The Fed is walking a tightrope between instability and inflation. Can it successfully tame inflation without causing severe market dislocations?

To reap the potential tax benefits of MLP investing and to make sure the allocation is meeting an investor’s needs, it’s important to understand the nuances of MLP investing.

A “boatload” of news this week suggests that the shipping industry continues to look very attractive from an investing point of view. Global cargo carriers are estimated to have recorded $150 billion in profits in 2021, the first time they’ve collectively reached that figure in a single year.

The municipal bond market has historically outperformed relative to Treasurys during periods of rising interest rates.

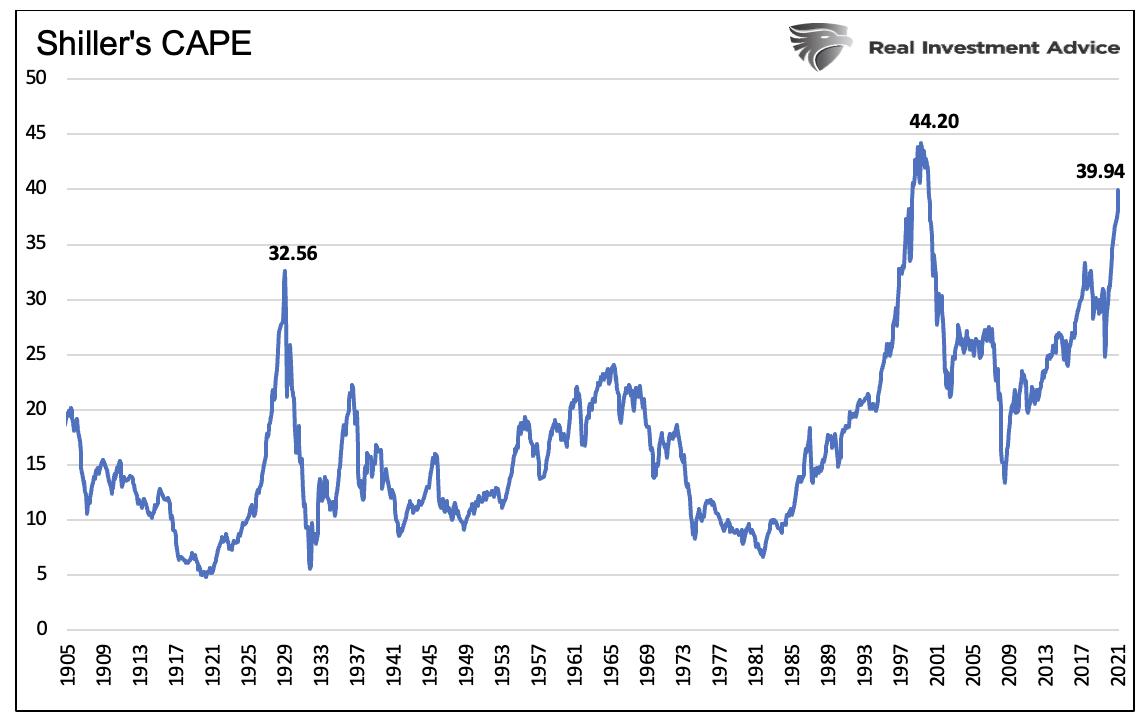

All 2-sigma equity bubbles in developed countries have broken back to trend.

A rapid one-two punch of interest-rate hikes and balance-sheet reduction from the Federal Reserve risks unsettling bond and stock markets that have already taken a beating.

