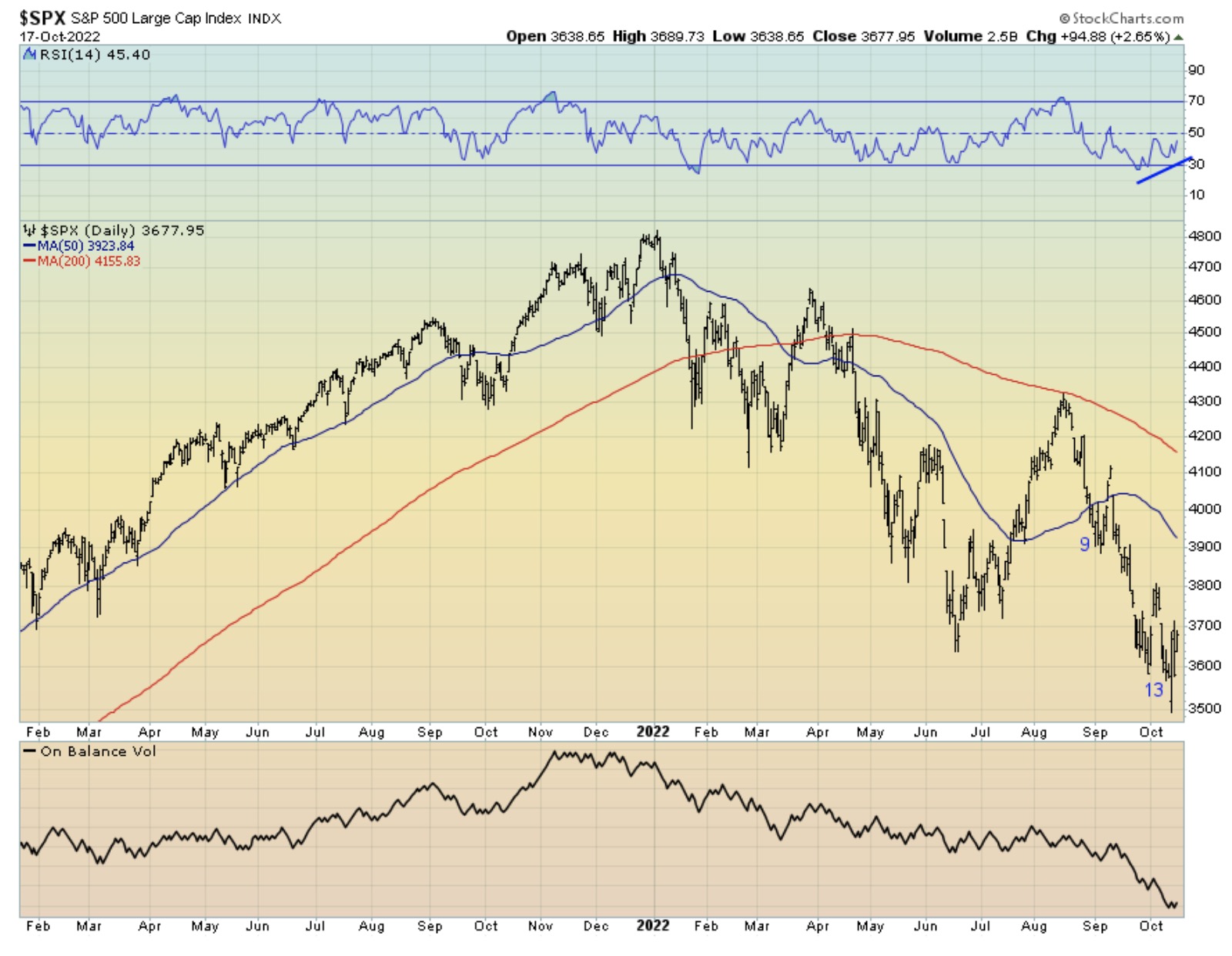

Stocks rose last week (S&P 500 +4.7%) after falling to a 2.5 year low the week before. The increase was attributable to technical and sentiment reasons, but also Q3 earnings reports coming in less bad than feared.

