At the start of the regional war in February, Wall Street banks were grappling with the prospect of a protracted slowdown in the Middle East. Three months in, many firms are rushing to add bankers after local investors largely looked past the conflict and doubled down on dealmaking.

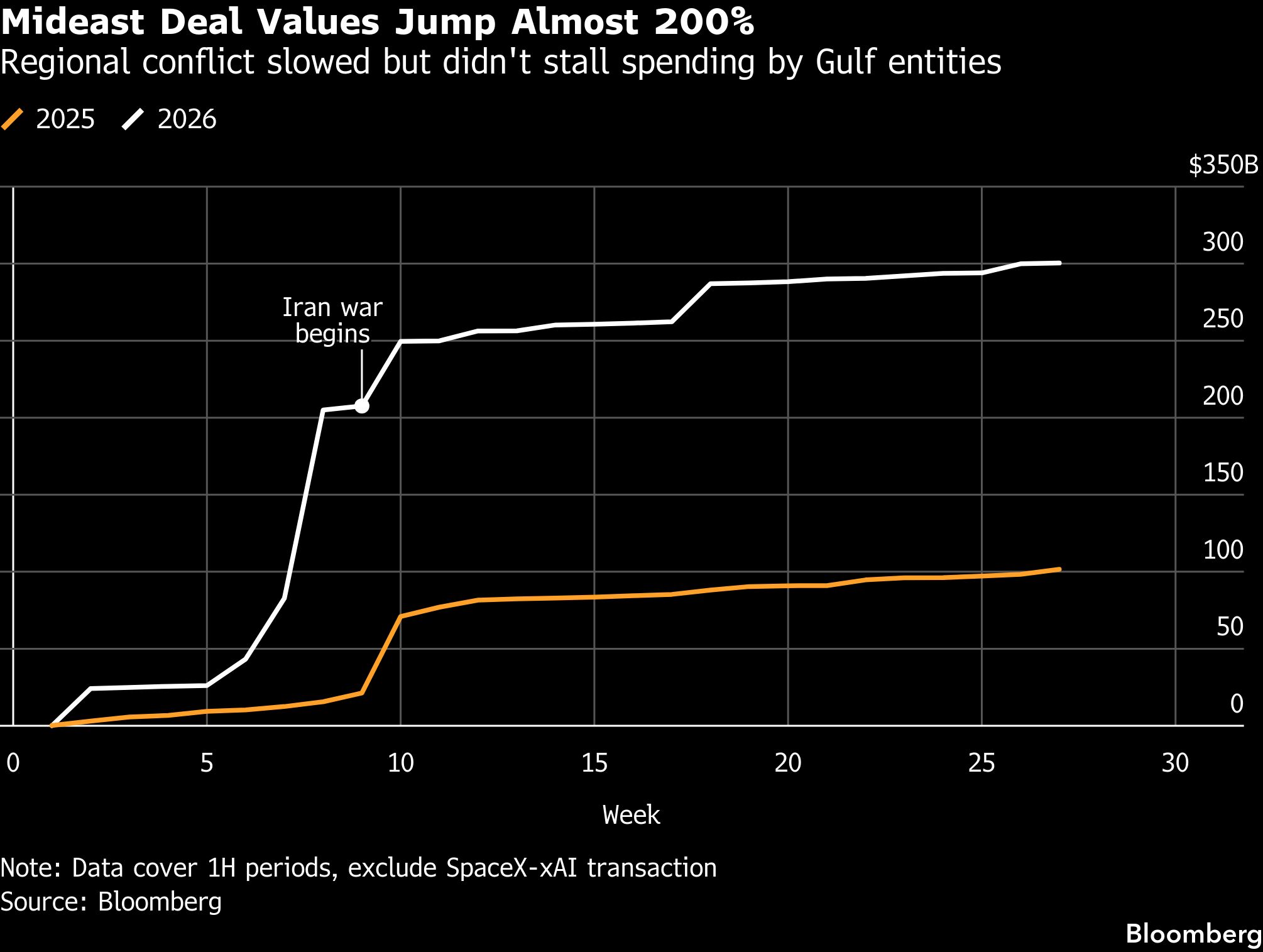

The value of deals involving Gulf entities rose almost 200% in the first half of the year to about $300 billion, according to data compiled by Bloomberg. That’s been driven by large bets on companies at the heart of the artificial intelligence boom, such as OpenAI and Anthropic PBC, helping activity recover strongly from a roughly 15% year-on-year drop in March, when the war began.

