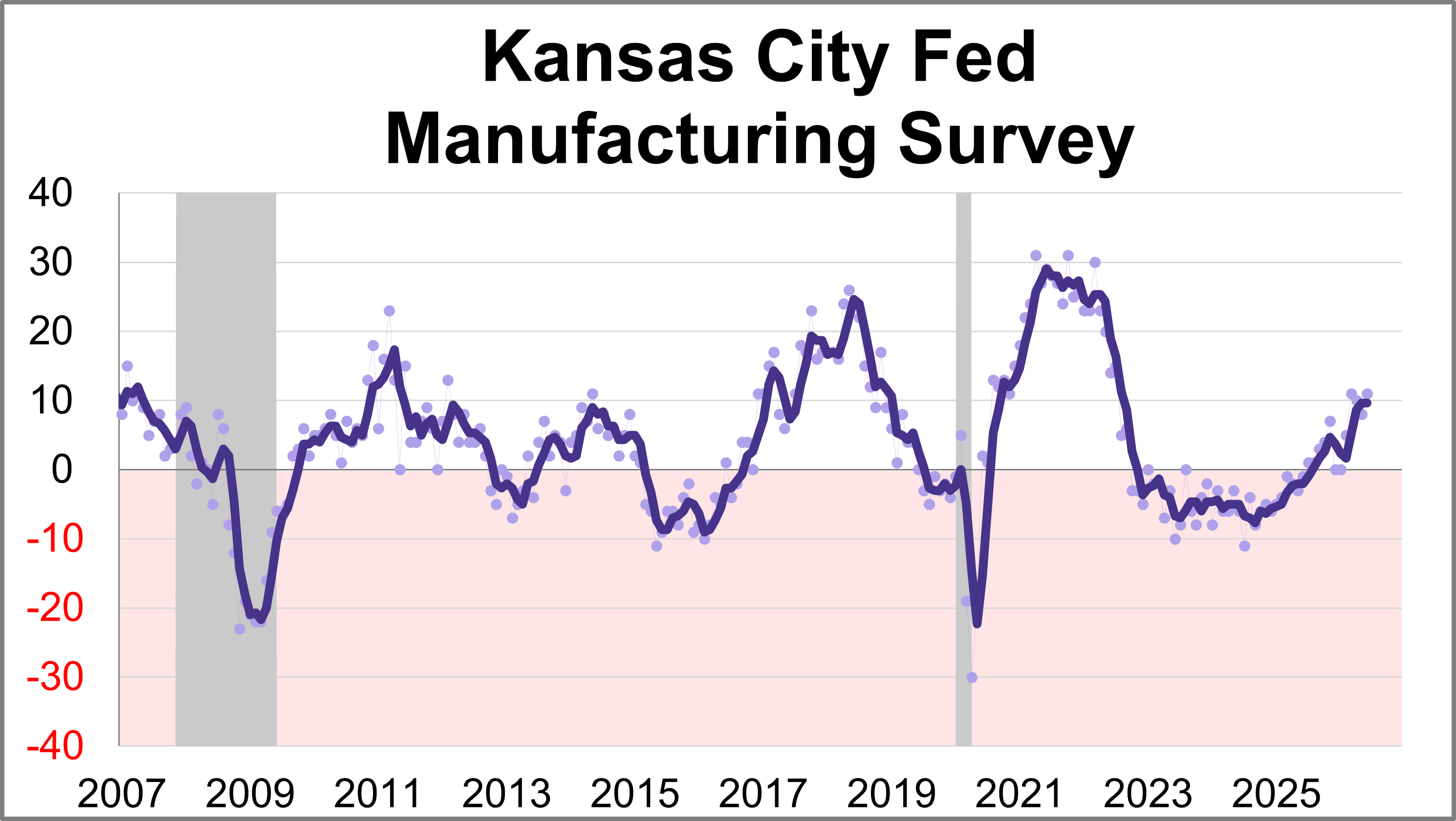

The Kansas City Fed Manufacturing Survey revealed regional activity continued to increase in May. The composite index came in at 8 this month, down slightly from 10 in April but still indicating continued expansion.

Alphabet Inc.’s addition to the Dow Jones Industrial Average marks another step in the benchmark’s effort to catch up with a market increasingly defined by Big Tech.

New orders for manufactured durable goods sank 4.5% in May to $332.05B, slightly less than the projected 5.0% monthly decline.