Global equity markets rallied on Monday after major networks declared Joe Biden the winner of the US presidential election, and early analysis of a COVID-19 vaccine from a large US drugmaker showed promising results.

A Joe Biden presidency, checked by a Republican-controlled Senate, may be just what emerging-market investors are looking for.

Recent research shows how fixed annuities can add value in the context of retirement income. In addition to being able to guarantee income for life, tax benefits are often advertised as a key advantage of using annuities. This article discusses the mechanics of tax deferral in annuity products.

I want to discuss a recent WallStreet Journal article by Ruchir Sharma entitled “The Rescues Ruining Capitalism.” We talk much about the bailouts and stimulus programs related to the economic shutdown and pandemic. However, the bailouts began back in 2008 when the Federal Reserve intervened with the insolvency of Bear Stearns.

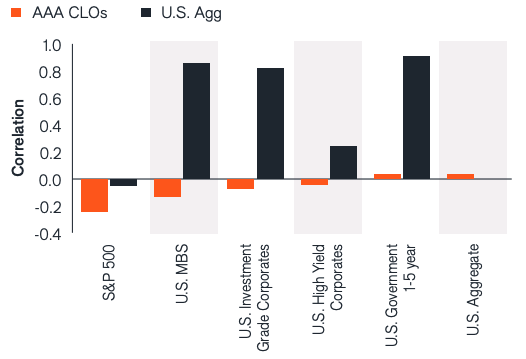

In an environment where interest rates are low and the risk of higher Treasury yields has risen, Portfolio Managers from Janus Henderson Investors discuss how allocations to AAA rated CLOs may help investors diversify a traditional fixed income portfolio, offering lower volatility, higher credit-quality and less sensitivity to any rise in interest rates.

As Mr. Valuation, I find myself constantly reminding investors that value investing requires patience. However, value investing also requires the willingness to get your money in front of attractive valuation when it is discovered. Trying to time your purchases perfectly can just as easily cause you to miss out on significant gains as it is to participate in them.

A strange thing happened on the way to the biggest post-election surge in modern stock-market history. On Wednesday, while the S&P 500 was tacking on $600 billion of fresh value, most of its members fell.

Federal Reserve Chair Jerome Powell opened the door to a possible shift in the central bank’s bond purchases in coming months, saying that more fiscal and monetary support are needed as rising Covid-19 infections cloud the outlook for the economic recovery.

Reflecting on the post-election landscape, Jeffrey Gundlach expects a split government to emerge, with a Biden presidency, Democratic House and Republican Senate. That outcome explains the gains in U.S. equities this week, but stocks are now “really overvalued.”

Investors likely have many questions about the 2020 election. Votes were still being counted late Wednesday, but here are answers to some of the most frequently asked questions we’re hearing.

While the election remains too close to call, investor attention will soon turn back to Capitol Hill, where senators will reconvene on Nov. 9 and House members on Nov. 16 for what is known as a “lame duck” session of Congress.

The post-pandemic world is charging into change. Trends that were in play prior to the onslaught of COVID-19 have been accelerated, and many of the companies that were already leading the charge are emerging supercharged.

History does not repeat, but it rhymes, as Mark Twain observed. As such, we are struck by the eerie and dangerous parallels between today’s markets and the markets back in 1999. Back then, Value investing and Value managers were under the gun for having underperformed their Growth brethren for too long.

There are many major policy decisions that will influence the outlook—trade, energy, taxes and budget deficits, and pandemic relief. However, it’s difficult to assess how these issues will be addressed post-election, and even more unpredictable how the market will react.

Key takeaways for investors amid the tightening race for the White House and control of the Senate.

Just hours before the U.S. election got underway, investors pulled the most cash ever from the world’s largest exchange-traded fund tracking corporate bonds.

So… who is right? Can we learn from history, as Santayana believes? Or has the past just set the table for what’s to come, as Shakespeare wrote? Is the future determined by the past, as Vonnegut argues? Or are the two unrelated, as the SEC requires fund managers to tell their prospective investors? We suggest that the answer to all of these questions is yes.

When you run an equity portfolio which is concentrated in 25-30 common stock selections, there are usually three stocks which stick out as particularly attractive at any given time.