The regional conflict has also prompted state governments to accelerate plans to bolster spending on infrastructure and defense, which could lead to billions of dollars of fresh investment and lucrative work for Wall Street institutions. Revenue for the Middle East at investment banks rose about 5% to $619 million in the first half, according to Dealogic, with a 55% jump in mergers and acquisitions fees offsetting declines in equity capital markets.

The wartime surge has meant one of the region’s leading investment banks that was previously pessimistic about meeting annual targets is now on track to meet goals and is looking to add headcount, a person familiar with the matter said. A second firm was similarly surprised by the volume of deals, and is now working on outbound transactions as well as local infrastructure and defense projects, according to a separate person.

The pickup in activity has led to a steady influx of professionals through the year. Barclays Plc, which is seeking to boost its presence in the Middle East, recently relocated energy banker George Tanner to Dubai from London. JPMorgan Chase & Co., Standard Chartered Plc, Deutsche Bank AG and Rothschild & Co. are among those adding staffers, people familiar with the matter said, asking not to be identified discussing confidential information.

Others like Lazard Inc. and Citigroup Inc. are hiring for Dubai-based jobs, according to posts on LinkedIn. Further afield, a Chinese bank is looking to add bankers in Dubai as part of its ambitions to secure cross listings between Hong Kong and bourses in the United Arab Emirates, a person familiar with the matter said. Even law firms, including New York-based Skadden, Arps, Slate, Meagher & Flom LLP that opened an Abu Dhabi office last year, have added staff.

Representatives for Citigroup, Lazard, Rothschild and Barclays declined to comment. Standard Chartered continues to selectively add senior talent, “reflecting our conviction that the Middle East will play an increasingly influential role in global capital flows and dealmaking,” said Rajesh Singhi, the firm’s global head of M&A advisory. A spokesperson for JPMorgan said the firm’s recruitment reflects the needs of its business and clients, while Majed Julfar, Deutsche Bank’s head of corporate coverage Middle East & Africa and chief country officer for the UAE touted the region’s “strong economic fundamentals and long-term growth prospects.”

To be sure, significant regional challenges remain, including attracting talent. Many bankers, traders and executives who temporarily relocated after Iranian missiles targeted the region have returned, but uncertainties persist. Negotiations between the US and Iran have been hamstrung by contentious issues and repeatedly interrupted by tit-for-tat attacks.

“There’s definitely been a shift in the tone,” said Gregory Agius, Switzerland-based chief executive of Agius & Partners, a recruitment firm that specializes in finance and private banking. Low taxes, growth, lifestyle and concentration of capital in the whole region remain attractive draws, but candidates are more selective, he said.

“Now it’s a physical security choice, and that changes everything,” according to Agius. “Employers need to be sharper on compensation, relocation support, and long-term focus.”

The war has also impacted specific pockets of dealmaking, including new share sales. Several initial public offerings have been delayed or canceled in the region after the war, with shareholders concerned that geopolitical volatility could impact trading performance.

And it’s hurt dealmaking activity in areas like construction, retail and hospitality, according to George Traub, managing partner at Lumina Capital Advisers. Still, he said, M&A in strategic sectors continues, “some with increased urgency,” in critical fields like food security, power, infrastructure services, logistics and defense that require larger deal sizes, cross-border financings and structuring.

Weeks into the war that began when Israel and the US attacked Iran and triggered retaliation from Tehran, some Wall Street executives acknowledged “near-term headwinds” facing the region. Still, many lined up to offer support and bet on Gulf governments using their oil wealth to play a bigger role on the global stage. “Our clients’ ambitions across the region haven’t changed,” Goldman Sachs Group Inc. Chief Executive Officer David Solomon told Bloomberg News at the time.

