Investors in the booming ethical bond market are having to swallow short term losses on the road to improving their green credentials.

Bond traders suspect the Federal Reserve will quickly discover it’s being too ambitious with its newly hawkish stance.

To envision the future of crypto, I keep trying different analytical tools. This time around the concept of relevance is focality, by which I mean the part of the system at which consumers direct their attention.

The dollar is on the rise, and with it comes underappreciated consequences.

The metaverse is part of the next iteration of the internet some are calling Web 3.0—and it promises to upend everything as we know it.

As the end of 2021 draws near, investors are pleased with the impressive performance posted by most asset classes, but we are still awaiting the transition to the endemic state of the virus.

Some of the market’s recent pressures are showing signs of easing.

Russ discusses the recent volatility and how to hedge the risk in the current environment.

Investors should hold off from ditching all their high-priced growth stocks for cheaper value shares as bond yields rise, at least until benchmark Treasuries yield 3%.

What might equity investors expect in 2022? Active stock picker Tony DeSpirito reviews the potential positives and impediments in his Q1 market outlook.

A renominated Powell is a different Powell. The Federal Reserve didn't raise interest rates today, a policy move we think is overdue, but it made major changes that set the stage for multiple rate hikes in 2022 and beyond.

Research Affiliates discusses the outlook for U.S. inflation expectations, and explains their business cycle model and how it informs portfolio positions.

With 2021 almost finished, it's a good time to look ahead to the key questions and themes for 2022. Overall, we believe economic growth, inflation and investment returns should moderate through 2022, but expect growth to remain above trend, which should support the outperformance of equities over bonds.

Insights from Franklin Templeton specialist investment managers Brandywine Global, Clarion Partners, ClearBridge Investments and Western Asset

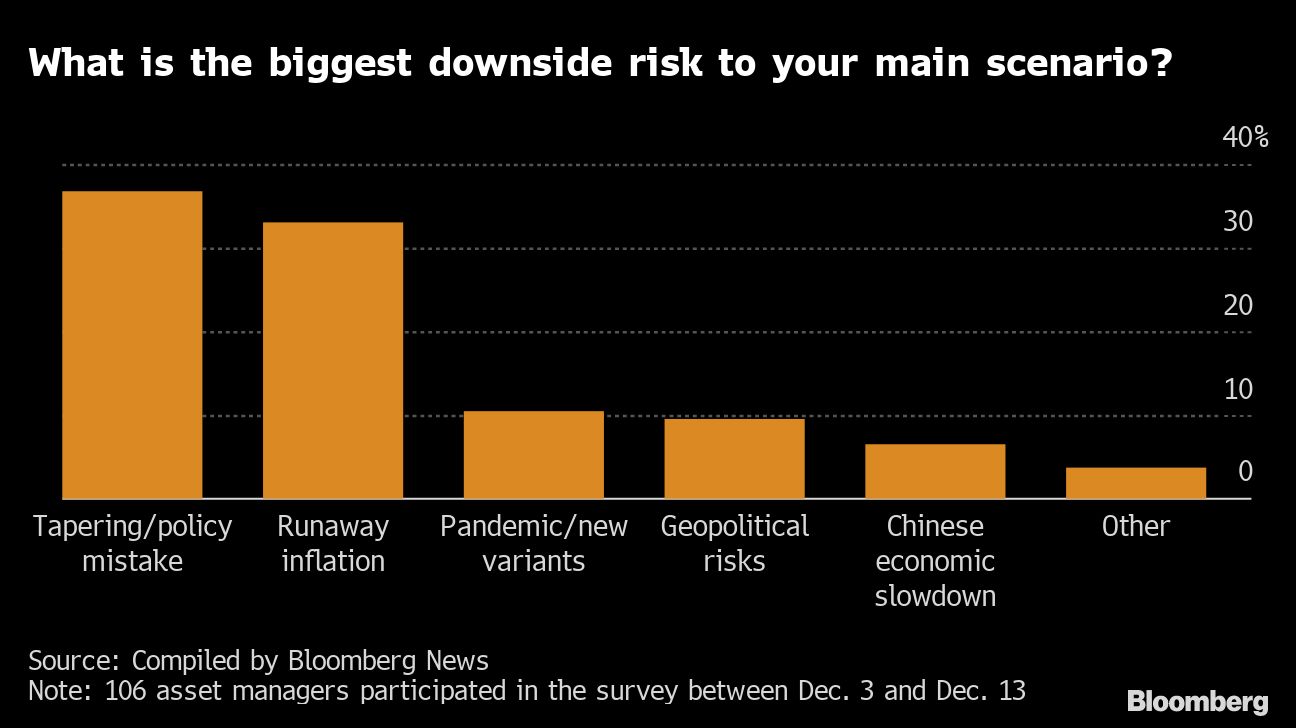

A hasty policy shift by central banks anxious to tame surging inflation is the biggest downside risk for global stocks next year, according to an informal Bloomberg News survey of fund managers.

