2022 Economic & Market Outlook

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsMACRO-ECONOMIC OUTLOOK

The economic and market landscapes are continuously evolving, and, as always, we suggest focusing on key market signals, which we define as:

- Economic growth rates

- Inflation expectations

- Monetary policy

- Corporate earnings growth rates

And we provide our 2022 thoughts on:

- Equities

- Real assets and alternatives

- Fixed income

At the time of writing, there are also several “known unknowns” that could significantly affect our perspective. These include:

1. The final outcome of the “Build Back Better” plan. Congress passed and President Biden signed a separate “infrastructure” bill, but the larger social spending bill known as the “Build Back Better” plan remains in flux likely until early 2022. The proposed bill contains a variety of tax, spending and regulatory issues that have the potential to dramatically affect economic growth and corporate earnings over the next several years.

2. The continuing evolution of the coronavirus pandemic and the corresponding federal-, state- and local-level responses. With the increase in vaccinations and the advent of booster shots and therapeutics, we seemed to have finally turned the corner on COVID-19. But it has proven to be stubborn, and spikes in new cases and hospitalizations in Europe and the U.S., combined with the Omicron variant, continue to hang over consumer behavior and potential consumption patterns.

3. Rising geopolitical issues between the U.S., China, Russia, Iran and Europe. Tensions are high, especially between the U.S. and China and between Russia and Europe, over a variety of issues. Probably none of the issues on a stand-alone basis will have much impact on the global economy, but the potential remains for a conflation and escalation of events that may have a disruptive effect on global growth.

Glossary found at end for terms and Index definitions.

The following is our views on the signals we can currently observe:

ECONOMIC GROWTH RATES

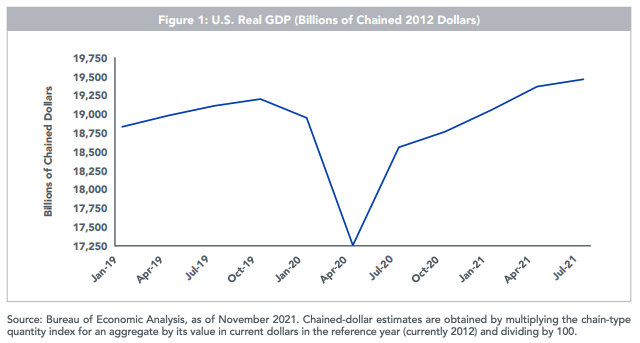

In the U.S., growth appears to be back on track to end the year after a modest deceleration in Q3. In a remarkable turn of events, real GDP has now surpassed its pre-pandemic level and is poised to build on this upward momentum. According to consensus forecasts, real GDP for 2022 is expected to expand at +3.9% for the year as a whole. However, based on current projections, the growth path may be more “front-loaded.” Indeed, H1 2022 real GDP is being estimated at +4.2% and then moderating to +2.9% for the second half of the year.

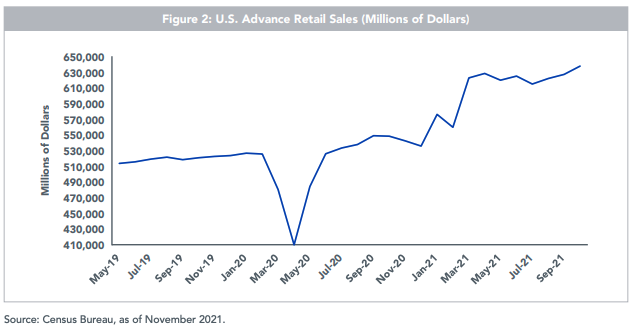

Not surprisingly, the U.S. economy has been the prime beneficiary of a relatively robust consumer sector. After plunging off the charts during the initial months of the COVID-19 lockdown, household spending came back with a vengeance, aided by unprecedented fiscal and monetary policy stimulus. In fact, according to the Census Bureau, Retail Sales surpassed its own pre-pandemic level as quickly as July 2020 and hasn’t looked back. It is no coincidence the GDP and Retail Sales charts highlighted here have that similar V-shaped look to them.

