A number of market headwinds—including trade tensions, rising interest rates and a general fear the long-running US economic expansion may be facing fatigue—have cast a shadow over the markets in the first half of the year.

Over the summer, some groups within the global equity market sold off sharply, leading to the current trends of poor performance and weak breadth. Foreign stocks, cyclicals and value-oriented sectors were the hardest hit.

While momentum stocks have prevailed since 2016, is quality about to have its day? Possibly, if volatility continues to rise, as Russ discusses.

In this issue, Research Affiliates discusses the funds’ long-term outcomes relative to peers, views on emerging market currencies and recent research centered on momentum.

An alternative risk premia strategy that relies on robust factors within a liquid, transparent, and disciplined framework has the potential to improve the long-term return prospects of traditional portfolios and to reduce their downside risk.

Fans of the “Fast & Furious” movies know the game of chicken. Two cars race toward each other, each driver waiting for the other to swerve out of the way. If neither swerves, the cars collide head-on. This game has been playing out in Europe as the UK and Italian governments each face off with the EU.

A review of last month’s market-moving events across countries and asset classes.

We look at ways to de-risk, diversify and differentiate ahead of a turn in the economic cycle.

After nearly 48 years in this business, we have seen a number of cycles and developed a long-term perspective. We have often spoken about the difference between a “secular bull market” and what many consider to be a bull market because it is up 20%+. The reciprocal is that a 20%+ decline represents a bear market.

A little over 10 years ago, few people had heard of mortgage-backed securities (MBS). Yet that changed when MBS brought the global financial system to its knees. Today, they’re still a pivotal part of the system, with the US Federal Reserve (Fed) the largest holder.

Reflecting on ten years since the Lehman Brothers bankruptcy: Households have reduced their borrowing, but governments haven’t. Debates over the response to the financial crisis may never end. Non-bank lenders have thrived while managing their risks.

Hurricane Florence made landfall in North Carolina today, bringing with it destruction and calamity, the cost of which could top $170 billion, according to analytics firm CoreLogic. If so, that would make it the costliest storm ever to hit the U.S.

As short-term rates move higher and the Treasury yield curve flattens, many investors are thinking about how to earn income while also protecting themselves against rising rates. In this post, we'll discuss why municipal floating-rate notes -- an often-overlooked part of the market -- may be an attractive option for these investors.

As Russ discusses, we remain in a strong dollar environment, which continues to have consequences for the market.

Stimulative measures drive growth, and the U.S. economy and stock market have benefited from quantitative easing, lower rates, less regulation and tax cuts. But Jeffrey Gundlach admonished investors that too much stimulus can backfire.

Investors tend to think of floating-rate bank loans as the cure for rising interest rates. But our research suggests that a rising-rate environment has historically been the worst time to buy loans.

Being wrong and admitting it, what a novel idea, yet as Bernstein states, “It helps to know that being wrong is inevitable and normal, not some terrible tragedy, not some awful failing in reasoning, not even bad luck in most instances. Being wrong comes with the franchise of an activity whose outcome depends on an unknown future.” Indeed, the real trick is to be wrong quickly for a de minimis loss of capital.

Risk is rising late in the cycle. How should investors respond?

There is a big economic calendar competing with mid-term election campaign stories. The increase in hourly wages in the employment report offset some market enthusiasm about continuing job market strength. With inflation concerns on a hair trigger, expect special focus on this week’s PPI and CPI. The Beige Book and JOLTS report will also get pundit scrutiny.

Nonfarm payrolls averaged a 185,000 gain over the three months ending in August, a relatively strong pace considering that labor market constraints are more binding and reports of worker shortages are rising.

One truism spanning the last three decades has been that emerging markets are a leveraged play on global growth – often outperforming when developed markets (DM) are growing but susceptible to sharp downturns when DM conditions are less favorable.

The macro data from the past month continues to mostly point to positive growth. On balance, the evidence suggests the imminent onset of a recession is unlikely. The largest risk to the economy is the escalation in trade war rhetoric.

This week, I had the privilege to attend the Cornerstone Macro Conference in New York. Langone’s presentation, moderated by Omega Advisers CEO Lee Cooperman, stood out as one of the highlights.

The Endless Summer (1966) is the crown jewel to ten years of Bruce Brown surfing documentaries. Brown follows two young surfers around the world in search of the perfect wave, and ends up finding quite a few in addition to some colorful local characters (Endless Summer).

