As the weather forecast predicted deep cold to start the year, I remembered to move the stash of soda and beer from our unheated, detached garage into the house; bottles and cans may burst when the liquid inside freezes. As COVID-19 arrived on the scene, we developed a habit of staying stocked up to be ready for impromptu gatherings in our backyard and to hedge the risk of shortages at the store. Clearing the pile proved to be quite a chore, making me sweat despite freezing temperatures.

Our drink inventory wasn’t the only asset that surged last year. Savings throughout the economy were thrown out of normal patterns by pandemic-related stimulus programs. Depleting savings will be one component of a return to normal.

First, some definitions. Saving (singular) is the flow of money retained. In economic measures of consumption, saving is the remainder of personal income not spent after taxes and expenditures. Savings (plural) is the stock of accumulated money in financial assets, like bank accounts and investment funds.

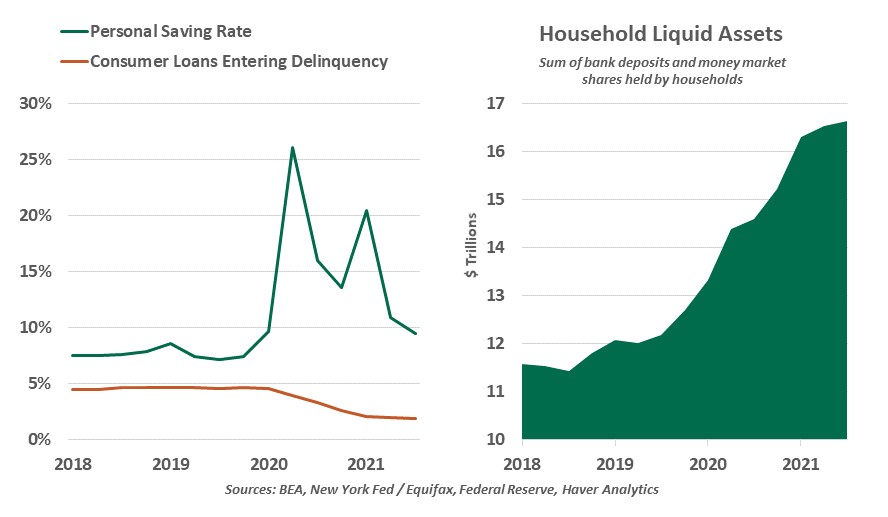

As the crisis took hold in 2020, the flow of saving reached new heights. Opportunities to spend money fell away as social gatherings were cancelled and travel was deferred. Terms for paying essential bills like rent and mortgage payments became lenient. Meanwhile, stimulus payments provided an extra cushion. Most workers maintained their incomes or experienced only a short disruption, while those who lost their jobs benefitted from enhanced unemployment payments. Steady incomes and lower expenses allowed saving to take off: the saving rate has hit exceptional peaks, as high as 34% in April 2020.

Through the interval of stringent lockdowns, some saved money was repurposed into durable goods purchases like home improvement and major purchases like new homes. Then, a reopened economy in 2021 allowed a return to spending on services. An additional COVID relief bill passed last March disbursed more cash, and child tax credit advance payments gave many parents monthly stimulus through the second half of the year. A comfortable savings buffer and a year of disruptions equipped consumers to get out and spend, and we did: as of November, personal consumption expenditures stand 13.5% higher than a year before.

The U.S. saving rate has started to normalize. In November, the share of income not spent was 6.9%, in line with its pre-crisis level. Government support programs have concluded, while venues for spending are continually reopening. But while elevated flows may be in the past, a substantial stock of savings remains. Liquid assets (bank accounts and money market funds held by households) are $3.3 trillion higher than their pre-pandemic level as of the third quarter of 2021, according to Fed aggregates.

|

Consumers' savings grew faster than most were able to spend.

|

Consumer credit also reflects the positive state of household finances. Credit card balances fell in the course of the pandemic, and to this day, roughly half as many accounts are reported with a past-due status. While debt repayment does not appear as saving in the personal consumption data, reducing liabilities improves households’ balance sheets. Credit issuers must now compete against consumers’ savings in order to grow their loans. In the second and third quarters of 2021, credit card balances returned to moderate growth (2.2% each quarter), another sign of a return to normal spending behavior.

These elevated savings have set the stage for growth to come. Some major purchases, notably automobiles, have been deferred; inventories are low, limiting options and inflating prices. As supply chains recover, purchase activity will carry on. Meanwhile, many of us who took opportunities to travel and socialize were reminded last year how important it is to get out of the house, and spending on services is likely to rebound when the current pandemic wave recedes. Savings can fuel higher spending, and compensate for tapering levels of government support.

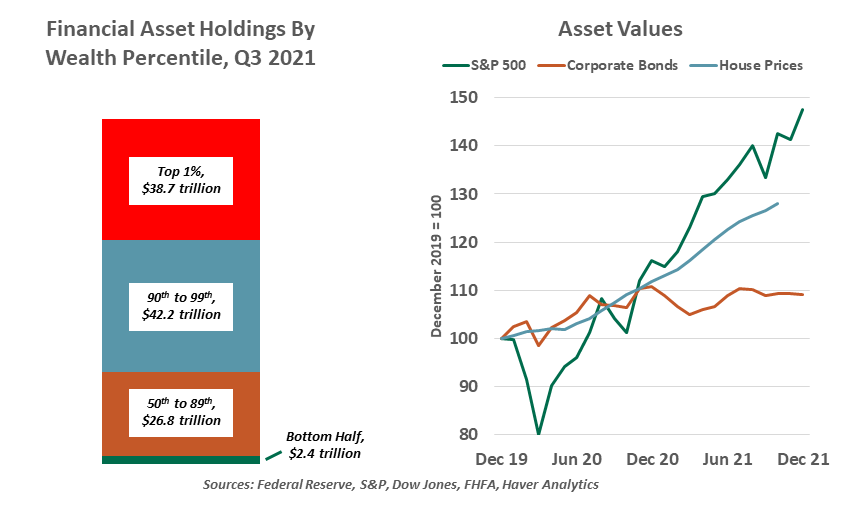

Cash savings alone are not the only reason for optimism about consumer spending. Nearly every asset class has appreciated since the COVID crash. Stocks broke new ground, with the S&P 500 closing at all-time highs on 70 trading days in 2021. Homeowners enjoyed a surge of home equity as house prices rose. Persistently low yields reduced total returns in bonds, but they have performed well and served their role as a risk hedge, with minimal defaults. The wealth effects generated by strong markets bolster confidence and keep consumers active. And as long as demand stays robust, the risk of a correction will stay low.

|

A rising tide lifts all boats, but some are closer to the sea floor than others.

|

The news is not uniformly good. Approximately half of households do not have retirement accounts that would have gained value, and even fewer invest in stocks directly. A third of households do not own their homes; they not only missed the upside of the housing market, but now must contend with rising rents. While all income earners enjoyed a gain in savings, lower earners started from a substantially lower base. Their cushion will be the first to run out, and their spending will be the first to lose momentum. For all that changed in the pandemic, the wealth picture has stayed fixed. The bottom half of households by wealth currently own 3.5% of all liquid assets, little changed from their pre-crisis share.

A consideration of both stocks and flows made me feel less guilty about our “savings” of beverages. Perhaps we over-bought, but we did not over-consume; too much consumption would have made for a less healthy year. And when the weather warms and neighbors come calling, I will be glad to have liquidity on hand.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2022 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.

© Northern Trust

Read more commentaries by Northern Trust