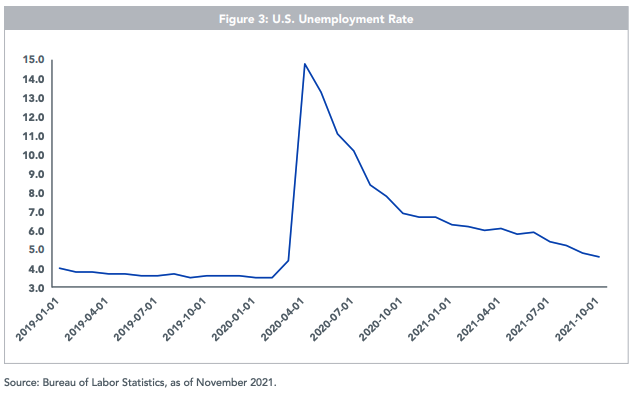

Looking into 2022, we expect the consumer to remain a solid contributor toward growth. Although the positive fiscal effects in the form of government checks and extended/enhanced unemployment benefits will fade, the labor market setting should pick up the slack and support the household sector going forward. The jobless rate has plunged to 4.6% as of this writing and, in all likelihood, appears ready to continue on this descending trajectory toward the 4% threshold.

Another key supporting influence could come from inventories. To be sure, while supply chain disruptions have received a lot of attention in terms of inflation (more on that later), their adverse impact on inventories have been less publicized. After its own pandemic-related plunge, Real Private Inventories began a relatively short-lived comeback before its latest supply chain-induced decline. In fact, the level of inventories has now fallen back to its lowest reading since 3Q 2017. As supply chain bottlenecks ease as next year progresses, we would expect to see manufacturers, wholesalers and retailers restocking their shelves accordingly

Finally, global manufacturing continues to accelerate and remains solidly above 50, marking expansion as shown in figure 5.

Investment Implications: A cautiously positive environment for “risk-on” assets, but with uncertainty caused by COVID-19, ongoing legislative discussions in the U.S. and continued geopolitical tensions.

INFLATION EXPECTATIONS

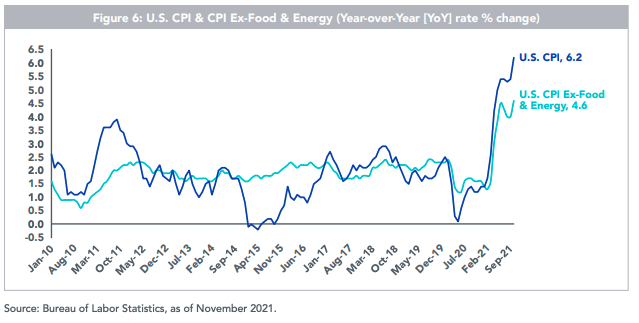

Is it transitory, is it permanent? Investors will find out in 2022 which inflation narrative comes to ultimate fruition. In our opinion, elevated price pressures are here to stay. While the October 2021 CPI print of +6.2% may not be where inflation ends up, we do feel the “final” number will still be well above the Fed’s +2% threshold.

One of the reasons for our “non-transitory” belief comes in the form of continued unprecedented fiscal spending, i.e., the bipartisan infrastructure package that has already been signed into law and the potential for an additional trilliondollar-plus spending package waiting in the wings.

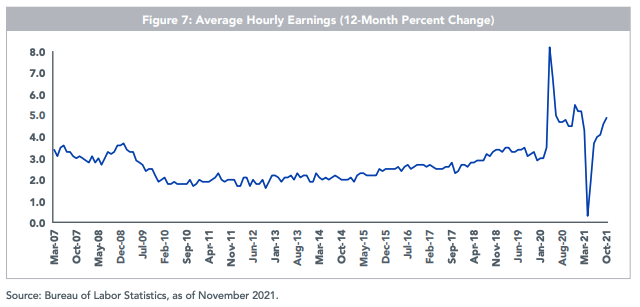

But beyond the fiscal side of the equation, a more traditional factor seems to be coming from wages. With the pandemicrelated effects now behind us, Average Hourly Earnings has revealed a definitive upward momentum in recent months, rising nearly +5% on an annualized basis and well above the trendline that existed going back to early 2007.

Another component to watch is service inflation. Until now, the run-up in price pressures has largely been a “goods” phenomenon, but service-related inflation is currently running at an annualized rate of +3.2%, its highest posting over the last five years. Combining the aforementioned factors with continued upside in wholesale prices, you get a recipe for a “stickier” elevation for the 2022 inflation outlook.

Investment Implications: We believe inflation fears will be the primary driver of investor behavior in 2021. We actively encourage advisors and investors to consider interest-rate-hedging, rising-rate and inflation-sensitive investment strategies as they consider their fixed income portfolios.

MONETARY POLICY

Was the renomination of current Fed chair Jay Powell for another four-year term a surprise to the markets? While Lael Brainard was receiving a great deal of media attention to be the next Fed chair, the announcement to extend Powell’s tenure at the helm wasn’t really that unexpected. In fact, one could arguably make the case this outcome is exactly what the markets wanted—i.e., continuity of the current Fed policy setting.