“Recession Fatigue” is setting in as consumers struggle under rising interest rates, high inflation, and a declining stock market.

Internal priorities and external circumstances have brought China's growth to an inflection point.

With mortgage rates more than doubling from ~3% to over 7% today the difference in cost between buying a home twelve months ago compared to today is very big.

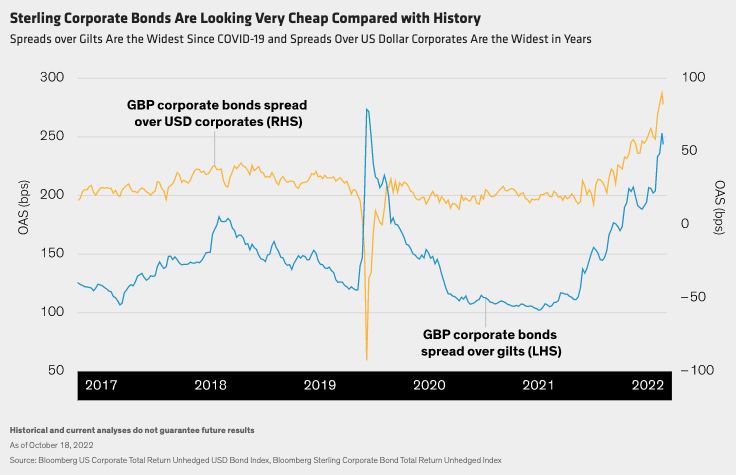

UK government bonds prices have plunged recently. Sterling-denominated corporate bonds have also fallen sharply and are looking cheap.

Key Takeaways

Macro uncertainties and tightening financial conditions are pressuring the real estate investment market. Tim Wang, Head of Investment Research for Clarion Partners, discusses the challenges and opportunities in this current environment.

Investors today probably feel a bit like the joker and the thief from Dylan’s classic, “All Along the Watchtower” – there’s too much confusion, they can’t get no relief. But our Core Equity team believes there is a way outta here – investing in dominant companies that pay growing dividends.

With this week’s announcement that the White House is deploying nearly $3 billion to boost domestic output of EV batteries and the minerals used to make them, it may be time for investors to take notice.

Treasury Inflation-Protected Securities can be a buffer against long-term inflation, but it's possible for TIPS price declines to outpace principal adjustment in the short term.

At the beginning of 2022, our most reliable stock market valuation measures stood at record levels, beyond even their 1929 and 2000 extremes. The 10-year Treasury yield was at 1.5%, the 30-year Treasury bond yield was at 1.9%, and Treasury bill yields were just 0.06%. By our estimates, that combination produced the most negative expected return for a conventional passive investment portfolio in U.S. history.

China's 20th National Congress could help air ideas for more growth-supportive policies.

In the context of a rough year so far, it's a good time to review whether this is just a bump in the road or something more serious to prepare for.

After a strong rebound from the pandemic in 2021, it’s been all downhill for the global economy this year. Economic activity is being hindered as policymakers cope with the hottest inflation in decades, impairments from the Ukraine war, and China’s prolonged lockdowns. Recession fears are starting to come true.

Much attention has been paid to the elevated risk (and announcement) of a recession, but investors should instead focus on signals coming from leading economic indicators.

Balancing financial gain and personal values can be a challenge for investors. A fund of funds approach to impact investing can help to provide the best of both worlds.

