Nonfarm payrolls averaged a 185,000 gain over the three months ending in August, a relatively strong pace considering that labor market constraints are more binding and reports of worker shortages are rising. The unemployment rate held steady at 3.9%, held up by a drop in labor force participation (likely a seasonal quirk related to the start of the school year). Average hourly earnings surprised to the upside, although these figures tend to be quirky.

Prior to seasonal adjustment, nonfarm payrolls advanced by 334,000 in August (about the same as a year ago), with almost all of that in education (non-education jobs rose 8,000, vs. -6,000 in August 2017). Adjusted, payrolls rose by 201,000 (median forecast: +190,000), but with a net downward revision of 50,000 to the two previous months. That left the three-month average at +185,000 (+183,000 for the private sector). Manufacturing payrolls fell by 3,000 (auto production: -4,900, although seasonal adjustment is difficult in July and August due to summer plant closings). The pace of job growth improved in the first half of this year. The demographics (an aging population and more limited pace of immigration) suggest that labor force growth should be slowing.

Chart 1

Click here to enlarge

Chart 2

Click here to enlarge

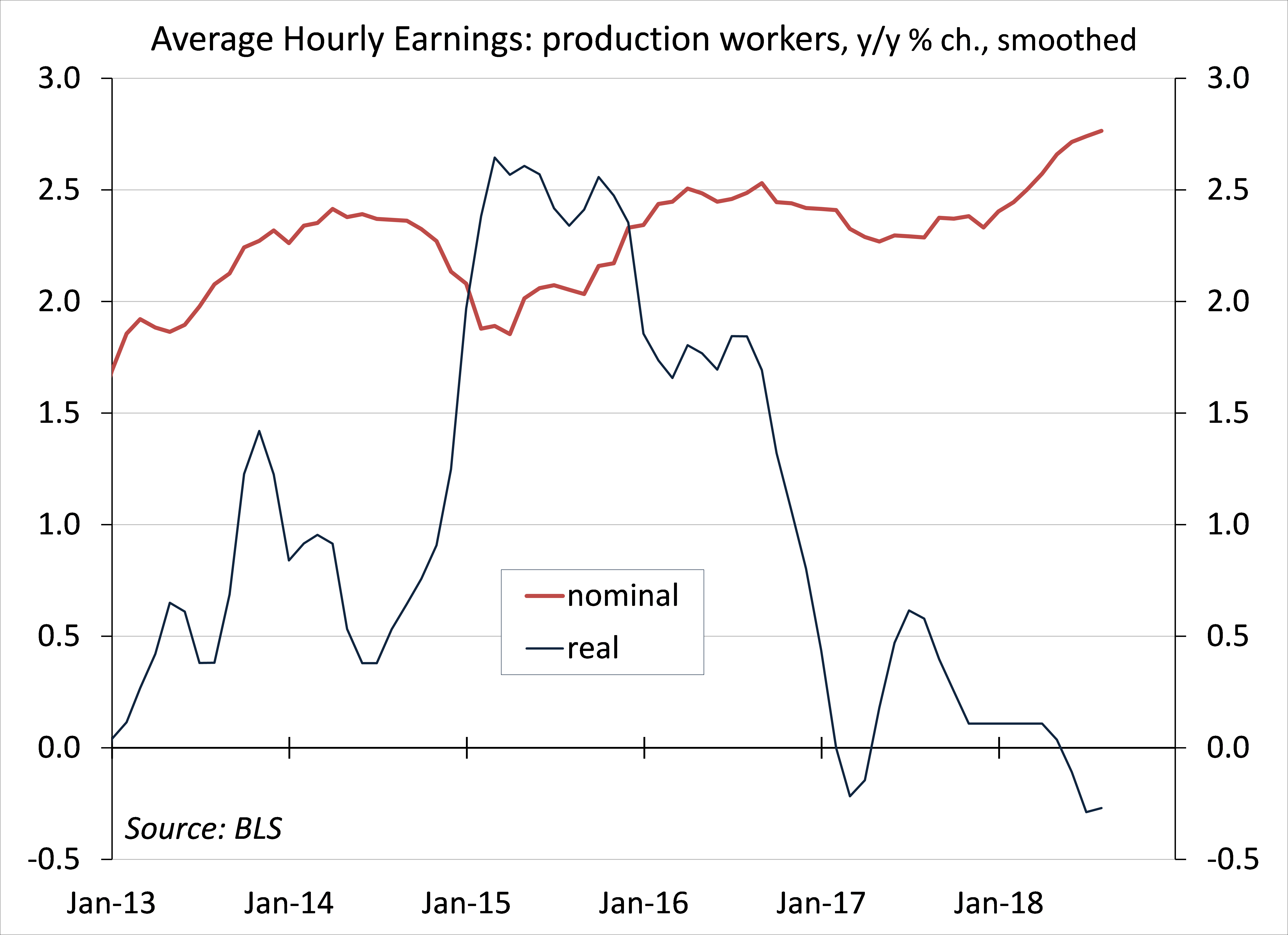

Average hourly earnings rose 0.4%, bringing the y/y pace to 2.9%. The monthly wage figures are notoriously quirky and subject to revision. The trend appears to be gradually higher, but still relatively moderate and has been outpaced by inflation.

The unemployment rate would have fallen further in August if not for a drop in labor force participation. Don’t read anything into that. The household survey yields reasonable estimates of ratios, but there is still a fair amount of statistical noise and seasonal adjustment is often quirky at the start of the school year (more so in September, but the school year starts in August for many).