The money and bond markets have initially viewed this combination at the top of the Fed as tilting ‘hawkish’ going forward. It should be noted that Powell’s stance, especially on inflation, has apparently adapted to reality. After a relatively stubborn stance for most of 2021, Powell conceded that it was time to “retire” the term “transitory”, when referring to inflation. In fact, he acknowledged that demand pressures will probably last longer than initially thought, with the “risk skewed to higher inflation” in the Fed’s current base case. However, up until the time of writing this piece, Powell has reiterated that the “rates-liftoff question isn’t before us now,” but that could change as well.

Before we get to rate hikes, it would appear the voting members are first going to ramp-up their current pace of tapering large-scale asset purchases (LSAP). Powell has made it very clear the Fed “won’t surprise” the markets on any change in their current plans. Against this backdrop, the policymakers’ forward guidance would need to begin pivoting towards the potential for rate hikes coming sooner than the Fed initially envisioned. The bottom line is that 2022 looks to be the year when Fed rate hikes could commence as early as Q2, with expectations building for two to three increases for the year as a whole.

Investment Implications: Global central banks are beginning to “unsync” with respect to their monetary policies— this may have a significant influence on currency movements through 2021. Here in the U.S., there clearly is growing concern about being “behind the curve” with respect to inflation, and we may see a Fed response sooner than was expected even just a few short months ago.

CORPORATE EARNINGS GROWTH RATES

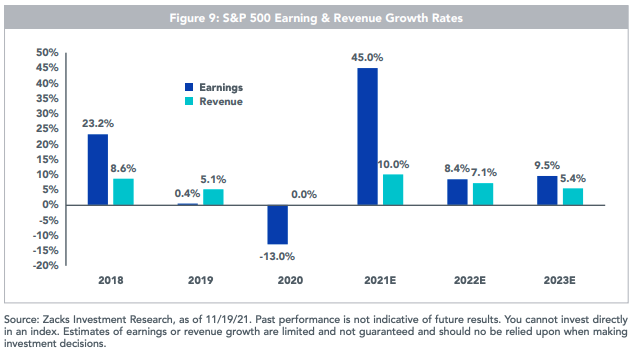

Though 2021 will mark a large leap over 2020 on the earnings front, there is not much about Street estimates for 2022 year that is particularly outlandish. For example, while strategists at Zacks Investment Research anticipate that 2021 will mark S&P 500 earnings growth of 45% over last year’s depressed levels, another increase of 8.4% in 2022 is not unreasonable. Given the Street’s wink-and-a-nod knowledge of digestible downside revisions to broad market earnings commonly occurring in many years, we do not view such forecasts as overly ambitious.

If we account for low-to-mid single-digit inflation in 2022, along with some order of real economic growth, perhaps in the 2%–3% range, the S&P 500 could witness something like 5%–7% earnings growth. However, we are hyper-vigilantly looking for wage inflation and an attendant pinch in profit margins.

Our sentiment carries over to overseas markets, with nothing particularly exciting or frightening about where the Street has landed in earnings forecasts for both non-U.S. developed and emerging markets. For example, Yardeni Research calculates MSCI EAFE earnings growing 7.0% in 2022, on top of this year’s 51.3% jump.

Perhaps more intriguingly, while the MSCI Emerging Markets Index will witness a 55.4% increase in 2021 earnings, only 5.9% is being tacked onto next year. That is only slightly higher than the IMF’s estimate of 5.1% real GDP growth for 2022. If we allow for some chunk of the IMF’s mid-2022 inflation estimate of 4% for developing economies to be absorbed by shrinking profit margins, then it is quite reasonable to expect upward revisions in emerging market earnings next year.

As we write, the nascent COVID-19 Omicron variant is hanging over the markets like a heavy cloak. We are heartened by early indications that Omicron may witness lower patient severity than the Delta variant, though time will tell if that remains the case. If so, it is possible that earnings surprise to the upside, especially in poor economies that have weak medical infrastructures.

Investment Implications: An expectation for slower earnings growth than we enjoyed in 2021, but still generally positive, and it should bode well for equities in 2022. We do believe that quality (strong earnings, balance sheets and cash flows), which has been an underappreciated risk factor for most of the past 2–3 years, may become increasingly important as we move through the year.

EQUITY MARKETS

Though the U.S. may ultimately pay penance for the multiple trillions in COVID-19 fiscal stimulus enacted in 2020 and 2021, the sheer scale of the tax credits, transfer payments, PPP, student loan deferrals¬—you name it—prevented a collapse in S&P 500 earnings last year. After falling 13% in 2020, S&P 500 earnings will leap 45% when the books are closed on 2021, according to Zacks.

Critically, because we believe stagflation is a lower probability in 2022 than some others do, we do not see anything particularly outlandish about the Street’s expectation for high single-digit earnings growth in 2022.