2021 has been a year of notable economic growth after unexpected change caused by the COVID-19 pandemic. In our Economic and Market Outlook for 2022, we lay out some of the “known unknowns” we believe could significantly affect the investing landscape...

This quarterly is a piece written by my Asset Allocation co-head John Thorndike. In it, he explains the rationale behind our strong preference for non-U.S. stocks despite the stellar performance the U.S. stock market has delivered over the last decade. The research behind the piece is an example of the bread and butter of our historical asset allocation analysis.

In the depths of the lockdowns in March and April, we were together at home, day after day. The U.S. Federal Reserve Board pumped large amounts of liquidity in our economic system. The U.S. Federal Government followed by providing large amounts of fiscal stimulus in PPP loans...

If 2020 was the year we all learned about epidemiology, 2021 has taught us more than we ever wanted to know about inflation. Price rises had remained calm and controlled for four decades, ever since the U.S. Federal Reserve under Paul Volcker hiked interest rates aggressively in the early 1980s.

Whether investors are ready or not, global monetary tightening cycles are fast approaching.

Commodities, by virtue of their fungibility and broad uses, have infiltrated nearly every facet of human life, making the world enormously reliant on their ready availability.

There are a number of key investment themes for 2022 I feel most people would agree on. Below are just a handful.

Today we’ll “war game” what the Fed is facing as it wrestles with inflation, growth, employment, and political considerations. We’ll try to entertain those thoughts as if we’re sitting in the conference room with Jerome Powell.

Ever since the Federal Reserve started hinting it was planning to end its ultra-loose monetary policy, bond yields have been falling. That it happened in a booming economy with the highest inflation readings in nearly 40 years has taken a lot of investors and analysts by surprise.

Historically, fourth quarter tax loss selling of closed-end funds (“CEFs”) has been prevalent in the market. CEFs may be more susceptible to tax loss selling given they trade on a stock exchange and market prices (investor return) can deviate from underlying net asset values (“NAVs”) (fund return).

The Fed’s monetary policy has screwed Americans. Such is the basic premise of a recent Washington Times article discussing inflation.

Inflation continues to be a concern these days, and many investors are looking for investments that can keep pace with, or hopefully beat, the rate of inflation. As a result, Treasury Inflation-Protected Securities, or TIPS, have become a popular investment option.

Uncertainties that caused U.S. Treasuries to rally and yield curves to undulate in November may persist and could contribute to volatility into year-end.

So, when you think about the end of 2021, and looking forward into 2022, we’re reasonably optimistic about the backdrop. Growth should be set up pretty well for 2022.

The U.S. Treasury’s Series I savings bonds are no longer a forgotten investment option.