BlackRock bond experts reveal the top themes driving our fixed income outlook. Learn the latest key risks and opportunities in today’s bond market.

The roller-coaster ride of 2020 still has a few twists and turns to navigate. But the massive policy response to the COVID-19 pandemic brought a quick, though incomplete, recovery. With volatility expected to continue, where can investors look for opportunities?

Want to hear something really scary? Inflation, the scourge of the modern economy, may be running much faster than we’re led to believe.

Head of Equities Stephen Dover joined Templeton Global Macro’s Katie Klingensmith and Fiduciary Trust Company International’s Gene Todd for a discussion about what they are keeping an eye on as investors.

I present data and observations highlighting how dividends can protect investors from inflation and market volatility. While this is relevant to other applications, I focus on retirement income.

Our election 2020 coverage concludes with a look at the nation’s physical and human capital.

Today I want to look at what will not change. And though I will make a few comments on the election below, I want us to think today about what we can look forward to with an optimistic and realistic vision.

Our Head of Equities, Stephen Dover, and Western Asset’s CIO, Ken Leech, believe global stimulus and the likely longer availability of zero or negative interest rates will support the path to growth in 2021. And China will continue its growth path to becoming a bigger part of the global financial community.

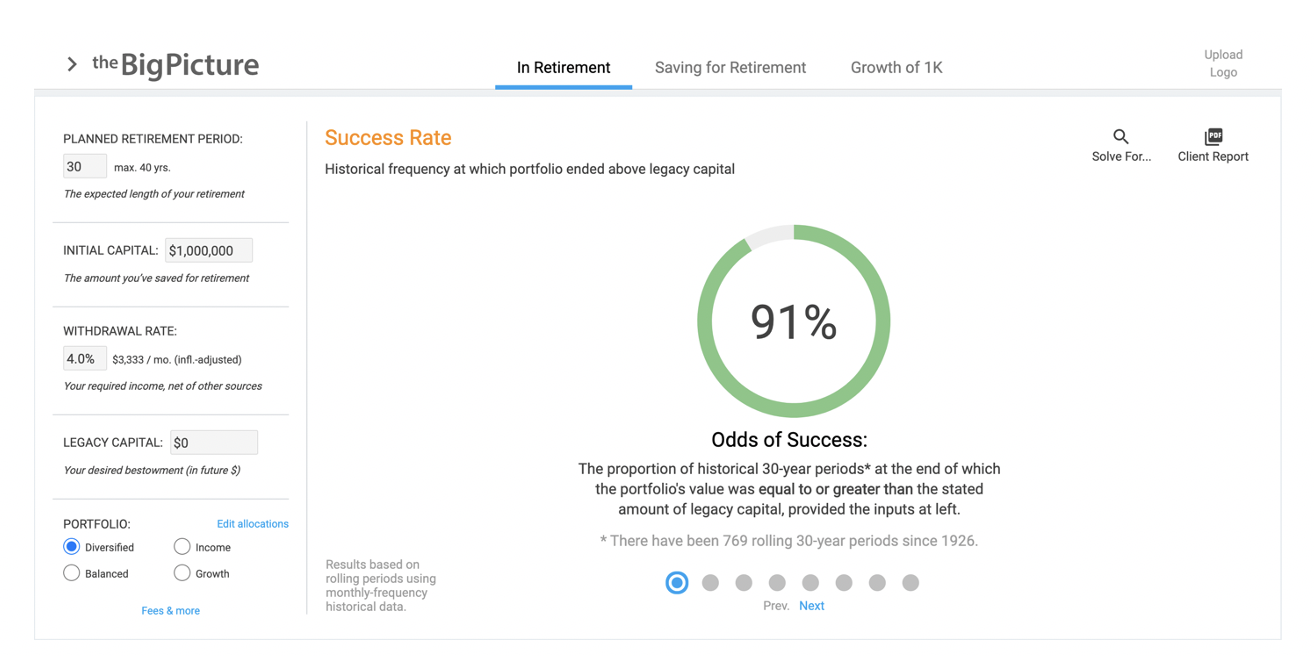

Bill Bengen’s research calculated how much a retiree can take out safely from a generic portfolio over 30 years without running out of money. Wouldn’t it be nice if you could take a prospective client’s asset allocation and calculate the percent of time periods since 1926 that it would have survived a 30-year retirement?

