This roller-coaster week for tech stocks from Seoul to New York fueled by extreme investor positioning and worries over chip demand is sending a strong signal: the case for the artificial-intelligence trade is still strong, but the days of everything going up in a straight line appear to be over.

After a first tremor two weeks ago sparked by fears of higher interest rates, AI-related stocks plunged again on Tuesday, this time on worries about demand for AI chips. The selloff sent South Korea’s Kospi, home of chipmakers SK Hynix Inc. and Samsung Electronics Co., down 10%. The Nasdaq 100 followed, losing 3.3% on the day in its second-worst session this year.

US chipmaker Micron Technology Inc. later dismissed those worries with a blowout sales outlook, sending its stock to a record and prompting investors to buy the dip in tech stocks worldwide. But the relief rally didn’t last. The Kospi plunged another 5.8% on Friday. The trigger this time: AI’s inflationary implications, evidenced by price hikes by Microsoft Corp. and Apple Inc.

While there hasn’t been panic selling, the cracks in this year’s biggest trade are real, and extreme investor positioning — including alarming levels of leverage in some of Korea’s exchange-traded funds — means the easy days of AI boom could be behind us, and the AI rally may no longer be a single trade.

Shares in memory chip-makers have risen more than 200% this year, while baskets of stocks exposed to data centers and electrical equipment have more than doubled. Yet, the rally in hyperscalers has stalled, and the Magnificent Seven Index is now down on the year. Google parent Alphabet Inc. has tumbled 15% since its peak in May. After raising $85 billion of equity this month, the company is losing key people who built its AI models.

“As in every technological revolution, growth at one point shifts from the infrastructure to the application layer. Most value of the internet economy was captured by companies like Amazon or Google, not Cisco or Sun,” says Igor Pejic, author of the book Tech Money.

“In the case of AI, growth momentum is now shifting from chips and data centers to vertical companies applying and monetizing the models. Examples include biotech, robotics and defense tech. This transition from the infrastructure to the application layer will take quite some time, but investors must be vigilant not to end up in a value-trap and overspend on infrastructure players.”

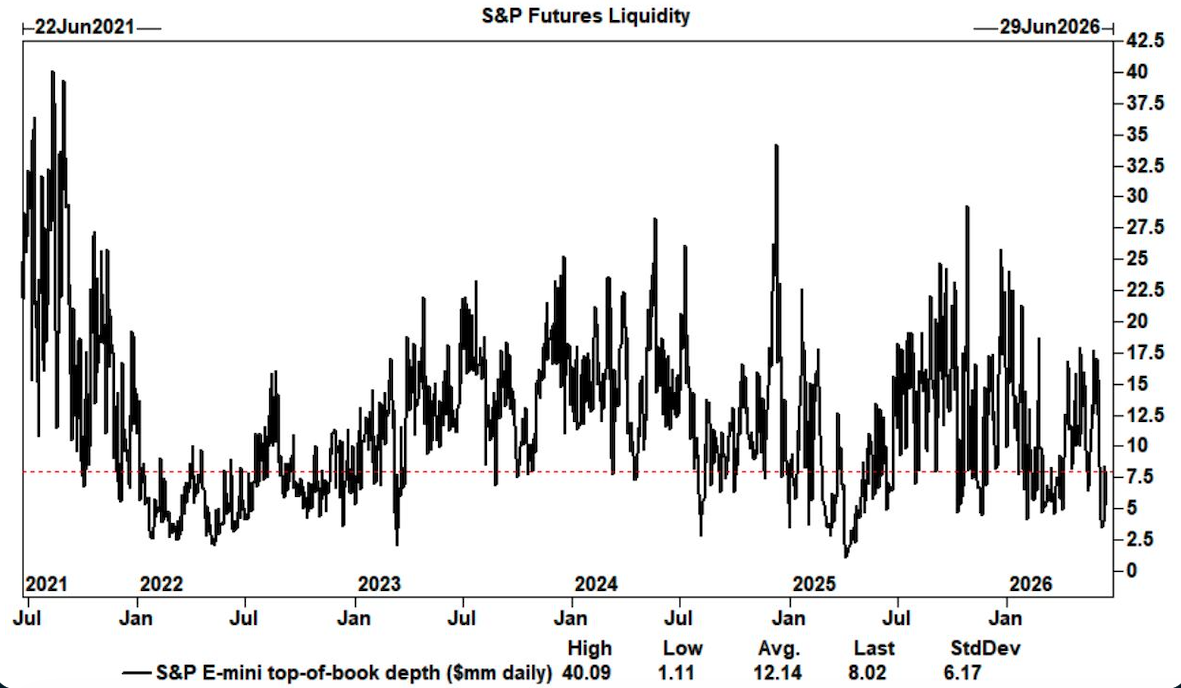

Stock market dynamics have also been a big factor behind the wild swings seen this week. Goldman Sachs Group Inc. traders have warned about shallow top-of-book liquidity, volatility-control funds have been forced to sell on big days, and leveraged ETFs in South Korea used by retail investors have been a big catalyst of volatility.