In fact, because the market is so used to downside earnings revisions, the S&P can behave satisfactorily next year even if earnings chop sideways.

One proviso: we assume that the Federal Reserve’s actions will not deviate materially beyond current consensus expectations for a maybe one quarter-point rate hike, maybe two, maybe three. Nevertheless, even if we allow for something like a total elimination of the central bank’s bond purchase program, the stock market can digest it. Something reasonably surprising, like four hikes, can also be tolerated in an economy that is, for all intents and purposes, at full employment.

Nevertheless, the Street will have to contend with cognitive dissonance on the matter of profit margins next year. The consensus forecast for S&P 500 earnings is $222 in 2022, which is penciled in to come courtesy of margin expansion, according to data from Refinitiv.

At 4,682, that puts the market at a P/E multiple of 21.1, with serious question marks as to how Corporate America will manage to pull off the margin coup in the face of intense wage pressure. We suspect disappointment on that front will be a dominating theme next year.

Some other obstacles abound. For one, the “TINA” trade—that “There Is No Alternative” to buying stocks in a zero-yield world—is losing its key argument. After spending much of the autumn trading in the 0.20%–0.30% range, the 2-Year Treasury note has smartly jumped to 0.59%. That is still remarkably low, especially with October’s 6.2% YoY inflation.

But it is higher than it was a few months back. TINA is not dead, but it has lost a little of its shine now that 2022 may witness friends and neighbors being able to grab 1% on a 12-month CD.

None of this need necessitate a bear market in equities, but some matters need to be dealt with. Among them: volatility is tame…for now. The reason it feels like ages since the S&P saw a pullback is because, by the market’s clock, it has been.

The only notable broad market retracement since the Q1 2020 crash was the forgettable bout of weakness in September and October. In that mini swoon, the S&P slumped from 4,536 to 4,300. Not a big deal, and forgettable.

If 2022 does bring heartache to U.S. equities, we like the WisdomTree strategies that are heavy on value and quality factors.

Going back to November 22, the day Jay Powell was given the green light to continue as Fed chair, the market responded with higher rates and a little dumping of large-cap growth stocks. If that action ends up mirroring 2022 writ large, it bodes ill for the “long-duration” equities.

There are 84 stocks in the S&P 500 that are priced beyond 10x sales, about triple the number at the peak of the dot-com bubble1 . Owning most of them has worked famously, largely because the market has been gifted 34 straight years of uberdoves running the Fed. Each of them—Alan Greenspan, Ben Bernanke and Janet Yellen before Jay Powell—had a hand in juicing equities. As Powell finally gives it a second shot at putting up rates, we believe value stocks will benefit because inflation is now so far ahead of overnight rates.

However, if some or many of those 84 stocks bring down the good with the bad, value traps will not be immune. That is why we think quality screens being run over value mandates can defend the margin pinch that is possible next year.

Turning to overseas markets, the euro and yen have been in states of freefall in the later months of 2021. Both of those currencies’ respective central banks are shouting from the rooftops that they have no intention of tightening policy in 2022, except for the European Central Bank (ECB) possibly ending its €1.85 trillion bond purchase program in Q1. As for an interest rate increase, it is not even on their radars.

Some of the GDPs of the economies in the eurozone are still south of pre-COVID-19 levels, with Spain still struggling. There is also the matter of the ECB’s purpose in the 2020s: to monetize the sky-high debt load in Spain and Italy, among others. The debt-to-GDP ratio of the latter jumped to 155.8% in 2020, up from 134.6% in 2019. We cannot figure out how it can decline.

Lockdowns in both Germany and Austria, along with some more restrictive COVID-19 measures in non-euro Scandinavian economies, are also noteworthy headwinds for the region. Cases are skyrocketing in several highly vaccinated states, making it hard for us to determine the COVID-19 restriction calendar.

Another wild card to keep an eye on in 2022: France’s elections. Current president Emmanuel Macron is in first place, though the next two candidates are both right-wing populists. Combine the support of Marine Le Pen and Eric Zemmour, and the total is greater than the ranks of those who support Macron. Those two will most certainly latch onto two issues: inflation and immigration. Keep an eye on both issues when reading the tea leaves.

In Japan, YoY inflation only turned from red to black ink in September. Fortunately, there is little prospect that new prime minister Fumio Kishida’s ¥43.7 trillion ($383 billion) stimulus program will materially spark the inflationary impulse. The largesse will, however, temporarily aid the cause of consumer spending. In addition to tax breaks for businesses that manage to increase employees’ wages, families with children are receiving ¥100,000 ($880) in cash distributions in this round.