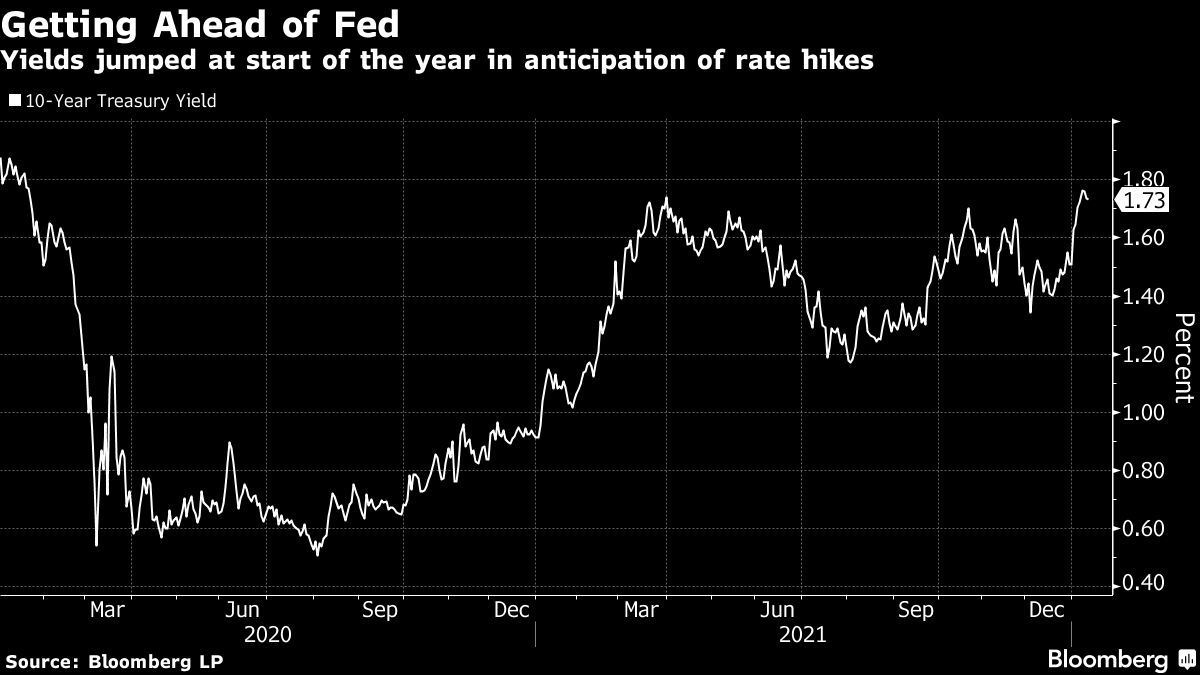

Last week, U.S. Treasury bond yields, climbed back to their pre-pandemic levels.

Now that the Fed has officially stopped referring to inflation as “transitory,” the question is whether they can bring it under control without slowing the economy. In our view, they have the right tools – reducing the balance sheet and raising the fed funds rate – they just need to trust their data and keep a steady hand on the wheel.

Treasuries slid and yield-curve premiums shrank to the lowest in almost two years amid increased speculation the Federal Reserve will deliver more than a quarter-percentage point rate hike in March.

Markets are weird right now. The value of risk-free assets has gone all out of whack, and if that doesn't seem scary, keep reading.

