Learnings from Lehman Brothers

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSeptember 15, 2008, is a day that I will never forget. I was working for the Federal Reserve at that time, based in Chicago. My office phone rang early that morning: it was my counterpart at the Fed in New York. “Lehman Brothers has filed for bankruptcy and all hell is breaking loose,” I remember him saying. “Can you get out here to lend a hand?”

I promised to check with my local boss, go home to pack, and fly out that evening. “You don’t understand,” he said. “We’ve made a reservation for you on the 10 a.m. departure. Go straight to the airport. In transit, please text your clothing sizes to me; we’ll order the things you’ll need for the first few days. And have your wife send two weeks of gear to our address in lower Manhattan.”

I called home. “Honey,” I explained, “I won’t be home for dinner … not for quite a while. And can you send a bunch of clothes to New York?” “Who is she?” my wife asked. That was the last laugh we shared for some time.

As we all reflect back on the events of a decade ago, several questions arise. Have we learned the lessons offered by the experience and taken corrective action? Have our powers of surveillance improved, so that we have a better chance of detecting the next crisis? And what are the lingering after-effects that still require attention? Now that we are ten years out from the crisis, let’s assess what we have learned.

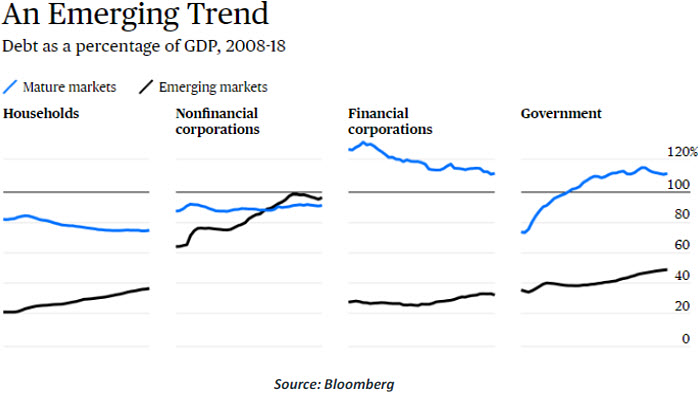

The Dangers of Debt

Debt was the kindling for the crisis. Normal amounts of borrowing are healthy; in fact, modern economies cannot work without intermediation between savers and investors. But having sufficient equity backing lending provides a buffer against loss, insurance against contagion, and the right incentives for both parties to the transaction.

By 2008, Americans had taken out mortgage debt using a very thin foundation of equity. According to the National Association of Realtors, the average down payment on a home had dropped to just 2%. Home loans had become increasingly complex, as had the mortgage-backed securities (MBS) formed from those loans.

As long as home values continued to increase, the system seemed sustainable. But as a scene in the movie “The Big Short” illustrated using a stack of Jenga blocks, once house prices cracked, the market’s foundation crumbled.

Today, household debt ratios in many countries have declined. But sovereign debt in most countries is twice the share of gross domestic product (GDP) than it was 10 years ago. In some ways, governments are better able to handle indebtedness than the private sector: their borrowing costs are lower, they have substantial assets that can be monetized

and they can print money. On the other hand, politics can make it very difficult to reduce

debt once it begins to accumulate.

To date, a vigorous global appetite for sovereign debt has absorbed the increased issuance. But central banks are beginning to reduce their ownership of government bonds, and worries over debt sustainability have periodically pushed smaller countries into crisis. It would not be that hard to imagine concern spreading one day to a much bigger country, with more substantial global linkages. The next crisis could very well be centered at that level.

Fiscal authorities around the world should respect this risk, and take steps wherever possible to limit their footprint on the world’s debt markets. And regions with lingering property price excess (like Canada and Australia) must take careful action to avoid a re-run of 2008.

Focus on Financial Stability

Lehman’s failure revealed a series of linkages between markets and institutions that had not been well understood. As an example, Iceland is a long way from Florida, so you might not expect that an American real estate crisis would reach the Arctic Circle. But Icelandic banks held substantial amounts of MBS, drawing them into the downward spiral.

Firms interacting with one another often require collateral as security. Financial exchanges and clearing houses require the maintenance of margin in their terms of membership. MBS were widely used for these purposes in 2008; almost overnight, the values of these assets came under serious question. Calls for additional margin and collateral forced firms to sell their best assets, creating unexpected contagion across markets. Investors speculated on which firms were most exposed, and limited their access to liquidity. That, ultimately, is what proved fatal for Lehman Brothers.