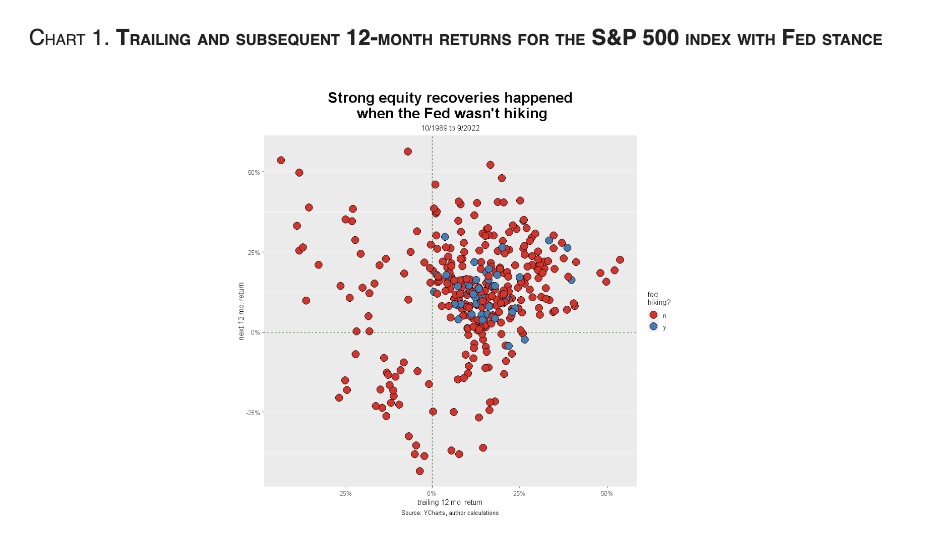

While the Fed continues to hike rates to combat high inflation levels aggressively, history shows that deflation will become a more significant threat when something “breaks” in the financial or credit markets.

If the prolonged period of declining and ultra-low interest rates is over, what does that mean future corporate profits, cash flows and dividends?

The Fed remains singularly focused on containing inflation but has made little headway so far.

The investors in the Smead International Value Fund have asked our team at Smead Capital Management what looks attractive today.

Inflation, instability, interference, these are the things that try our souls (to paraphrase American patriot Thomas Paine). They’re also the things that can make one think twice about keeping their wealth in dollars.