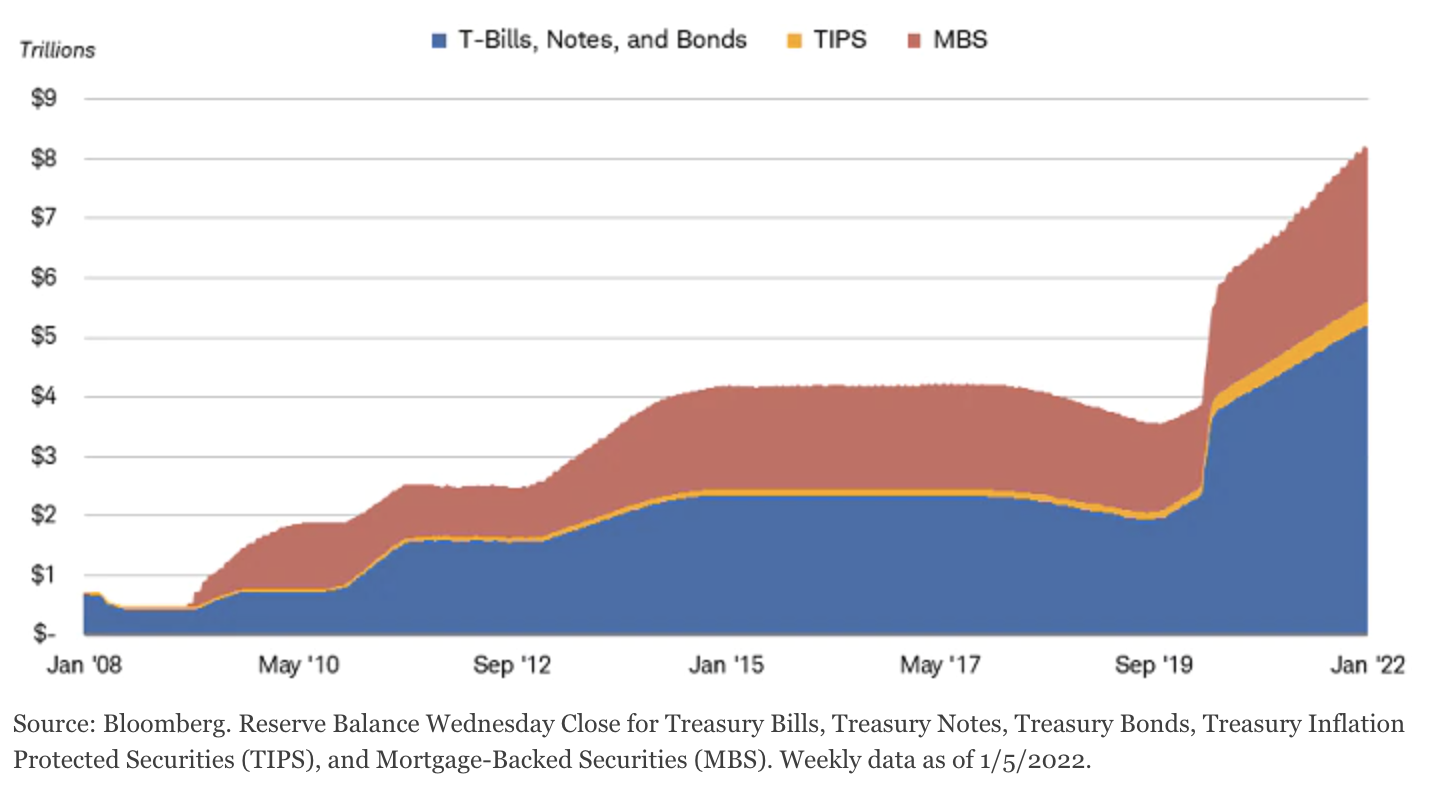

The flow of excess cash has returned to normal, but the stock is still quite elevated.

Stocks are priced for perfection. Bonds trade at historically low yields despite 7% inflation. What could go wrong?

If we will experience a lower equity risk premium, how much lower of a premium will make stock investing unattractive relative to bonds?

Few inventions have touched so many lives as the container.

In an economy where the Fed has lost every systematic tether to common sense, empirical evidence, and concern for financial stability, it’s worth beginning this first market comment of 2022 by recalling the ways we’ve adapted in order to navigate that environment.

As we reflect on 2021, we can’t help but feel it was quite a year. Looking ahead, we think many of the same headwinds and tailwinds are likely to persist in 2022, so we are trying to find the right balance between offense and defense.

The year ended on a highly upbeat tone for investors as equities rose to new heights against a backdrop of inflation and a prolonged pandemic

2021 is now in the rear-view mirror and I believe that future financial historians may regard it as the year of peak speculation.