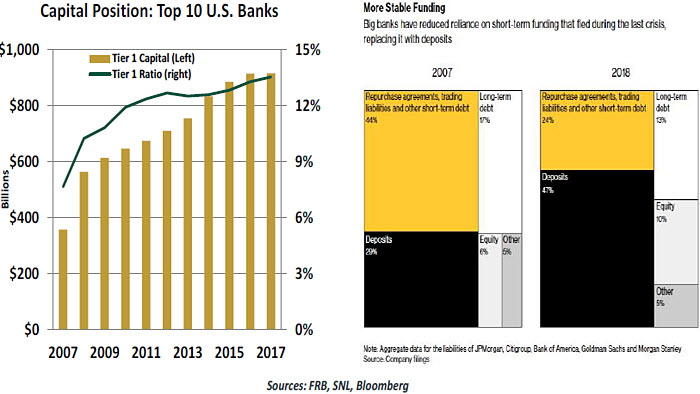

Lehman, like other investment banks, had little capital to guard against its fate. In early 2008, the firm’s ratio of leverage to equity was 30 to one. Commercial banks were a little better off, but still did not have enough capital to absorb the losses that seemed likely to emerge.

In the years since, financial supervisors have responded in two ways. Capital standards have been tightened, and are now based on annual stress tests that examine worst-case scenarios. The top U.S. firms now have twice as much high-quality capital as they did in 2007. And new international liquidity standards have reduced reliance on short-term

funding that can flee under duress.

Further, more interbank transactions are now handled by exchanges, which are easier to govern and far more transparent. Importantly, the volume of bespoke financial instruments of all kinds has diminished in the last decade.

To keep watch over the system, the Fed, the Bank of England and the European Central Bank (ECB) have chartered financial stability departments. This should provide some reassurance, but central banks don’t have a good track record in identifying financial excess. And financial supervision is still spread across a broad range of agencies and jurisdictions that don’t always cooperate with one another. Some additional consolidation, at least on a regional level, would be highly desirable.

Lingering Bitterness

In retrospect, I find it amazing that decisions made under terrible pressure, with limited information and by policymakers who hadn’t slept, proved so effective. To be sure, the rules were stretched to their limits, but the results are compelling. Most of the emergency programs made money for U.S. taxpayers, and savers worldwide avoided devastating losses. The global expansion and bull market that began in the spring of 2009 would not have been possible without policy that was big, bold and lasting.

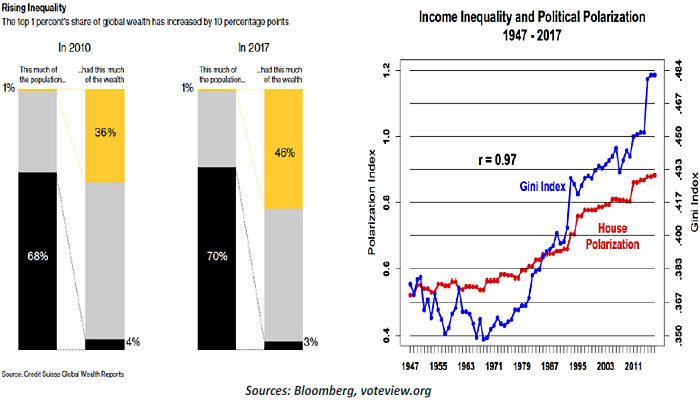

Nonetheless, some people remain angry over what they see as a bailout of bad actors. Firms did fail as the recession spread, and millions of people worldwide endured long stretches of unemployment. The rapid recovery of banks stood in stark contrast to the fortunes of many and engendered antipathy that is as fresh for some today as it was 10 years ago. This is one of the frustrations that contributed to the rise of populism in many countries.

Channeling this sentiment, the U.S. Congress passed the Dodd-Frank Act in 2010, which reduced the Fed’s discretion to deal with stressful situations. That may have been viscerally satisfying, but it will certainly slow the ability of authorities to react when the next emergency arises. The international coordination and assistance that was part of the rescue effort in 2008 might be much more difficult to engineer today. When the next crisis arrives, the world’s ability to address it will be more limited.

Despite the controversy, the response to the global financial crisis was career-defining and immensely gratifying for those involved. That said, I would prefer not to have that kind of experience again.