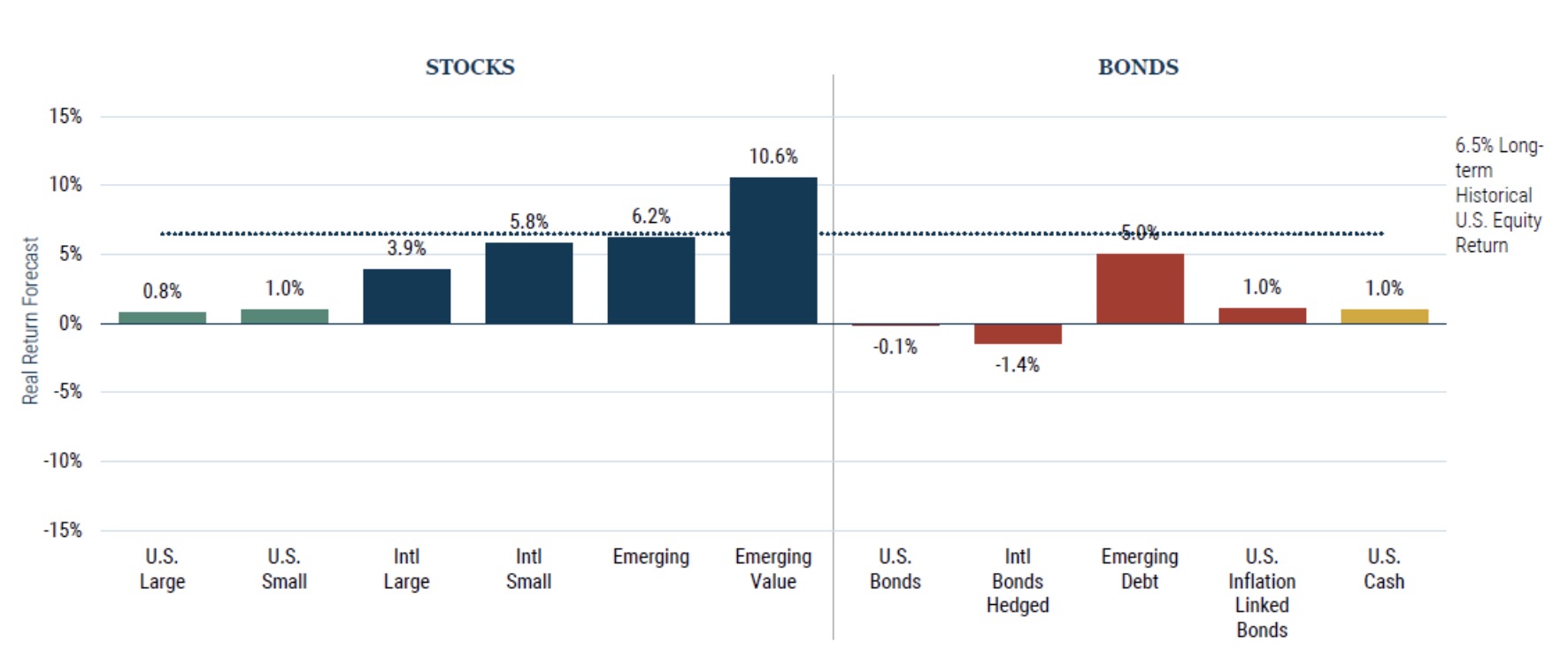

GMO 7-year asset class forecast: 3Q 2022.

The difficult capital markets saga of 2022 continued through the third quarter with few safe harbors as rates rose and growth slowed.

From an investment standpoint, aggressive regime shifts like the current one often create price dislocations as allocators restructure their portfolios, according to K2 Advisors.

While many perceive the S&P 500 Index to be a broad innovation-heavy index, in a way it is and in a way it isn’t.

When it comes to elevating the “customer experience” to improve client satisfaction and results, today’s family offices could learn a thing or two from Starbucks.

We are at the point in this nasty bear market where those who are buying the glamour tech stocks of the last ten years (on the way down) are at a crucible.

A new Money Metals client reported to us significant trouble retrieving of his silver American Eagles which were supposed to be held for him in a segregated storage account at another prominent bullion dealer.

Investors may have to wait until the Fed’s done tightening for equity market fortunes to change. History suggests that next bull market may not start until both inflation and valuations are again low.

As has been the case in recent weeks, the stockmarket finds itself in a position where various technical factors, market internals, positioning and sentiment are suggesting this sell-off may be overdone and a short-covering rally due.

The Nobel Prize in Economics was recently awarded to former Federal Reserve Chairman Ben Bernanke, as well as professors Douglas Diamond and Philip Dybvig, for their work on understanding the role banks play in the economy, especially during a financial crisis.

The world is in a very different macroeconomic position today compared to the prior forty years.

U.S. equities are beginning the new week sharply higher, getting a boost from the U.K.'s decision to abandon nearly all its tax cut plans.