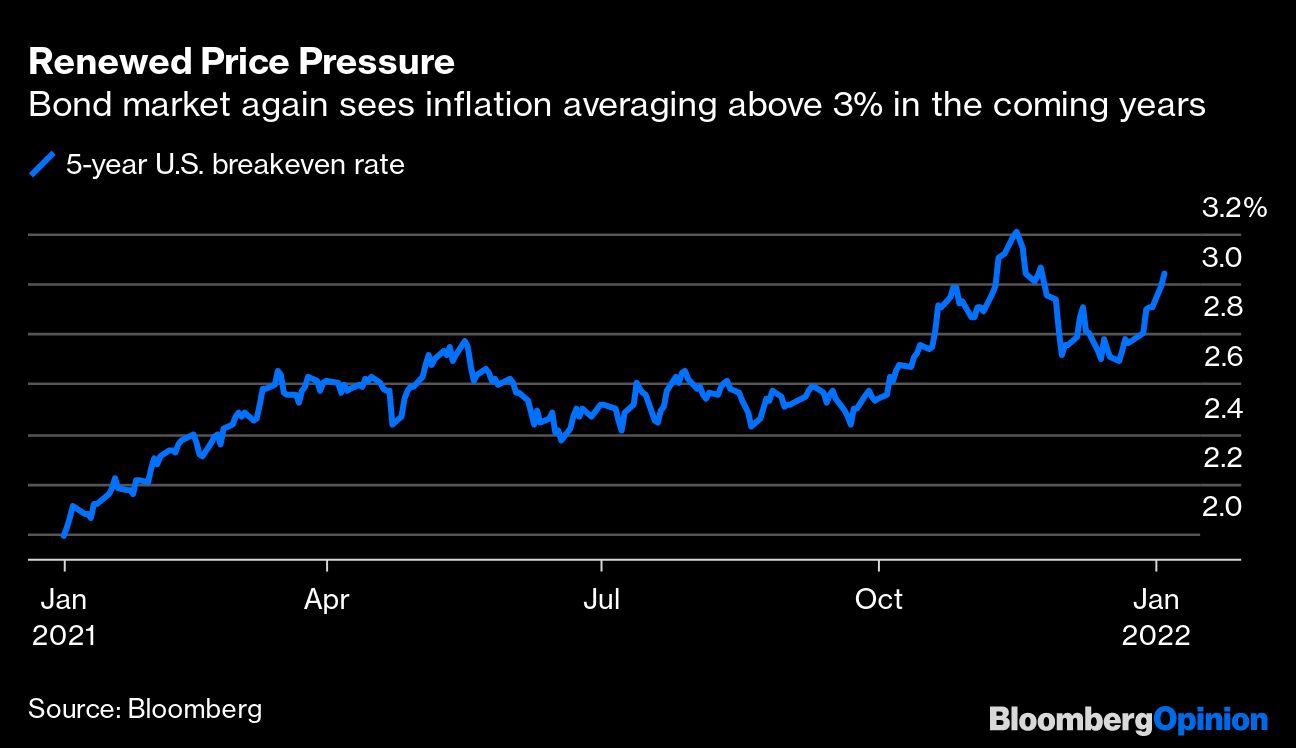

U.S. Treasuries shook off the steepest jump to consumer-price inflation in four decades and absorbed a 10-year note sale, with the figures reinforcing already widespread anticipation that the Federal Reserve will start raising interest rates in March.

The Federal Reserve dealt the bond market a sharp body blow on January 5th with the release of the minutes of its last Federal Open Market Committee (FOMC) policy meeting in December 2021.