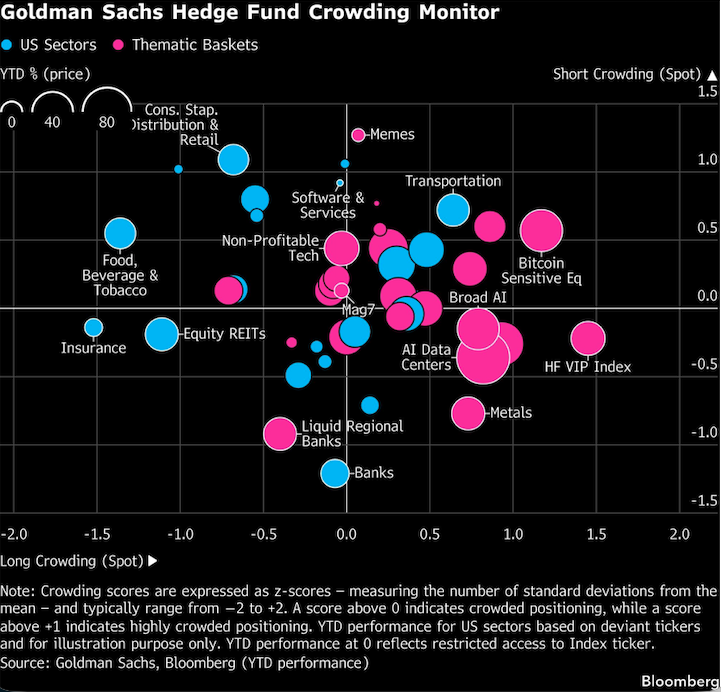

High investor positioning is a rising risk, but not yet acute. Long positions in AI and data-center themes were only at near six-month highs as of June 18, before the pullback started, according to Goldman Sachs Group Inc. prime-brokerage data.

Overall, that’s not high enough to signal that the bull market is over. Meanwhile, the US economy is healthy, the overall market sentiment is positive but not euphoric, and data shows earnings growth is still strong.

“AI infrastructure stocks will generate roughly half of S&P 500 earnings-per-share growth this year and have driven most of the year-to-date increase in index earnings-per-share estimates,” said John Flood, head of Americas equities execution services at Goldman Sachs. “Let’s see what second-quarter earnings bring us. I am optimistic.”

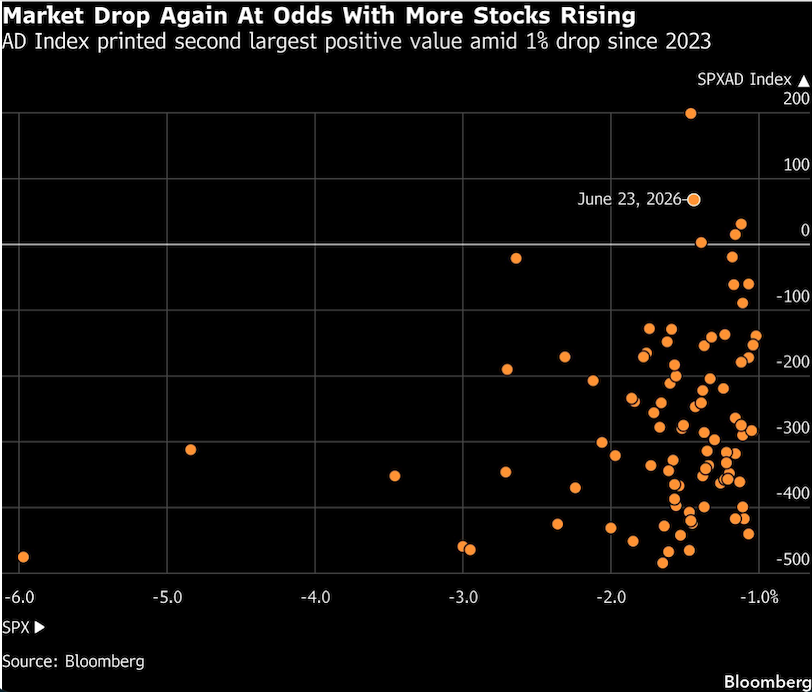

While hedge funds have raised their exposure to US tech back toward five-year highs, their gross and net positioning in the Magnificent Seven has fallen to a one-year low. And while the group of stocks still dominates benchmarks, market breadth turned positive on Tuesday even as the S&P 500 fell, showing one of the strongest advance-decline readings since 2023. This is a sign that the selling was concentrated in Big Tech, while investors found plenty of other stocks to buy on that day.

While the Nasdaq 100 did stage an almost 0.8% rebound on Thursday, futures trading suggests it will wipe that out and extend a weekly decline that’s already in excess of 3%.

Overall for investors, a thinner margin for error doesn’t mean the rally is over. It means the ride gets rougher from here, with more rotation, more sessions when the AI theme gets sold hard and more air pockets in the most crowded corners of the market. None of that is enough to completely derail the rally, but rather the implication of narrowly led, heavily owned, leverage- and retail-fed market. Investors who want the upside will have to live with the chop that comes from now on. That is the price of admission, not the exit sign.