July is a great time to buy stocks. In fact, it’s been the best month for the S&P 500 Index in the past two decades. Bulls are finding comfort in that history ahead of what stands to be an eventful stretch.

The S&P 500 hasn’t had a losing July since 2014, a streak of consistency absent elsewhere in the year. Since 2005, the US equities benchmark has averaged a 2.5% gain in July, more than four times the advance in the other 11 months, according to data compiled by Bloomberg.

This year the track record is meeting worries that a confluence of market-moving events will whip up volatility in the second half of the month. That’s when Corporate America kicks off its next round of earnings announcements, coinciding with the release of key inflation data and a Federal Reserve interest-rate decision.

“The first two weeks of July will probably be strong for stocks, like it usually is, then traders will probably start pounding the table to put on hedges in the second half of the month for both August and September because of uncertainty ahead of the Fed’s next rate decision,” said Chris Murphy, co-head of derivatives strategy at Susquehanna International Group. “Then the Mag Seven could be another catalyst for selling heading into August if their earnings results disappoint.”

The 500-member index has notched 24 records so far in 2026, ranking among the top 20 opening six months to a year since World War II, data compiled by investment research company CFRA show. When that has happened previously, the index proceeded to gain another 6% in the next six months, on average, the firm’s data show.

But favorable seasonal patterns are confronting worries around fundamental risks. The fallout from the Iran war continues to weigh on inflation, raising the pressure on the Fed to contain it. The specter of rising interest rates threatens corporate earnings, and the US midterm elections in November remain a wild card.

To Murphy, the case for owning index protection starting in mid-July in either the SPDR S&P 500 ETF Trust, or SPY, or the Invesco QQQ Trust exchange-traded fund, or QQQ, is growing. August and September are historically the two weakest months of the year for US stocks, Murphy said.

Even after a basket of the so-called Magnificent Seven stocks shed nearly 9% in June, its worst monthly drop since March 2025, technology stocks remain at risk of further weakness as overall investor exposure in the group hovers at elevated levels, according to Citigroup Inc. strategists. Bearish flows are building in both tech stocks and the broader S&P 500.

“Existing Nasdaq long positioning risks are on the rise, with ~80% of long positions offside, highlighting increased vulnerability to further long unwinds,” a team led by David Chew wrote in a note to clients.

Meantime, Bank of America Corp. technicians said investors should hedge any further rallies and brace for a potential “three-wave correction” in the next few months.

The jobs report on Thursday will be the first test for the market this month. The options market is bracing for a 0.8% swing for the S&P 500 on that day, up from a realized move of 0.6% over the past 12 months, according to data compiled by Citi. The release comes a day early due to US stock and bond markets being closed on Friday in observance of the July 4 holiday.

Then, JPMorgan Chase & Co. and other big banks will kick off earnings season on July 14. Investors will also assess a CPI report on the same day, followed by the Fed’s rate decision on July 29. Those are the critical milestones that will determine if bulls can keep driving stocks higher after an 18% rally since late March pushed the S&P 500 toward 7,500, a key psychological milestone.

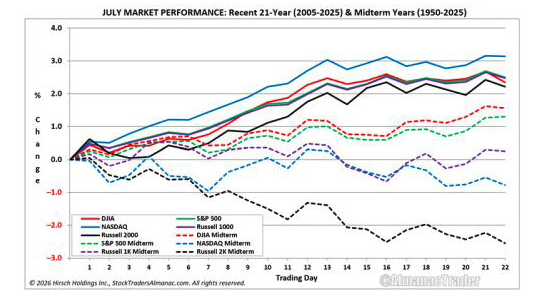

Typically, July opens strong for stocks, before risk-on spirits fade mid-month, according to Jeffrey Hirsch, editor of the Stock Trader’s Almanac.

Overall though, July has been a strong month for US stocks, even during US midterm election years. Since 1950, the S&P 500 has averaged a gain of 1.3% in US midterm years in July. Returns have been notably weaker for small caps, with the Russell 2000 Index averaging a loss of 2.5% during that span, according to Hirsch.

With the Russell 2000 coming off its best first half relative to the S&P 500 since 2001, this suggests traders may favor larger, more established companies if uncertainty around inflation, interest rates and economic growth persists, according to Hirsch.

“Seasonal trends suggest July could continue to provide support for equities, but the midterm-year backdrop serves as a reminder that volatility can emerge quickly and unexpectedly,” according to Hirsch. “But the selloff in the Mag Seven stocks of late has taken some of the air out of any bubble fears traders had about the AI frenzy and leaves the door open for stocks to rebound in early July.”

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Jessica Menton