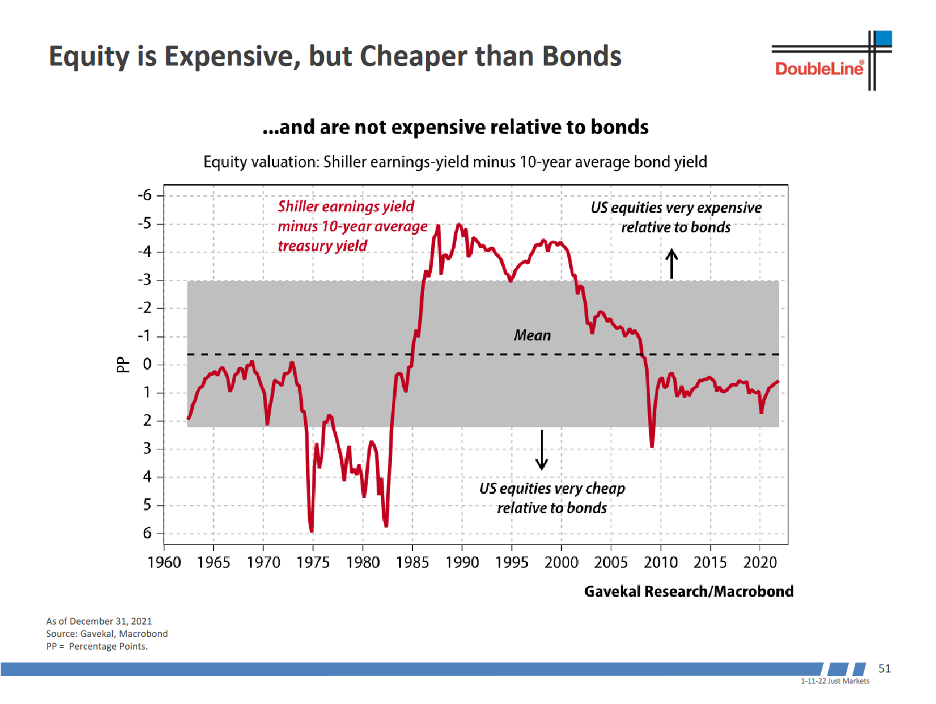

Monetary policy has driven U.S. stock prices to excessive valuations, according to Jeffrey Gundlach. But they remain cheap relative to bonds.

Uncertainty has become an ongoing theme in markets, economies, and communities everywhere, and in this environment, PIMCO investment professionals gathered – virtually, once again – for our recent Cyclical Forum.

Long before supply chain issues and soaring consumer prices made the headlines, I warned readers that massive monetary expansion made persistent inflation inevitable.

Some of the most exciting growth areas pertain to strong secular trends, many of which are agnostic to the growth potential of any geographic region.

Rates have seemed lower than they should be for a long time. With inflation surging higher now, it is critical investors solve this puzzle so they can construct portfolios accordingly

The Federal Reserve has managed to do something that’s rarely seen in the U.S. these days: Get members of the Democratic and Republican parties to agree.

One of WisdomTree’s flagship value Funds made some notable changes at the start of the new year.

Every year around this time, we update our always-popular Periodic Table of Commodities Returns.

Rising inflation is troubling bond investors worldwide, but European bond markets will likely experience comparatively weaker inflation pressures and stronger central bank support.

In this article, I examine the history of 13-year returns on stocks and bonds to put the most recent 13-year period into perspective. It has indeed been extraordinary.