Chart 3

Click here to enlarge

Chart 4

Click here to enlarge

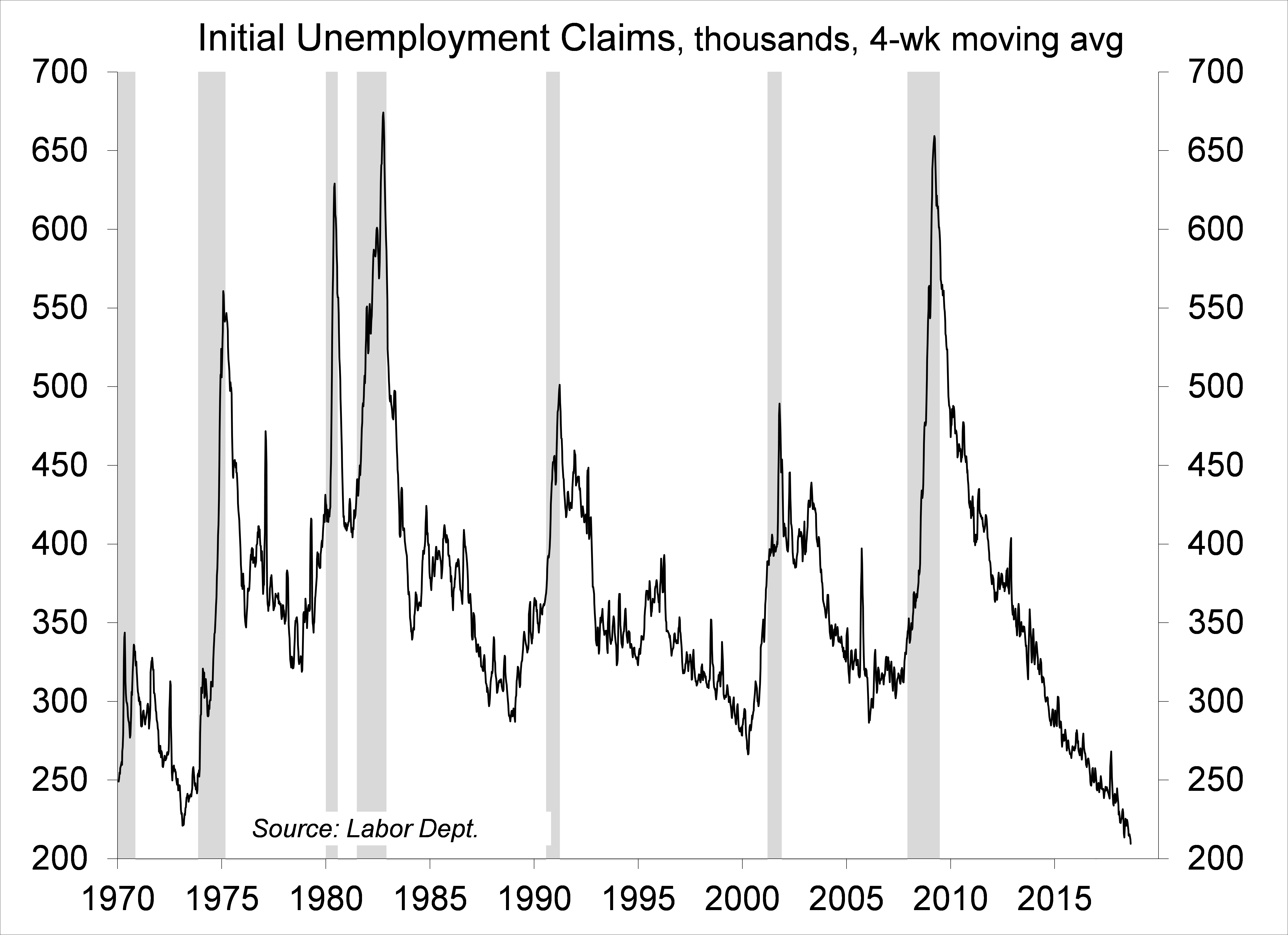

The broad range of labor market data, including weekly claims for unemployment benefits (now at their lowest level since 1969), point to tighter job conditions. That should generate further anxiety for the Federal Reserve. Monetary policy decisions will remain data dependent, but the level of uncertainty is expected to rise in the months ahead.

The opinions offered by Dr. Brown should be considered a part of your overall decision-making process. For more information about this report – to discuss how this outlook may affect your personal situation and/or to learn how this insight may be incorporated into your investment strategy – please contact your financial advisor or use the convenient Office Locator to find our office(s) nearest you today.

All expressions of opinion reflect the judgment of the Research Department of Raymond James & Associates (RJA) at this date and are subject to change. Information has been obtained from sources considered reliable, but we do not guarantee that the foregoing report is accurate or complete. Other departments of RJA may have information which is not available to the Research Department about companies mentioned in this report. RJA or its affiliates may execute transactions in the securities mentioned in this report which may not be consistent with the report's conclusions. RJA may perform investment banking or other services for, or solicit investment banking business from, any company mentioned in this report. For institutional clients of the European Economic Area (EEA): This document (and any attachments or exhibits hereto) is intended only for EEA Institutional Clients or others to whom it may lawfully be submitted. There is no assurance that any of the trends mentioned will continue in the future. Past performance is not indicative of future results.

© Raymond James

© Raymond James

Read more commentaries by Raymond James