We are bullish on the dollar relative to euro and the Japanese yen in 2022, owing to our contention that any surprise from the Fed will be on the hawkish side. In non-U.S. developed markets, we have strategies that hedge the forex and others that do not. We favor the former.

The place to bear foreign currency risk may instead be in emerging markets, where many currencies have already experienced heavy selling pressure in recent years.

Consider Brazil. The real2 was trading at BRL4.91 as recently as June, having sold off to BRL5.58 by late November. Brazil may be a ripe one for contrarians because good news is hard to find.

Its president, Jair Bolsonaro, suffers from a 24% approval rating owing to a tough slog with COVID-19. The “Operation Car Wash” corruption scandal, which broke several years ago, snagged so many government officials who were lining their pockets that it still looms large in the market’s psyche. On top of that, the 2019 collapse of a Vale-operated mine left scores dead, putting another reminder in investors’ heads of the types of surprises that often lurk in emerging markets.

Russia also has tough-to-digest headlines. The ruble has witnessed a sharp weakening as President Vladimir Putin threatens Ukraine with military engagement and the Kremlin orchestrates a migrant crisis at the Belarus-Poland border.

Though Europe’s energy crisis has subsided in recent weeks, 2022 may continue to witness Putin using “natural gas diplomacy” in a push to strong-arm the approval of the Nord Stream 2 pipeline. If the papers are signed, Moscow will be able to sell natural gas to Germany without it piping through Ukraine.

To add insult to injury, Putin’s natural gas theatrics and the green push on coal conspired to send Chinese manufacturers into an energy price-induced tailspin in H2 2021.

Maybe the biggest overhang for Chinese equities is the collapse of Evergrande, the bankrupt property developer that had to default on several notes this autumn. Peers such as Fantasia Holdings have already seen their debt obligations collapse to pennies on the dollar.

China also finds itself among the dwindling ranks of countries that are still trying to maintain a total COVID-19 containment policy. When Beijing will end “Covid Zero” is anyone’s guess. It hasn’t helped that the giant economy to its northeast, Japan, also took a tough COVID-19 hit in Q3. That country saw GDP contraction in Q3.

Investment Implications: After nearly two year spent surging, gains in global equity markets may be tougher to come by in 2022. Nevertheless, we think most central banks are behind the curve—and are starting from a very low interest rate base. Earnings forecasts are by no means ebullient, though we suspect vulnerability may confront companies with thin profit margins. With many stocks trading at dizzying valuations, we favor value biases with a profitability check to avoid being caught off guard in corrections.

REAL ASSETS AND ALTERNATIVES

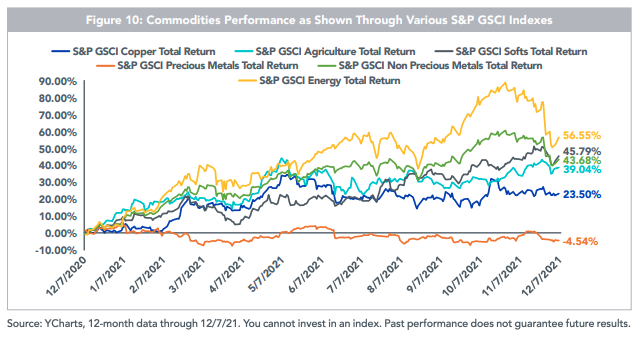

We expect commodities to continue to rally at least through the first half of 2022, as the global economy (eventually) moves past COVID-19 concerns and lockdowns. The evolution of and response to the Omicron variant of the virus may affect this outlook over time.

Furthermore, we expect investors to regain interest in real assets and nontraditional income sources, such as MLPs, REITs, infrastructure, covered calls and preferreds.

Finally, after years of relative dormancy due to low volatility and low interest rates, we expect renewed interest in alternatives and nontraditional investment strategies (e.g., global macro, arbitrage, long/short, managed futures, etc.) as investors seek to improve the diversification profile of their portfolios. Historically, these types of strategies have performed well in rising interest rate and volatility market environments, which we certainly believe we may experience as we move through 2022.

Investment Implications: One of our primary investment themes for 2022 is that, due to high equity valuations, rising rates and tight credit spreads, we believe there will be an increased interest in real assets, alternatives and portfolio diversifiers.