Stocks tumbled again on Wednesday, as worries about rising COVID-19 cases and hospitalizations sent investors toward the safe havens of U.S. Treasuries and the dollar.

The relative calm we feel in the markets right now isn’t the end of the storm, it is just the eye.

The African continent is warming quickly, and climate change is expected to disproportionally affect every aspect of life there, from human health to food security and economic growth, according to the World Meteorological Organization’s first-ever State of the Climate in Africa report.

The tightrope walker has his blindfold off, the wind is blowing, and it’s a long way down. Technically speaking, high-yield bond prices broke downward through a “double bottom,” which could reasonably be taken as an indicator of coming trouble for the stock market as well, given the greater wariness among bond market investors this year.

The primary goal of this article is to explain what makes dividends different. Dividends provide investors with a growing stream of income that is largely independent of market volatility. On balance, dividends are a powerful financial planning tool many retirement models seem to neglect.

Corporate bonds are riskier than Treasury securities. The reward for accepting this risk is larger when spreads widen, but may be less than investors expect when spreads are modest.

There are a number of uncertainties heading into the November 4 election and many more as we look ahead into 2021. There’s a long held belief that the stock market abhors uncertainty. There’s also an old adage that says the market often climbs a wall of worry.

The coronavirus pandemic has created many challenges for individuals, businesses and governments around the world. In Europe, there’s a new vehicle to help finance the economic recovery there—social bonds. David Zahn, our Head of European Fixed Income, discusses this exciting new bond issuance, earmarked for funding employment initiatives.

As Prime Minister Suga begins his administration, the message is one of continuity, but Abenomics may need a reboot after COVID-19. We examine what Suganomics may mean for Japan.

The message from the bond market after the latest brief leap in yields is clear: The Federal Reserve is standing by to prevent an alarming increase in rates, no matter how much debt the Treasury sells amid the pandemic.

The hunt for new hedges is in full gear.

Canada’s central bank looks to evolve its policy framework amid concern over disinflationary trends.

Markets have continued to rally despite the ongoing economic impact of the pandemic and the uncertainty of the upcoming U.S. election. We’re expecting increased volatility in the near term, and we think a cautious approach is the best course of action.

Scott Minerd, Chairman of Investments and Global CIO, discussed his outlook for markets and the economy with CNBC’s Brian Sullivan during the Milken Institute 2020 Global Conference.

U.S. Treasury bonds are not likely to repeat their spectacular performance as income-producing risk reducers in portfolios of the past four decades. While bonds still have an important role to play in some settings (e.g., liability hedging for retirement plans), we believe investors should look at alternatives for diversification, including inflation-protected securities, gold, defensive currencies and stocks and option protection.

Emerging-market debt has rebounded sharply off March lows, but attractive yields and compelling opportunities persist. We provide a roadmap for what may lie ahead.

Markets continued their recovery during the 3rd quarter, but the narrative transitioned from concerns about the pandemic to the U.S. election – a trend that we expect to continue in October. The outcome will likely have a material impact on both fiscal stimulus policies and Treasury yields.

We have a light economic calendar with a focus on housing. There are continuing political and pandemic stories that could dominate the news cycle at any time. For those focused on financial markets, earnings season might provide answers to important questions.

The Federal Reserve and other central banks will eventually discover that breaking up isn’t easy after partnering with their governments and the financial markets to avert a pandemic-driven depression.

Here in the U.S., I estimate that the actual number of people infected by SARS-CoV-2 to-date is currently just over four times the number of reported cases. Actual cases are undercounted partly because, based on very large-scale, unbiased testing, roughly 45% of people who acquire SARS-CoV-2 infection are asymptomatic.

Key Takeaways

It is a given that you should never mention the “R” word. People immediately assume you mean the end of the world: death, disaster, and destruction. Unfortunately, the Federal Reserve and the Government also believe recessions “are bad.” As such, they have gone to great lengths to avoid them. However, what if “recessions are a good thing,” and we just let them happen?