Giving Credit

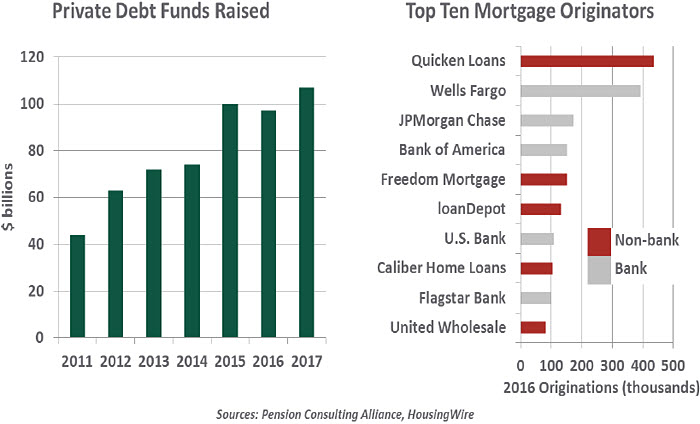

Recovering from the global financial crisis required banks to rapidly change their business profiles. They needed to increase capital cushions, and managers prioritized stability over growth. While this turnaround was underway, consumers and businesses seeking loans found themselves with fewer options. Non-bank lenders emerged to meet this demand and serve a profitable market. As alternative lending has expanded, some have asked whether it represents renewed risk to the financial system.

Well-heeled institutional investors developed the private lending market as an alternative to equity and hedge fund investments. Direct lending offered investors stability, higher yields than most bond portfolios and diversification from more volatile equity markets. A study by the Alternative Credit Council sized the private debt market at more than $600 billion in 2017 (growing from $150 billion 10 years before), of which $217 billion was “dry powder” ready to lend.

Business owners now have many more options to raise equity, as well. Private equity availability has grown at all stages of a business, from angel funds and incubators that invest in smart ideas to buyout funds that allow owners to sell their businesses.

Entrepreneurs can also turn to crowdfunding to launch a product, effectively accepting advance orders to test the market and fund its production before taking on the full cost of development.

Leveraged loans have also grown as a source of debt to commercial borrowers. In these structures, a company with a below-investment grade credit rating issues debt, offering company assets as collateral. The demand for these bonds has been strong as investors have searched for yield in a low-rate environment.

Consumer debt has also been disrupted by financial technology (fintech) companies that recognized the credit gap and swooped in to serve these markets. Some fintech firms were backed by private equity, giving investors an opportunity to make returns through consumer lending. Others positioned themselves as marketplace lending platforms, connecting credit seekers with a wide assortment of funders, from individual consumers to pension funds.

Fintech lenders have several advantages in their business models. Most of them are not chartered as banks. Avoiding banks’ regulations, examinations, capital requirements, branch networks and legacy technology allows fintechs to operate efficiently. Their web pages and apps are modern and user-friendly. And they can evolve with their customers’

needs, such as initially offering unsecured installment loans and growing into products like

mortgages and financial advice.

Fintechs have altered the mortgage origination business, as well. Direct-to-consumer lenders gained share in the recent interval of low interest rates, offering competitive refinancing rates. The fintechs’ tactic has paid off: Quicken Loans has become the highest-volume mortgage originator, exceeding conventional banks.

Mortgage brokers acquired a very bad name during the crisis, but the agency problems associated with this channel have been reduced. Mortgages must meet much tighter underwriting criteria to be sold to Fannie Mae and Freddie Mac (which themselves have been reformed through government conservatorship).

A common theme for all of these new financing vehicles is a lighter regulatory regime than banks face. While investors appreciate the efficiency of lighter compliance requirements today, the cost of a recession may cause much greater pain tomorrow. We find some comfort in the source of funding. Private equity investors place bets with their own wealth, and this “skin in the game” heightens their risk management. If a deal goes bad, the loss is limited to those investors. Private equity funds do not trade like stocks or securitized debt and are less likely to cause contagion. However, self-regulation only works until an incident exposes a weakness. An eventual increase in regulation of these new entrants will create a level playing field with banks and will protect consumers and investors alike.

We believe these shifts in lending and funding are permanent, structural changes to the economy. Unlike the conditions that led to a crisis, however, we believe risks have been managed well in these markets.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2018 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/disclosures.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All