FIXED INCOME

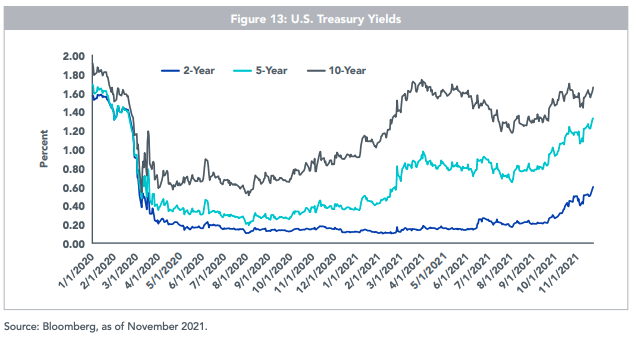

Recent trading activity in the U.S. Treasury (UST) market underscores the transformation taking place regarding the Fed policy setting for 2022. Typically, all eyes are on the UST 10-Year yield when discussing the rate outlook, but we advise also keeping an eye on the part of the curve that is more closely tied to potential Fed rate hikes, the 2- and 5-Year notes. In each case, the UST 2- and 5-Year yields have established new 2021 high watermarks and moved back to pre-pandemic readings. According to technical analysis, they have also potentially moved to “breakout” mode to the upside.

As far as the UST 10-Year is concerned, we expect the yield to trade “north” of 2% for most of 2022. Given the recent negative move in the TIPS market, we believe real yields are vulnerable to the upside too.

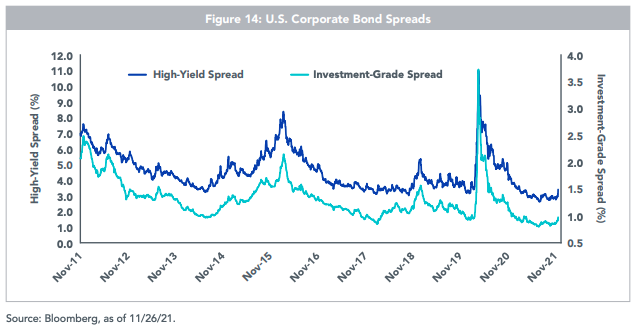

Solid corporate fundamentals and economic growth provide underlying support for U.S. corporate bond market valuations, despite historically tight levels. We continue to believe any potential spread widening would be viewed as a renewed buying opportunity. In terms of preference, we remain highly focused on credit selection in both investmentgrade and high-yield sectors and favor investing in higher-quality bonds lower down the credit spectrum over assuming additional rate risk in longer-duration bonds.

Emerging market (EM) central banks have aggressively raised short-term rates in 2021, improving carry at the short end and offering some protection against further rises in U.S. rates and dollar strength. However, near-term headwinds remain if U.S. rates continue to surge and the U.S. dollar presses on. But at some point next year, the combination of low valuations, higher carry in FX and higher income through EM debt could entice investors, potentially as the Fed’s path becomes clearer. EM corporates, given good fundamentals and more attractive yield opportunities than U.S. and developed market (DM) credits, should provide incremental value for credit investors and investors in general.

The dollar has been on a significant run lately, in concert with the rise in U.S. short-term Treasury rates. Despite positioning that is a little rich, dollar bulls should continue to be rewarded as investors price in a greater distinction among future central bank policies, particularly between the U.S., Europe and Japan. Right now, investors are intensely focused on the likely pace of the Fed reducing monetary accommodation to stem inflation pressures. Carry and momentum are providing support to the dollar.

Investment Implications: We maintain our positioning of being under-weight in duration and over-weight in credit, with a focus on quality security selection, especially in high-yield and securitized credit. We also believe investors will be increasingly interested in nontraditional or “alternative” yield solutions as they seek to generate risk-controlled income in today’s difficult market regime.

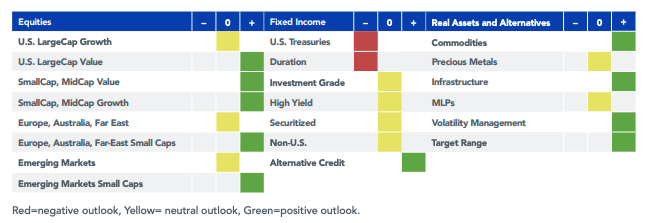

SUMMARY AND ASSET ALLOCATION IMPLICATIONS

WisdomTree has outlined three high conviction investment themes for 2022:

Rising Rates

Improving Core Allocations

The New Value Cycle

When focusing on what we believe are the primary market signals, we conclude that 2022 will enjoy cautiously optimistic economic and market environments, with the usual caveat of not knowing the outcome of the current “known unknowns.”

Our current asset class outlook is represented in the graphic below:

- Our asset allocation guidelines are as follows:

- We maintain a strong preference for stocks over bonds.

- In equities, we remain roughly in line with the MSCI ACWI Index in terms of our regional exposures to the U.S., EAFE and EM.

- Somewhat uniquely (we think), we have explicit over-weight allocations in small-cap stocks in the U.S., EAFE and EM.

