Nov 3, 2020

Now that Election Day is here, many investors are wondering what the outcome will mean for the bond market. There are many major policy decisions that will influence the outlook—trade, energy, taxes and budget deficits, and pandemic relief. However, it’s difficult to assess how these issues will be addressed post-election, and even more unpredictable how the market will react.

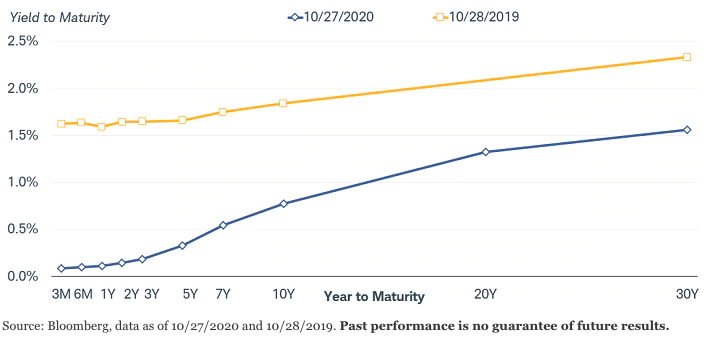

Consequently, we would avoid making any major changes to fixed income portfolios based on the elections, but we will be keeping a close eye on the fiscal stimulus talks because those have the potential to have the biggest influence on the bond market. In general, we believe it’s likely that some sort of fiscal aid package will be passed after the election, but the size, timing and specifics are up in the air. To some extent, the upward trend in long-term bond yields over the past few months and steeper yield curve suggest that the market has already begun to price in some improvement in the economy during 2021.

Treasury yields are lower, but the curve is steeper

Instead of focusing too closely on the uncertainties ahead, we suggest focusing on the factors that we can assess with some certainty. Federal Reserve policy is one of those factors. The Fed has indicated very clearly that it a) will keep its policy rate near zero until inflation rises and/or the unemployment rate returns to pre-pandemic levels; b) has put in place programs and facilities to help support markets; and c) is planning to continue its bond-buying program.

With the Fed anchoring the federal funds rate near zero and expanding its balance sheet, our view is that interest rates are likely to remain lower for longer. There may be a modest rise in 10-year Treasury yields toward the 1% region on the back of a fiscal stimulus package, but it will likely be limited by ongoing low inflation and Fed policies.

Look for coupon income—cautiously

With yields near zero or negative in many markets and likely to remain that way for at least a few years, bonds with higher coupons may become more attractive. We suggest investors focus on earning current coupon income while protecting against unexpected risks, such as another downturn in the economy or inflation. Coupon payments can provide a degree of certain income, barring a default.

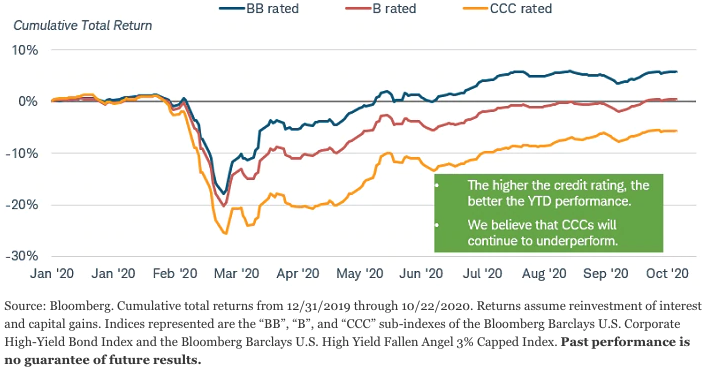

Highly rated investment-grade corporate and municipal bonds with lower risk of default or downgrade should fare better in an uncertain economy than riskier bonds with below-investment-grade ratings. Some exposure to high-yield corporate bonds may be appropriate for a small allocation, but we would suggest avoiding the lowest-rated bonds within the high-yield market. To date, bonds rated BB and higher have performed much better than lower-rated bonds, a trend we believe is likely to continue.

Higher-rated high-yield bonds have outperformed

Similarly, in the municipal bond market, we favor keeping the bulk of a portfolio in bonds rated AA or higher. The elections could result in policies that aid lower-rated bonds, but we don’t believe it’s wise to speculate on how policy may evolve for lower-rated issuers. On the surface, higher tax rates should be supportive to municipal bond prices, but tax policy proposals made on the campaign trail are often changed when the legislation is drawn. Taxable municipal bonds might also be attractive for some investors because the average credit quality tends to be higher than in the corporate bond market, while yields are similar.