There is a huge economic calendar in a holiday-shortened week. The mid-term elections impend, so politicians will be on the stump. With Labor Day setting the stage and the week loaded with key employment reports, expect plenty of attention to employment issues. Much of this will be confusing and unproductive spinning.

Is it different this time around?

Current stock market capitalization is largely an artifact of speculative psychology, not reasonably discounted cash flows. Unless investors rely on eternal sunshine of the spotless mind – the assumption that current levels of extreme cyclical optimism will be permanent – they should not expect the associated valuation extremes to be permanent either.

60% allocated to equities and 40% to bonds has been an extraordinarily successful investment strategy for most of the past 40 years, but I believe the show is now largely over. In this month's Absolute Return Letter, I focus on the 40%, and I argue that, although I don't expect 10-year government bonds to deliver more than 0-2% annual inflation-adjusted returns in the years to come, there are indeed things you can do to earn higher returns.

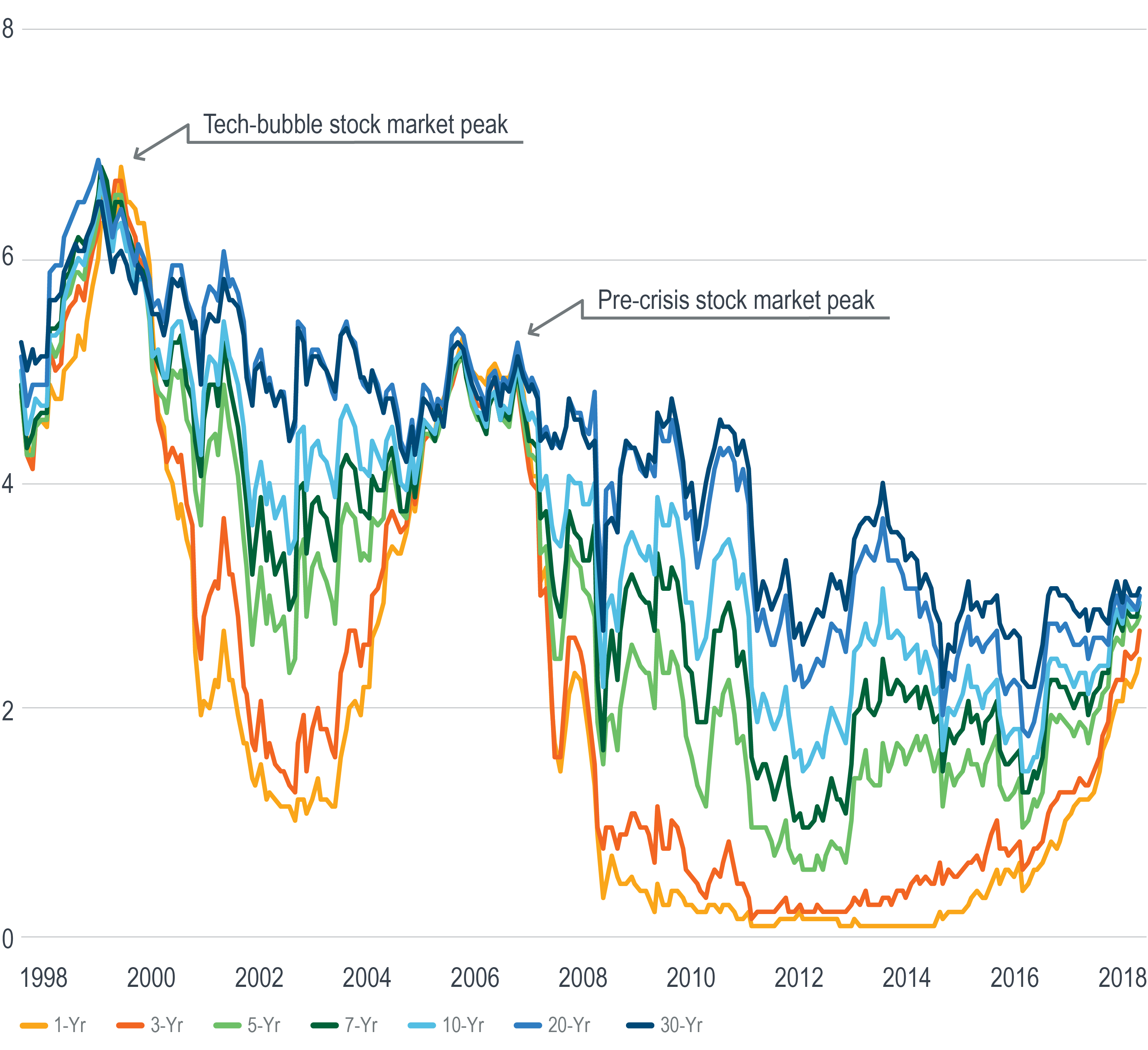

Investors and advisors have become concerned about the possibility, if not the likelihood, of the Treasury yield curve inverting. The reason for the concern is that the slope of the yield curve historically has been a good recession predictor.