- Given the evolution of COVID-19 and its variants and the increasing global rate of vaccinations, we think we may see a second “economic reopening” cycle, which will bode well for our allocations to value and small-cap stocks. Rising rates may provide a headwind to large cap/growthier sectors and stocks.

- The dollar rose toward the end of 2021, and that rally may continue in 2022, especially versus the euro and the yen. But we remain structurally bearish longer-term, and our non-U.S. positions remain unhedged.

- Within fixed income, we continue to favor shorter duration and an over-weight in quality credit (emphasis on quality security selection). We see pockets of opportunity in securitized and alternative credit.

- We are bullish on the broader commodity complex as the global economy recovers.

- We continue to see value in real asset and alternative investment allocations for investors seeking to increase overall portfolio diversification.

- Generating relative and absolute returns will be key in 2022—that is, we believe 2022 will be a year when investors focus on “alpha generation” and not simply “beta wave” performance. Expectations for returns from traditional assets remain muted, given current rates, spreads and valuations, and the ability of traditional diversified portfolios to achieve objectives in the manner they have in the past will be challenged. Capital efficiency, alternatives, alpha drivers and diversifiers will become increasingly important as we move through the year.

Glossary:

Basis Points (bps): 1/100th of 1 percent. Beta: A measure of the volatility of a security or a portfolio in comparison to a benchmark. In general, a beta less than 1 indicates that the investment is less volatile than the benchmark, while a beta more than 1 indicates that the investment is more volatile than the benchmark. Equity Risk Premium: An excess return that investing in the stock market provides over a risk-free rate. This excess return compensates investors for taking on the relatively higher risk of equity investing. Eurozone (EZ): Consists of the following 18 countries that have adopted the euro as their currency: Austria, Belgium, Cyprus, Estonia, Finland, France, Germany, Greece, Ireland, Italy, Latvia, Luxembourg, Malta, the Netherlands, Portugal, Slovakia, Slovenia and Spain (source: European Central Bank, 2014). Debt-to-GDP ratio: the ratio between a country’s government debt and its gross domestic product. Federal Reserve (Fed): The Federal Reserve System is the central banking system of the United States. Gross domestic product (GDP): the total monetary or market value of all the finished goods and services produced within a country’s borders in a specific time period. Growth stocks: Stocks whose share prices are higher relative to their earnings per share or dividends per share. Investors are willing to pay more because of their earnings or dividend growth expectations going forward. Price-to-earnings (P/E ratio): The ratio for valuing a company that measures its current share price relative to its per-share earnings (EPS). Quality: Characterized by higher efficiency and profitability. Typical measures include earnings, return on equity, return on assets, operating profitability as well as others. This term is also related to the Quality Factor, which associates these stock characteristics with excess returns vs the market over time. Return on Equity (ROE): Measures a corporation’s profitability by revealing how much profit a company generates with the money shareholders have invested. Return on Assets (ROA): Firm profits (after accounting for all expenses) divided by the firm’s total assets. Higher numbers indicate greater profits relative to the level of assets utilized to generate them. Treasury Inflation-Protected Securities (TIPS): a type of Treasury security issued by the U.S. government. TIPS are indexed to inflation in order to protect investors from a decline in the purchasing power of their money. Value: Characterized by lower price levels relative to fundamentals, such as earnings or dividends. Prices are lower because investors are less certain of the performance of these fundamentals in the future. This term is also related to the Value Factor, which associates these stock characteristics with excess returns vs the market over time.

Index Definitions:

Alerian MLP Index: the leading gauge of energy infrastructure Master Limited Partnerships (MLPs). The capped, float-adjusted, capitalizationweighted index, whose constituents earn the majority of their cash flow from midstream activities involving energy commodities, is disseminated real-time on a price-return basis (AMZ) and on a total-return basis (AMZX). Cboe S&P 500 Buy Write Index: tracks the performance of a hypothetical covered call strategy on the S&P 500 Index. The S&P 500 Buy-Write strategy involves buying the entire stock portfolio covered by the S&P 500 Index and selling equivalent number of near-term slightly out-of-the-money S&P 500 index call options on a monthly basis. Consumer Price Index (CPI): a measure that examines the weighted average of prices of a basket of consumer goods and services, such as transportation, food, and medical care. Dow Jones FXCM Dollar Index: The value of the United States dollar relative to a basket of four currencies: the Euro, the British Pound, the Japanese Yen, and the Australian Dollar. MSCI ACWI Index: A free-float adjusted market capitalization-weighted index that is designed to measure the equity market performance of developed and emerging markets. MSCI EAFE Index: Market cap-weighted index composed of companies representative of the developed market structure of developed countries in Europe, Australasia and Japan. MSCI Emerging Markets Index: a broad market cap-weighted Index showing performance of equities across 23 emerging market countries defined as “emerging markets” by MSCI. Purchasing Managers’ Index (PMI): An indicator of the economic health of the manufacturing sector. The PMI is based on five major indicators: new orders, inventory levels, production, supplier deliveries and the employment environment. A reading above 50 indicates an expansion of the manufacturing sector compared to the previous month; below 50 represents a contraction while 50 indicates no change. S&P 500 Index: Market capitalization-weighted benchmark of 500 stocks selected by the Standard and Poor’s Index Committee designed to represent the performance of the leading industries in the United States economy. S&P Global Infrastructure Index: designed to track 75 companies from around the world chosen to represent the listed infrastructure industry while maintaining liquidity and tradability. To create diversified exposure, the index includes three distinct infrastructure clusters: energy, transportation, and utilities. S&P Global REIT Index: Serves as a comprehensive benchmark of publicly traded equity REITs listed in both developed and emerging markets. S&P GSCI Softs: Sub-index of the S&P GSCI that measures the performance of only the soft commodities, weighted on a world production basis. In 2012, the S&P GSCI Softs index included the following commodities: coffee, sugar, cocoa and cotton. S&P GSCI Energy: Sub-index of the S&P GSCI, provides investors with a reliable and publicly available benchmark for investment performance in the energy commodity market. S&P GSCI Precious Metals: Sub-index of the S&P GSCI, provides investors with a reliable and publicly available benchmark for investment performance in the precious metals commodity market. S&P GSCI Agriculture: Sub-index of the S&P GSCI, provides investors with a reliable and publicly available benchmark for investment performance in the agriculture commodity market. S&P GSCI Copper: Sub-index of the S&P GSCI, provides investors with a reliable and publicly available benchmark for investment performance in the copper commodity market. S&P US Preferred Stock Index: Designed to serve the investment community’s need for an investable benchmark representing the U.S. preferred stock market. Preferred stocks are a class of capital stock that pays dividends at a specified rate and has a preference over common stock in the payment of dividends and the liquidation of assets.

IMPORTANT INFORMATION

Unless otherwise stated, all data as of November 23, 2021.

Investors should carefully consider the investment objectives, risks, charges and expenses of the Funds before investing. To obtain a prospectus containing this and other important information, please call 866.909.9473, or visit WisdomTree.com to view or download a prospectus. Investors should read the prospectus carefully before investing.

There are risks associated with investing, including the possible loss of principal. Foreign investing involves special risks, such as risk of loss from There are risks associated with investing, including the possible loss of principal. Foreign investing involves special risks, such as risk of loss from currency fluctuation or political or economic uncertainty. Investments in emerging or offshore markets are generally less liquid and less efficient than investments in developed markets and are subject to additional risks, such as risks of adverse governmental regulation and intervention or political developments. Funds focusing their investments on certain sectors and/or regions and/or smaller companies increase their vulnerability to any single economic or regulatory development. This may result in greater share price volatility.

Fixed income investments are subject to interest rate risk; their value will normally decline as interest rates rise. High-yield or “junk” bonds have lower credit ratings and involve a greater risk to principal. Fixed income investments are also subject to credit risk, the risk that the issuer of a bond will fail to pay interest and principal in a timely manner or that negative perceptions of the issuer’s ability to make such payments will cause the price of that bond to decline.

You cannot invest directly in an index. Index performance does not represent actual fund or portfolio performance. A fund or portfolio may differ significantly from the securities included in the index. Index performance assumes reinvestment of dividends but does not reflect any management fees, transaction costs or other expenses that would be incurred by a portfolio or fund, or brokerage commissions on transactions in fund shares. Such fees, expenses and commissions could reduce returns.

This material contains the opinions of the authors, which are subject to change, and should not be considered or interpreted as a recommendation to participate in any particular trading strategy, or deemed to be an offer or sale of any investment product, and it should not be relied on as such. There is no guarantee that any strategies discussed will work under all market conditions. This material represents an assessment of the market environment at a specific time and is not intended to be a forecast of future events or a guarantee of future results. This material should not be relied upon as research or investment advice regarding any security in particular. The user of this information assumes the entire risk of any use made of the information provided herein.

WisdomTree Funds are distributed by Foreside Fund Services, LLC, in the U.S. only.

Kevin Flanagan, Rick Harper, Jeremy Schwartz, Scott Welch and Jeff Weniger are registered representatives of Foreside Fund Services, LLC.

1 Source: Thomson Reuters Refinitiv, as of 12/1/21.

2 Referring to Brazilian currency.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All