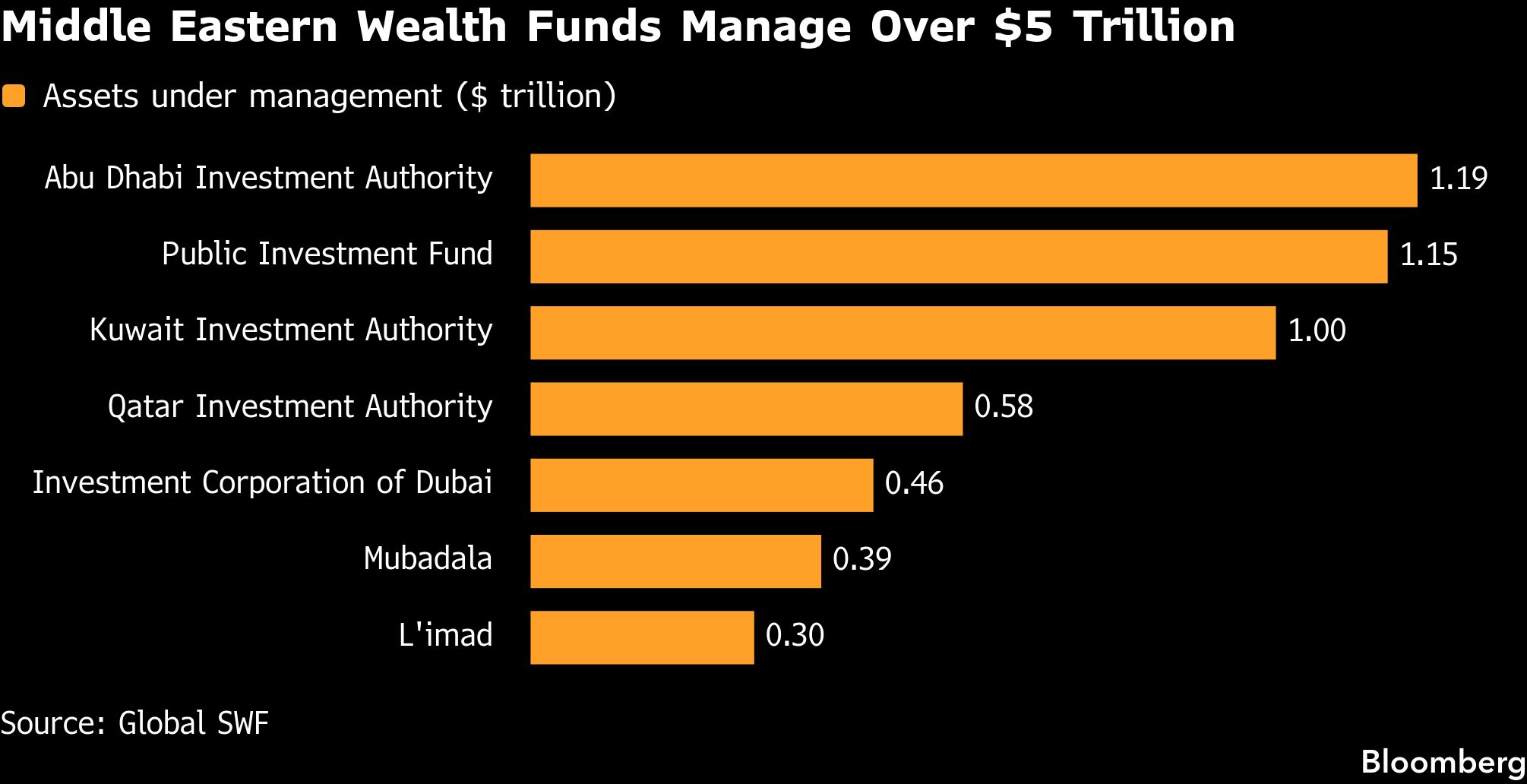

Indeed, Middle Eastern investors have continued to deploy billions of dollars across sectors. Gulf wealth funds have committed a record $53.9 billion so far this year, half of which went to the US, followed by China and the UK, while technology was the most popular sector, according to Global SWF Managing Director Diego Lopez.

“The ranking of most active funds was topped once again by Mubadala, which invested $15.2 billion at group level,” Lopez said. “The rest of Gulf 7 funds showed no sign of slowdown either despite the Iran War.”

Gulf wealth funds, which together oversee assets worth close to $5 trillion, have long been key backers of global deals. Over the years, in times of financial turmoil, these investors have often stepped in as bankers of last resort. This time around, with conflict at their doorstep, regional governments have also unveiled a swathe of plans to bolster capabilities across key areas.

The UAE, for instance, is working on a plan to try to end its dependence on the Strait of Hormuz. At the heart of the UAE’s plan is an expansion of its eastern ports that sit outside the critical chokepoint on the Gulf of Oman coast. Meanwhile, Abu Dhabi’s L’imad Holding is joining local and global partners in an investment venture targeting infrastructure projects worth $30 billion.

Over in Saudi Arabia, Aramco executives have lined up the most ambitious privatization plan in the company’s history, driven by a desire to shore up the balance sheet — the deals are likely to eventually raise as much as $35 billion, Bloomberg News has reported.

And in Kuwait, some of the largest global investors including BlackRock Inc.’s Global Infrastructure Partners and Brookfield Asset Management Ltd. are vying for a $7.5 billion stake in the state-oil firm’s pipeline network.

Two months into the war, Moelis & Co. CEO Navid Mahmoodzadegan was already touting a “return to normal” in the Middle East, where the firm has deep ties to regional governments and is an influential force in dealmaking.

“There’s a real opportunity when we get on the other side of this to get to a new Middle East,” he said.