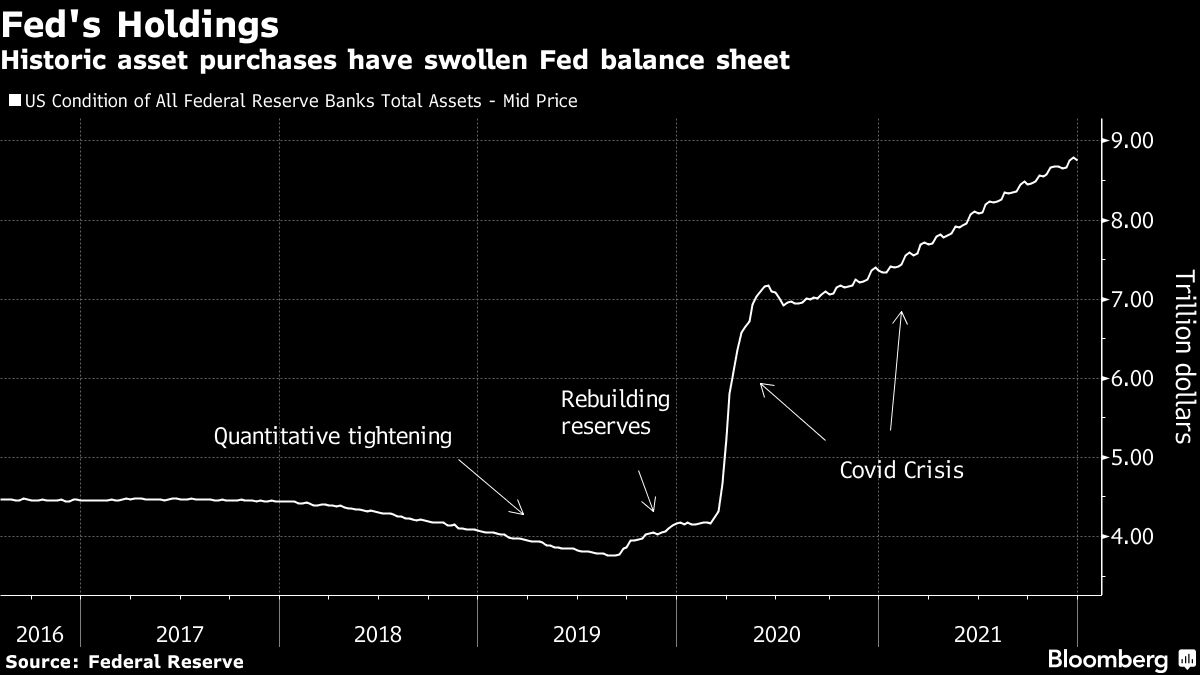

Federal Reserve officials have begun debating how to approach shrinking a stockpile of more than $8 trillion of bonds as a key element of a policy-normalization campaign in the wake of unprecedented moves to shore up the economy during the pandemic.

Not much has changed in regards to my economic growth outlook going forward since my most recent growth cycle update.

Cryptocurrencies had a breakout moment in 2021, and NFTs were some of the biggest stars. Now, as with any new and hot investing trend, financial pros are hoping to capitalize on the craze with products promising a way to piggyback on the market.

