Everybody is familiar with the phenomenon of the eye of the storm, that small zone of calm in the dead center of a hurricane’s swirling fury. The wind and rain at the edge of a storm is slower and gains in intensity towards the middle, but right in the eye it seems like there is no storm at all. When you are in the eye of the storm, you could walk outside and feel completely safe. Yet the worst is still to come. As the storm progresses and the wall on the other side of the eye hits, it doesn’t build from the edge but slams immediately at full force.

After suffering through a brutal economic and market storm since March, we are experiencing what seems like a break in the weather. Market volatility is down, and the economy has begun to recover, faster than almost anyone expected at the outset of the pandemic and the economic shutdown. Credit spreads have tightened but are still cheap on a historical basis, stocks recovered but have recently fallen from fresh all-time highs. We have seen some extremely strong economic numbers, although these reflect more a retracement from a historically swift and steep drop rather than intrinsic growth.

Video

Scott Minerd discussed his outlook for markets and the economy with CNBC’s Brian Sullivan during the Milken Institute 2020 Global Conference.

Do not be mistaken. The relative calm we feel right now isn’t the end of the storm, it is just the eye. The market’s performance and the economy’s recovery is calm compared to the volatility of March and April, but several issues concern me as the eyewall approaches. The possibility of a stimulus package getting passed before the election is remote, despite Federal Reserve (Fed) Chair Powell’s extraordinarily direct call for more fiscal stimulus to avert economic disaster. Without fiscal stimulus, personal income will stagnate, job gains will slow, consumers will pull back, and more small and medium-sized businesses will fail. The economic fallout from lack of fiscal actions increases the likelihood of a negative fourth quarter gross domestic product (GDP) print while Main Street remains in depression.

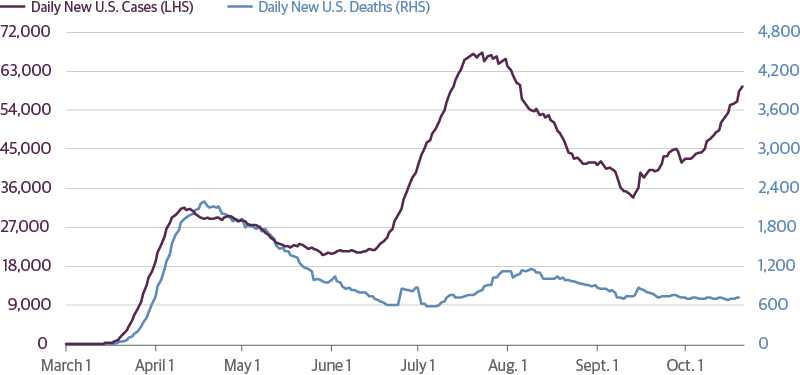

At the same time, COVID-19 is resurging, which will further test our healthcare systems, our economy, and our nation’s resolve. Over the past week, daily new cases averaged 60,000 versus the recent trough of 36,000 in early September. As we head into the winter flu season, more indoor activity will likely cause cases to accelerate more, echoing the 1918 pandemic.

A Second Wave of COVID-19 Infections Could Dwarf the Initial Crisis

Source: Guggenheim Investments, Bloomberg. Data as of 10.20.2020.

There is also considerable uncertainty surrounding the upcoming presidential election. From a macroeconomic perspective, I am not overly concerned that a Trump victory or a Biden victory will be better for the economy, because either administration will likely push for more stimulus next year. However, a surge in mail-in voting is sure to cause legal challenges in the context of high political polarization. As such, the risk of a contested election is likely. The subsequent political chaos could cause a sharp tightening in financial conditions, and a pullback in consumer spending and business investment due to the spike in uncertainty—a terrible outcome for our country at this stage of the recovery.

Beyond the eyewall lies a poor credit environment judging by credit defaults, rating migration, and corporate fundamentals. in aggregate, the high yield market has 4.5x more debt than last 12 month earnings before taxes and other items, a ratio that already exceeds the 2008–2009 default cycle peak, and is likely to worsen from here. We have seen a record $240 billion of fallen angels in 2020, and our research indicates that we could experience another $200 billion–$300 billion by the end of 2021.

Price activity, both in stocks and in bonds, tells me that the market is coiling, a term that is associated with relatively quiet markets that are getting ready to make big moves. Equities are roughly flat from two months ago. Over the last six months the bond market has basically gone nowhere. The 10-year Treasury note has traded between 50–90 basis points since the end of March, and in dollar price terms it has stayed in a range of roughly 3 points between the low and the high.

If we are in the eye of the storm, mounting economic and political turmoil will likely cause the stock market to go lower once it breaks from its coiling range and before it can resume its rise. In the bond market, despite seasonal trends indicating rates should go up this quarter, the risk is that the next break out move in yield is down. Credit spreads would widen, but yields may fall for investment-grade credit since the Fed is physically present in this sector to prevent a complete fallout.

Ultimately the first stop for yields on the 10-year Treasury note will be around 40 basis points, and before the end of the year there is a good chance that we will see the 10-year note at 10 basis points. But even at that level, foreign capital will flow here because U.S. yields remain among the highest in the world. The euro zone is stalling out due to another wave of COVID-19, and other major economies like India and the United Kingdom are slowing down. The Bank of England is increasingly signaling openness to a negative interest rate policy, putting further downward pressure on global interest rates. The bottom line is that fundamentals and technicals are telling us the same story, which is that we are vulnerable to a significant rate decline.

Going forward, I expect there would be another buying opportunity given any pullback in risk assets. We are taking every opportunity to lock in better yield, because given the trajectory of rates, portfolio yields will gradually erode as bonds mature or get called over the next year or two. We could ultimately see a “yield” of negative 50 basis points on the 10-year note, and corporate yields in the neighborhood of 1 percent for investment-grade corporate debt. Those are levels where reinvestment risk becomes more significant.

Even with this cautionary outlook, I remind people to have more faith in the willingness and ability of our government to print money. It is now the policymakers’ preferred solution to every problem. Back when quantitative easing was getting underway during the financial crisis, it was clear that as the Fed was running out of bullets the only solution left was to print money. This is even more true today. The Fed is almost out of ammo and the most potent firepower at its disposal is still the good old-fashioned printing press. Central bank accommodation will continue to play a critical role in supporting credit availability at affordable terms. This in turn would temper the market’s default concerns and inevitably drive spreads tighter.

There will be some beneficiaries from the coming decline in interest rates, such as the housing industry and corporate borrowers, but interest-sensitive entities such as insurance companies, pension funds, and municipalities will need to prepare for this outcome and what ultra-low and negative yields signal about long-term return prospects. The eye of the storm is not a place to relax, but instead it is an opportunity to prepare for what is to follow.

Important Notices and Disclosures

This material is distributed or presented for informational or educational purposes only and should not be considered a recommendation of any particular security, strategy or investment product, or as investing advice of any kind. This material is not provided in a fiduciary capacity, may not be relied upon for or in connection with the making of investment decisions, and does not constitute a solicitation of an offer to buy or sell securities. The content contained herein is not intended to be and should not be construed as legal or tax advice and/or a legal opinion. Always consult a financial, tax and/or legal professional regarding your specific situation.

This material contains opinions of the author, but not necessarily those of Guggenheim Partners, LLC or its subsidiaries. The opinions contained herein are subject to change without notice. Forward looking statements, estimates, and certain information contained herein are based upon proprietary and non-proprietary research and other sources. Information contained herein has been obtained from sources believed to be reliable, but are not assured as to accuracy. Past performance is not indicative of future results. There is neither representation nor warranty as to the current accuracy of, nor liability for, decisions based on such information.