The months of July and August are traditionally a little quieter for markets in Europe as participants take a summer break. But things don't stop completely. As the wheels get back up to speed, David Zahn, Franklin Templeton's Head of European Fixed Income, considers a few developments in Europe over the summer months that might have slipped under the radar.

It was the best of times, it was the worst of times. A tale of two world leaders, U.S. president Donald Trump and China president Xi Jinping—both of whose countries have among the world’s best economies right now. But whereas Xi is playing Santa Claus to the rest of the world, doling out loans to finance-starved countries, Trump is playing Scrooge, waging an economic war with Canada, the European Union, China and others.

Change will be today’s topic. Below I’m reproducing part of a letter I originally wrote in December 2007 and have referred to several times. It is the single most-read letter I have written and the most commented-on, too. I consider it, in some ways, my most important letter. If you’ve read it before, you should read it again. I have updated it a little bit, but the principles are just as timeless as ever. And for the time conscious, we have shortened it a bit and at the end, I try to apply those principles to present economic times.

The minutes of the July 31-August 1 Fed policy meeting and Chairman Powell’s Jackson Hole speech reinforce the view that the central bank will raise short-term interest rates again on September 26. The pace of monetary tightening beyond that is unclear, reflecting a number of uncertainties.

In a future of lower expected price appreciation, investors should focus on the second leg of returns: income. ETFs make it incredibly easy to capture diversified sources of higher-yielding assets.

This week, as investors and economists fixate on record highs set by major stock market indices, they have ignored much more significant developments that emerged from the Federal Reserve's annual meeting in Jackson Hole, Wyoming. Fed Chairman Jerome Powell delivered a speech that somehow was almost universally interpreted as a reiteration of his commitment to continue to raise rates throughout the next few years. "Steady as she goes" was the takeaway from just about any news outlet. But the Chairman's actual message was essentially the opposite of what the media reported.

Investors might be interested in this month’s alarming debt projections from the CBO, which beg the question: Is America’s near-vertical debt trajectory bullish or bearish for bond holders? Here’s my answer.

As yields increase, short-maturity bond funds can offer both higher income potential and a cushion against interest rate risk. Karen explains the mechanics, in part three of her Rising Rates series.

The flattening Treasury yield curve is getting a lot of attention, but there’s another flattening that is arguably of greater importance: the narrowing return gap between low- and high-risk assets. Jeff explains.

Reduced global trade may have the unintended consequence of strengthening the US dollar, raising interest rates and pushing down stock prices. Together with tighter Federal Reserve policy, these developments may increase market turbulence.

In commodity investing, roll yield and carry are not the same thing.

Looking through your old compact disc collection can be nostalgic. The cover photo on your favorite CD or a few bars of a summer song can transport you back in time to what seems like a better, simpler place.

Turkey's crisis may offer investors the opportunity to build positions in ASEAN countries and India.

Data shows a solid economy, yet markets are acting like recession is around the corner. Russ explains why.

We believe the Income Fund has the tools to be resilient in the face of rising interest rates.

The US economy has continued to perform well on many fronts, with positive readings for growth, employment and inflation. In terms of growth, the stimulus effect from tax cuts was clearly visible in second-quarter 2018 data, and could be maintained for at least another quarter, in our view.

The early part of 2018 was characterized by US equity market volatility. What stands out is the contrast with abnormally low volatility last year. The S&P rose over the 12 months of 2017 with a benign economic backdrop. We think true investment risk has probably declined since January as equity valuations are now at more normal levels creating more interesting opportunities.

We have used the “Not Afraid” story many times over the past 48 years, but we dredged it up again this morning because of the many questions about “being afraid” we got in Boston two weeks ago and New York City last week.

US investment-grade corporate bonds look cheaper today than their lower-quality counterparts in the high-yield market. Is this the buying opportunity of a lifetime? Not exactly. A closer look reveals there’s actually method to the madness.

Since 2008, US growth stocks (particularly in faster-growing sectors such as technology) have tended to perform better than US value stocks, as the chart below shows.

For the first time in at least 40 years, there’s a fundamental economic reason that a yield curve near-inversion might notherald a recession.