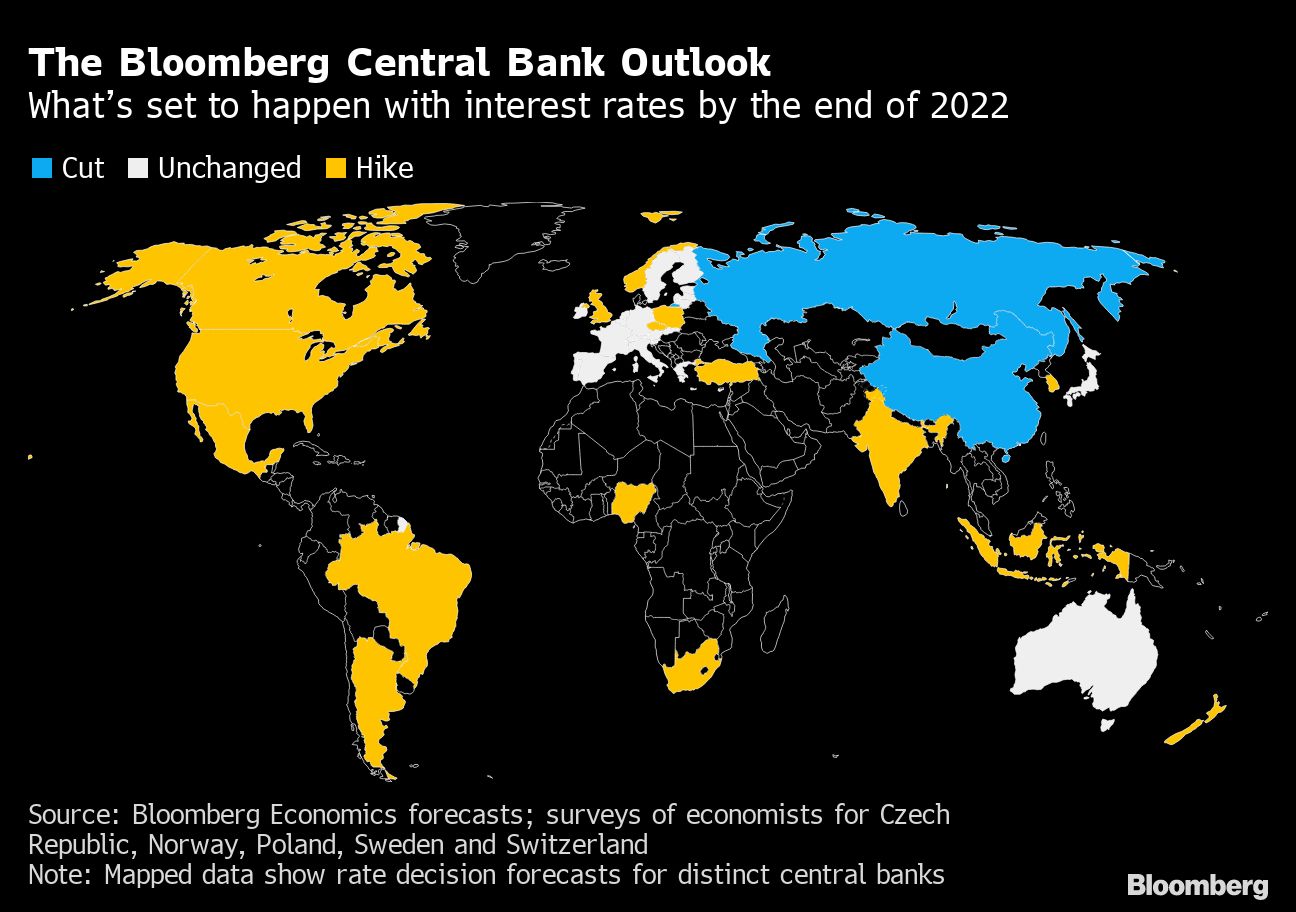

Global central banks are set to spend 2022 diverging, as some take on the menace of inflation and others stay focused on boosting economic growth.

Bond traders are turning into armchair virologists again.

Gold rebounded as the dollar pared gains and a U.S. manufacturing gauge fell short of economists’ expectations.

Small cap growth stocks lagged for most of 2021 as the market simultaneously dealt with the pandemic, inflation, and tightening Fed policy. Given these challenges, we have been focusing on high quality companies trading at attractive valuations, and we have also been looking at non-technology businesses that are embracing digitization.

Equities have enjoyed strong gains since the pandemic low of 2020, aided by massive monetary and fiscal stimulus, excess consumer savings, and incredibly negative real policy rates and bond yields.

What can investors expect this year? Above-trend economic growth, at least two interest rate hikes and continued earnings strength among technology stocks, says Raymond James CIO Larry Adam.

To all the record highs, the months without a correction and every other death-defying feat the stock market has pulled off, add another superlative. The S&P 500 Index has now doubled since New Year’s 2018, capping a stretch of sustained strength with few precedents.

A change in fundamentals could make international bonds more attractive.

In 2021, readers of the Investor Alert and Frank Talk were most interested in stories on gold mining, precious metals, natural resources and emerging markets (no surprise). But there was also interest in macroeconomic topics (inflation, mostly) as well as Bitcoin and cryptocurrencies.

Although major economies and markets fared well in 2021 despite all of the uncertainties surrounding new variants of the coronavirus, 2022 will bring new challenges. In addition to central banks shifting toward policy normalization, geopolitical and systemic risks are multiplying.

A Pittsburgh insurance broker and a Richmond, Virginia forensic accountant have developed an alternative rating system for measuring the ability of life/annuity companies to keep their promises even in market crises. They call it the transparency, surplus and riskier assets ratio, or “TSR” for short.

Anyone gearing up for bond yields to surge in 2022 should think again. A global glut of saved cash has the potential to restrain an increase in rates, even as central banks dial back their pandemic stimulus.

A legislative impasse raises bigger questions about public finances.

The S&P 500 will probably end next year with a gain, while yields on 10-year Treasuries and the price of oil will climb as well. That’s according to nearly 900 Bloomberg Terminal clients who responded to a survey conducted by our Markets Live blog in the first two weeks of December.

Rick Rieder and team identify 11 themes that could drive returns in 2022, as the greatest monetary experiment since the advent of flat currency enters its next phase.

As is our custom, we conclude the year by reflecting on the 10 most-read investment and planning articles over the past 12 months. Tomorrow, we will highlight the 10 most-read practice management articles.

CIO Robert Horrocks, PhD, sees fascinating and surprising investment opportunities arising in the emerging markets and China next year. Fed actions to manage inflation and the ongoing challenges of the pandemic will be important factors but the performance of markets may ultimately depend on the success of well-managed companies in key sectors.