Markets have been hyper-focused on AI, crypto and buffer ETFs, but REIT ETFs have quietly staged an impressive comeback. The REIT terrain has shifted rapidly over recent years, and forward-looking investors and advisors have taken notice.

Key Takeaways

- Data center REITs surged 37% YTD through May 2026, leading a sector-wide revival driven by flattening rate trajectories.

- Schwab’s SCHH crossed $10 billion in AUM, while equal-weighted RDOG outpaced the market with a 15% return.

- Yielding over 6%, specialized REIT strategies let advisors capture equity growth upside while boosting overall portfolio dividend income.

Macro Tailwinds

The sector’s recent hurdles are well-known: Retail faced e-commerce disruptions, office REITs were battered by the shift to hybrid work, and high interest rates over 2024–2025 elevated capital costs while depressing property valuations. However, as we cross the midpoint of 2026, a flattening trajectory and subsequent reduction in rates by global centrals have provided tailwinds to these depressed REIT sectors, powering a cyclical pivot back into the asset class.

Broad Index vs. Sector Selection

The core lesson of 2026 is that REITs can no longer be treated as a monolithic asset class. There is a stark divergence within the REIT market, highlighting the growing importance of granular selection.

-

AI Tailwinds: Data center REITs are the undisputed standout. Driven by insatiable physical demand for high-speed data and AI infrastructure, the sector returned more than 37% year-to-date through May 2026, single-handedly anchoring the commercial real estate revival.

-

Secular Growth Stories: Industrial and logistics REITs continue to thrive on e-commerce, reshoring and supply-chain modernization. Meanwhile, health care REITs (senior housing and skilled nursing) are showing structural resilience rooted in demographic aging.

-

Contrarian Income: Office REITs remain structurally challenged by hybrid work, and multifamily REITs face supply pressures across specific Sun Belt markets. Yet, because years of underperformance have left many of these assets trading at distressed valuations, they offer significant compelling recovery potential for clients with higher risk tolerances.

REIT Exposure via ETFs

Because REITs are legally required to distribute at least 90% of their taxable income to shareholders as dividends, their high yields give them bond-like characteristics. However, they offer two advantages over fixed income — capital appreciation and inflation-hedged dividend growth. As a result, many advisors treat REIT ETFs as a “hybrid” allocation, effectively boosting the yield of a standard equity bucket without giving up growth equity upside.

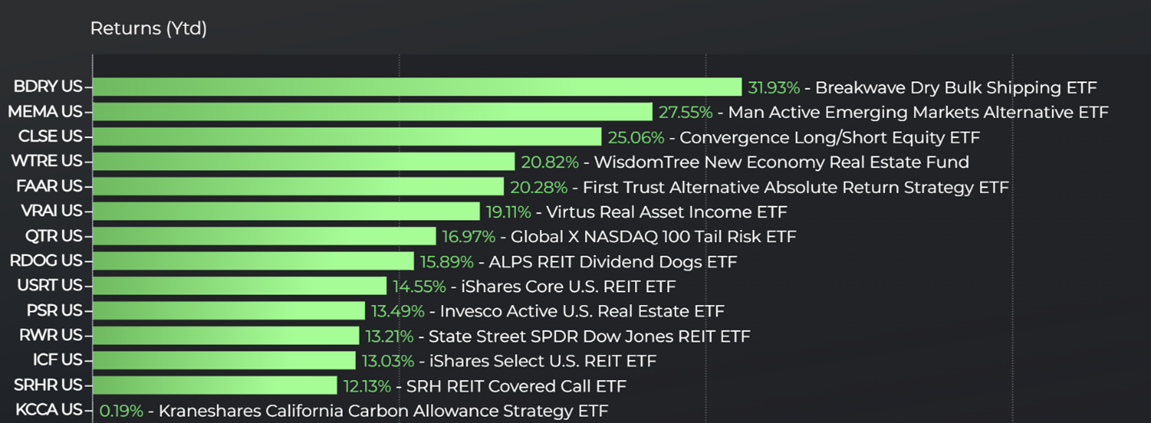

Top-Performing Alternative ETFs in 2026

Investors are spoiled for choice when navigating the ETF market. Broad index funds that capture the entire market, such as the State Street Real Estate Select Sector SPDR ETF (XLRE) and the Schwab U.S. REIT ETF (SCHH), span the gamut — holding a mix of residential, industrial, and specialized real estate. As one of the premier vehicles for tracking the S&P 500’s real estate sector, XLRE has captured a 9% gain year-to-date. The $8 billion fund is heavily weighted toward multi-billion-dollar cell tower and industrial logistics giants, capturing elite enterprise winners.

Meanwhile, SCHH took in north of $1 billion in net inflows over the past year and just recently crossed the $10 billion mark in total assets — solidifying its place as one of the most liquid options out there. It is also one of the most cost-effective core real estate building block on the market, boasting an expense ratio of just 0.07%. Strong performance from its largest tech and health care holdings has insulated the fund from office sector anxieties.

Conversely, tactical funds like the ALPS REIT Dividend Dogs ETF (RDOG) alter the playbook. By applying the “Dogs of the Dow” theory — equal-weighting the highest-yielding REITs across various segments — RDOG has significantly outpaced the broader cap-weighted market, delivering a 15% total return in 2026. The fund’s strategy has squeezed out a trailing 12-month dividend yield of more than 6% by capturing heavily discounted, high-yielding names in segments poised for a cyclical rebound, like hospitality and gaming/casinos.

Focused thematic funds like the WisdomTree New Economy Real Estate Fund (WTRE), which isolate secular growth stories like technology, e-commerce and logistics infrastructure, have also outperformed to the tune of 20% on a NAV basis.

Bottom Line

After years of being overshadowed by higher-growth themes, real assets are reclaiming the spotlight. Whether deploying low-cost, multi-sector giants or tilting toward specialized tech infrastructure plays, REIT ETFs offer advisors a timely opportunity to capture income and equity upside in an improving rate environment.

Originally posted on ETF Trends

For more news, information, and analysis visit the Thematic Investing Content Hub.

Vettafi.com is owned by VettaFi LLC (“VettaFi”). VettaFi is the index provider for RDOG for which it receives an index licensing fee. However, RDOG is not issued, sponsored, endorsed, or sold by VettaFi. VettaFi has no obligation or liability in connection with the issuance, administration, marketing, or trading of RDOG.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Read more commentaries by VettaFi