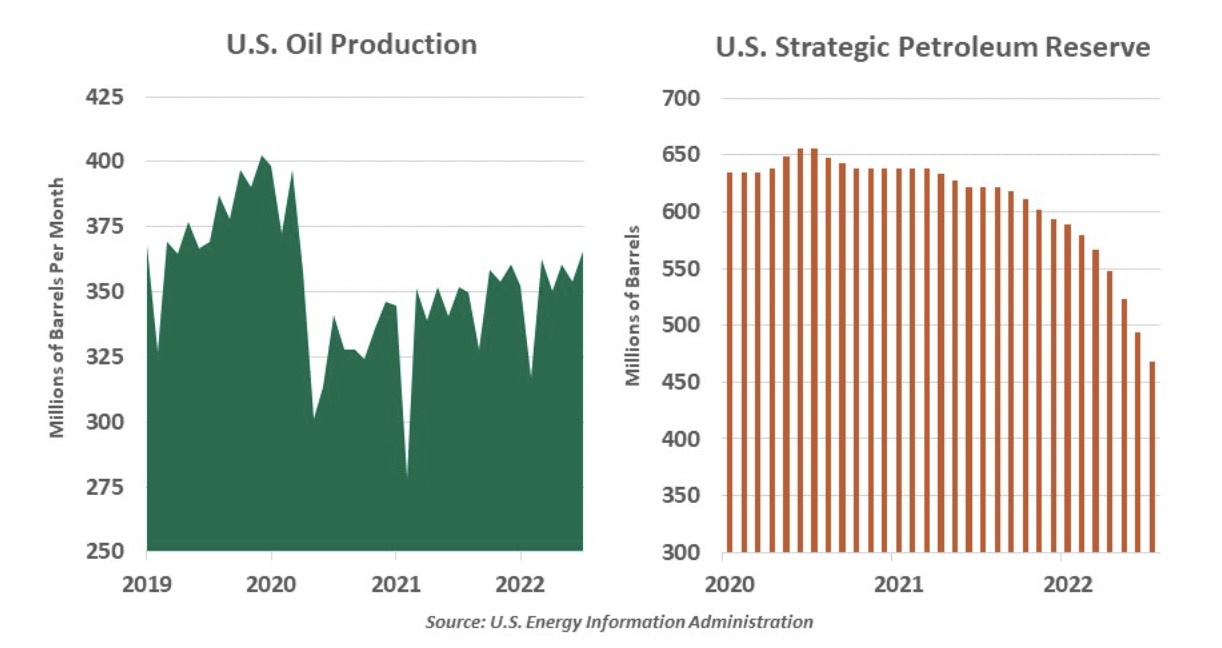

Renewed increases in energy prices come at a bad time in the battle against inflation.

Is this the “Superbubble’s Final Act?” Such was a fascinating piece of commentary recently from Jeremy Grantham, famed investor and co-founder of GMO.

Readers of a certain age will remember Carnac the Magnificent, Johnny Carson’s recurring alter ego.

In 1987, Sports Illustrated, the preeminent sports periodical of the time, predicted the Cleveland Indians would win the American League pennant in its baseball season preview.

Inflation concerns on Friday once again pulled the rug from under investors struggling to find their footing as the Federal Reserve's battle against rising consumer prices shakes the economic terrain.

S&P 500 Introduction 2022 has been a bad year price-wise for the stock market as measured by the S&P 500. However, I contend that is not enough to simply know that the market is down, it is even more important to know why.

2022 has been a stormy year for bond investors, and the forecast calls for more of the same. We address today’s biggest investment challenges—from persistent inflation to rising rates to a looming recession—the silver linings of higher yields, wider credit spreads, and strategies for navigating bad weather.

When markets are challenging, your clients look to you to help manage their expectations as well as their hard-earned money.

Millennials were more comfortable with the stock market this year, a May survey found. We explore the outlook for equities through a generational lens.