For investors with a higher risk tolerance, an allocation to emerging-market bonds and preferred securities can help increase current income and potential returns. However, we would limit the amount allocated to these more aggressive asset classes to no more than 20% of an overall portfolio.

Stay adaptable

While we believe our “up in credit quality” strategy should help reduce volatility for investors, there is still potential for unexpected negative surprises. We can’t entirely eliminate risk, but we can take steps to mitigate risks ranging from the potential for a double-dip recession to surging inflation. Our view is that it makes sense to hold some Treasuries to mitigate the risk of an economic downturn or steep drop in stock prices and also some Treasury Inflation-Protected Securities (TIPS) to hedge the risk of inflation.

In sum, the elections are likely to create short-term volatility, but we suggest trying to ignore the noise. We’re staying focused on the Federal Reserve because it has such a major influence on the bond market, and looking for opportunities to generate income while mitigating risk. When times are uncertain, holding a broadly diversified portfolio can be one of the smartest strategies for investors.

Important Disclosures:

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision.

All expressions of opinion are subject to change without notice in reaction to shifting market or economic conditions. Data contained herein from third party providers is obtained from what are considered reliable sources. However, its accuracy, completeness or reliability cannot be guaranteed.

Past performance is no guarantee of future results and the opinions presented cannot be viewed as an indicator of future performance.

Indexes are unmanaged, do not incur management fees, costs and expenses and cannot be invested in directly. For more information on indexes please see www.schwab.com/indexdefinitions.

Diversification strategies do not ensure a profit and do not protect against losses in declining markets.

The policy analysis provided by the Charles Schwab & Co., Inc., does not constitute and should not be interpreted as an endorsement of any political party.

Fixed income securities are subject to increased loss of principal during periods of rising interest rates. Fixed-income investments are subject to various other risks including changes in credit quality, market valuations, liquidity, prepayments, early redemption, corporate events, tax ramifications and other factors. Lower-rated securities are subject to greater credit risk, default risk, and liquidity risk.

International investments involve additional risks, which include differences in financial accounting standards, currency fluctuations, geopolitical risk, foreign taxes and regulations, and the potential for illiquid markets. Investing in emerging markets may accentuate these risks.

Tax-exempt bonds are not necessarily suitable for all investors. Information related to a security's tax-exempt status (federal and in-state) is obtained from third parties, and Schwab does not guarantee its accuracy. Tax-exempt income may be subject to the alternative minimum tax. Capital appreciation from bond funds and discounted bonds may be subject to state or local taxes. Capital gains are not exempt from federal income tax.

Treasury Inflation Protected Securities (TIPS) are inflation-linked securities issued by the U.S. government whose principal value is adjusted periodically in accordance with the rise and fall in the inflation rate. Thus, the dividend amount payable is also impacted by variations in the inflation rate, as it is based upon the principal value of the bond. It may fluctuate up or down. Repayment at maturity is guaranteed by the U.S. government and may be adjusted for inflation to become the greater of the original face amount at issuance or that face amount plus an adjustment for inflation.

Preferred securities are often callable, meaning the issuing company may redeem the security at a certain price after a certain date. Such call features may affect yield. Preferred securities generally have lower credit ratings and a lower claim to assets than the issuer's individual bonds. Like bonds, prices of preferred securities tend to move inversely with interest rates, so they are subject to increased loss of principal during periods of rising interest rates. Investment value will fluctuate, and preferred securities, when sold before maturity, may be worth more or less than original cost. Preferred securities are subject to various other risks including changes in interest rates and credit quality, default risks, market valuations, liquidity, prepayments, early redemption, deferral risk, corporate events, tax ramifications, and other factors.

Source: Bloomberg Index Services Limited. BLOOMBERG® is a trademark and service mark of Bloomberg Finance L.P. and its affiliates (collectively “Bloomberg”). BARCLAYS® is a trademark and service mark of Barclays Bank Plc (collectively with its affiliates, “Barclays”), used under license. Bloomberg or Bloomberg’s licensors, including Barclays, own all proprietary rights in the Bloomberg Barclays Indices. Neither Bloomberg nor Barclays approves or endorses this material, or guarantees the accuracy or completeness of any information herein, or makes any warranty, express or implied, as to the results to be obtained therefrom and, to the maximum extent allowed by law, neither shall have any liability or responsibility for injury or damages arising in connection therewith.

The Schwab Center for Financial Research is a division of Charles Schwab & Co., Inc.

(1120-0V86)

© Charles Schwab

Read more commentaries by Charles Schwab