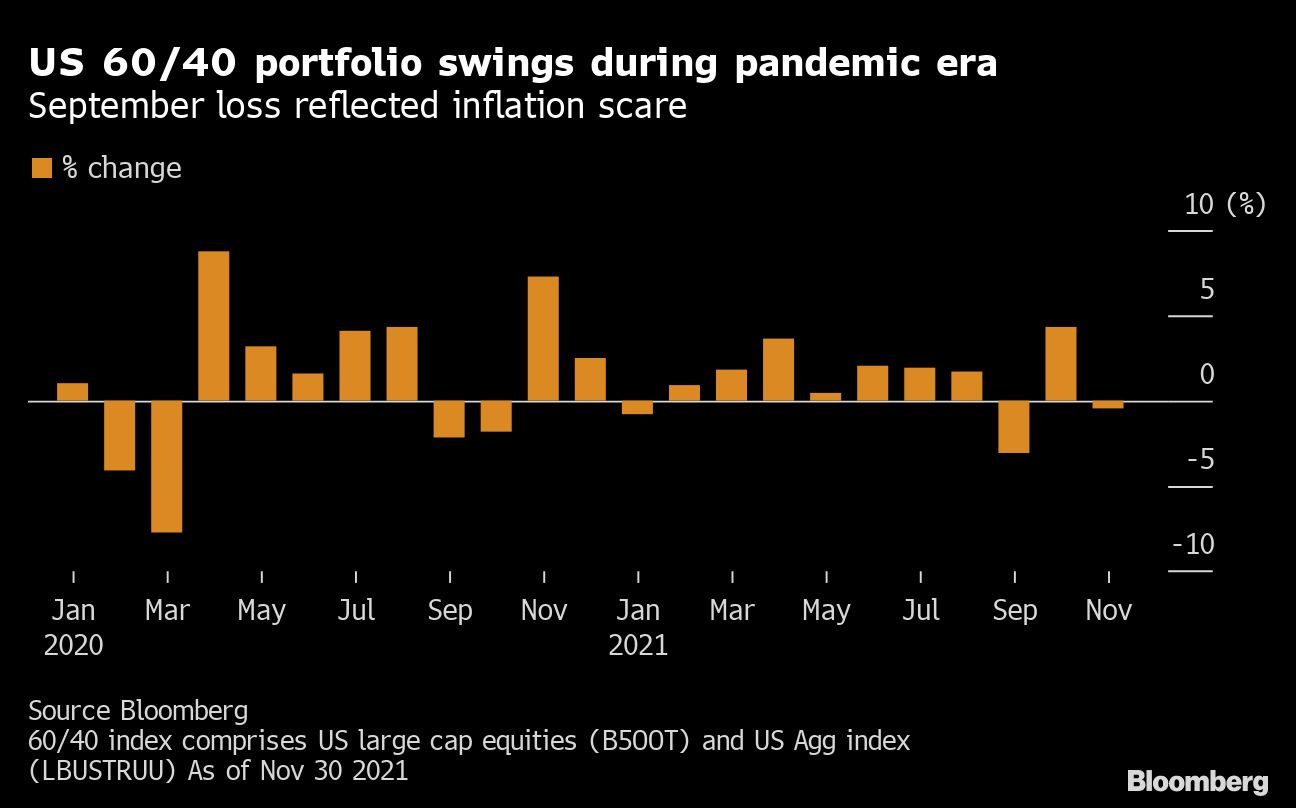

Wall Street likes to warn that past performance doesn’t guarantee future results, but when it comes to the traditional 60/40 mix of stocks and bonds, it kind of has. Persistent inflation could bring that to an end.

Inflation will stay above 4% for 2022, according to Jeffrey Gundlach, which makes Treasury bonds at yields of 1.5% to 2% overvalued.

Disruptive trends and fatter tail risks highlight the importance of selection within asset classes and regions.

After a year of rebound and recovery, we believe that economic growth, inflation and investment returns are likely to moderate in 2022.

Interest rates were mixed in November, as shorter maturity yields continued to rise while longer maturity yields fell further. The continued flattening of the yield curve reflects the market’s expectation that the Fed will be more aggressive in their tapering of official purchases and potentially raise the fed funds target rate more quickly and aggressively than previously thought.

The S&P 500 index is up more than 20% so far this year, but more than 90% of its member stocks have had “correction” level drawdowns—more than 10% from a peak—at some point this year. In short, while overall stock market performance has been strong, there has been a lot of churn beneath the surface.

Like many others, I believe Bitcoin could fix Turkey’s lira problem. And to understand why, it might be helpful to dust off a book written 45 years ago by Austrian economist Friedrich Hayek.

It appears as though we may be heading towards an inflection point in early 2022 whereby we begin to see the rate of growth continue its deceleration to the downside. Whether inflation follows suit remains to be seen, though my base case in the direction of change in inflation could surprise to the upside again in December and perhaps even January.

The deteriorating health situation in Europe threatens to send the recovery into reverse.

Bear with us as (no pun intended) you read this longer-than-usual outlook!

Rick Rieder and team examine the parallels, or lack of them, between the economy, markets and policy of the 1970s and today.

As the last wave of baby boomers heads into retirement, the need for a consistent and reliable stream of income is growing. Advisors seeking a balance between generating income and providing for future growth may want to consider income-focused model strategies.

Do you believe any advisor can become a strong salesperson?

U.S. and global stocks fell sharply Friday amid spiking fears about a new COVID variant, named Omicron, emanating from South Africa, where it’s spreading quickly. The S&P 500, Dow Jones Industrial Average and Nasdaq Composite indices closed down more than 2%, while the Russell 2000 fell nearly 4%.

In this video I present 8 undervalued dividend growth stocks with dividend yields ranging from 2.51% to 5.11%. All these companies are undervalued in what is a very overheated stock market today.

The COVID-19 crisis spurs cohesion, but fresh challenges await.

Last year, Jeremy Siegel correctly predicted the bull market in stocks, the rise in inflation and interest rates and soaring home prices. In this year’s interview, he predicts another year of good performance for U.S. stocks – and identifies the risks investors will face.

The charts and comments below are drawn from the “Clips That Matter” feature of our Over My Shoulder service. Because we know a picture is worth a thousand words, my co-editor Patrick Watson and I select a few important charts and graphics and send them to subscribers each week with some brief comments. Many say these clips are their favorite part of the service.

I hope everyone had a wonderful Thanksgiving full of family, love and laughter! Even if that wasn’t your experience, there’s still much to be grateful for.

Investors generally are still expecting above-average returns for U.S. stocks over the next several years. Meanwhile, since valuations are so high, models that have been historically accurate predicting 10-year returns point to negligible returns.