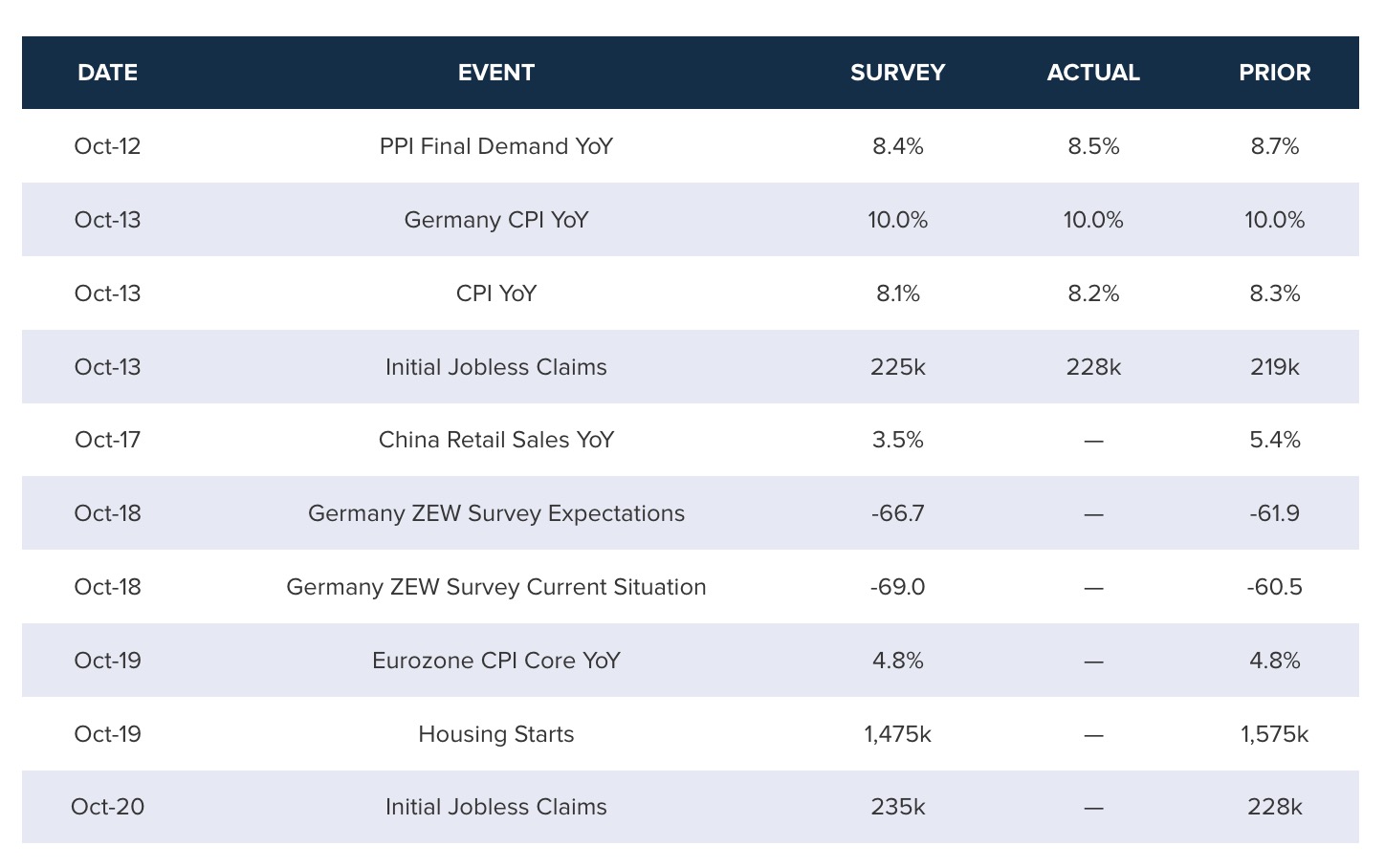

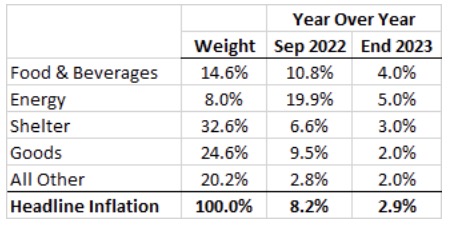

Core inflation in the U.S. outpaced expectations for September and may fortify the Federal Reserve’s hawkish resolve.

A couple of weeks ago, in our quarterly strategy report, I argued that it appeared that innovation had bottomed.

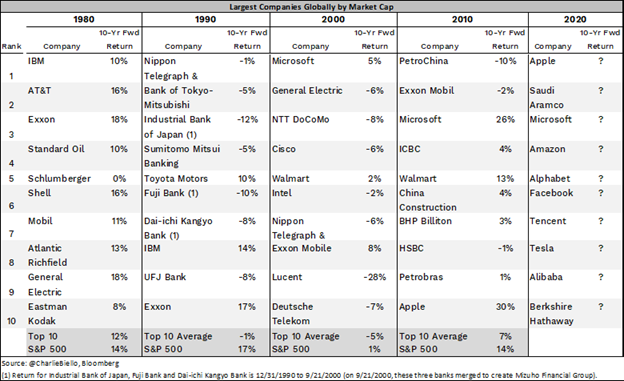

Digging in a little deeper, we sifted through this first quintile of the S&P 500 for other insights.

Is a recession lurking around the corner in 2023? If so, how might it impact defined benefit (DB) plan sponsors—and what steps, if any, should they consider taking?

Sandpiles can be fun. Nothing beats taking kids to the beach (or being a kid!) and watching their creativity blossom into all kinds of magical shapes. The problem with sand construction is it doesn’t last. I have it on good authority that building your house on the sand probably won’t end well.

As new inflation data pushes the Fed toward continuing with rate hikes, precious metals markets are struggling to make headway.

Review the latest portfolio strategy commentary from Mike Gibbs, managing director of Equity Portfolio and Technical Strategy.

You might be surprised to learn that despite the devastation, we do not expect Hurricane Ian to have a material credit impact in Florida.

The Northern Trust Economics team shares its outlook for growth, employment, inflation and interest rates.