Does a risk-free bond with 7% yield interest you? If so, read about the red-headed stepchild of the bond world that is finally attracting investors.

On May 29, Colombia could elect its very first leftist president should Gustavo Petro receive a majority of the vote. The former congressman and mayor of the capital city of Bogotá, Petro is an unabashed admirer of and Hugo Chávez.

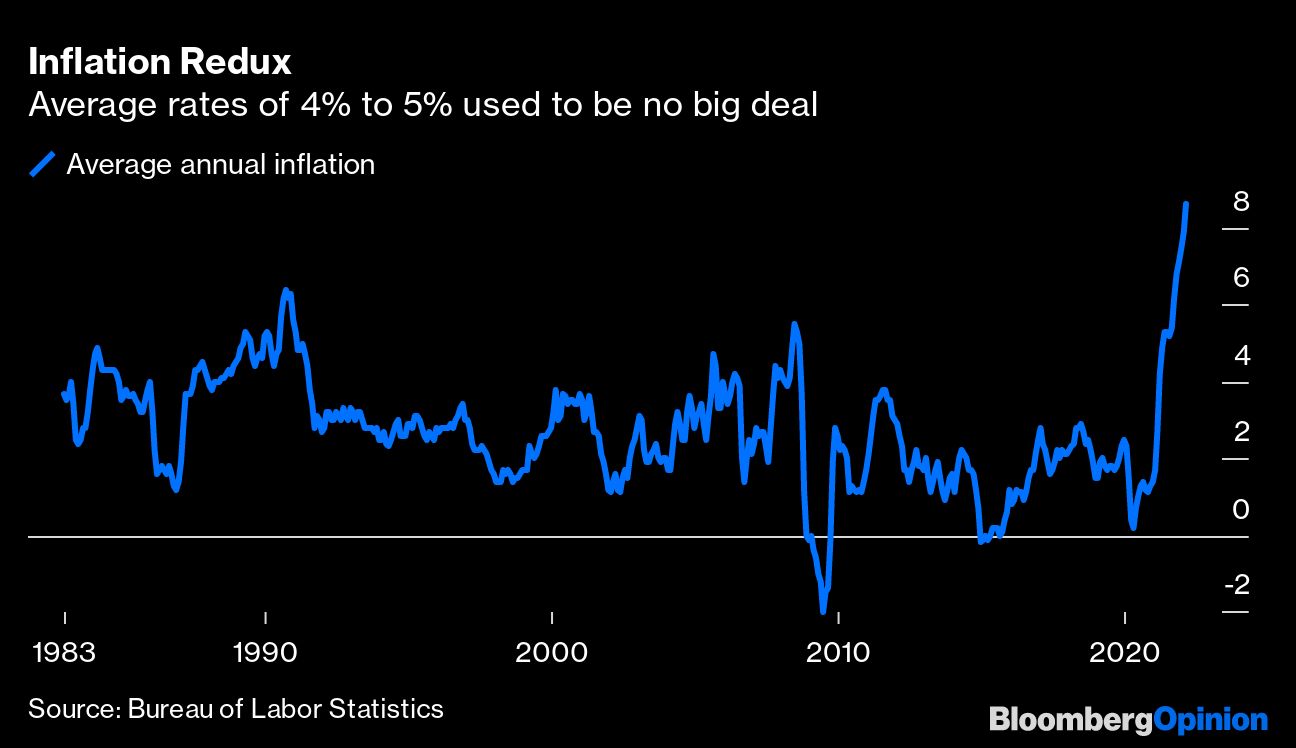

If you haven’t noticed—perhaps because you live on Mars—inflation is here. Not just in the US but almost everywhere. Prices for everyday goods and services, including necessities like food, are climbing rapidly. The US Consumer Price Index rose 8.5% in the 12 months through March… and we know it understates categories like housing.

It might seem at first that everything is against emerging markets.

Concerns about the Ukraine war, inflation, and the Fed were top of mind last quarter, but a lesser appreciated long-tern headwind is the de-globalization of the labor force, which could have profound effects on the economy.

Our last edition of Volume Analysis stated, “The federal reserve’s rocket has since overshot its orbit, causing massive inflation while providing a speculative paradise for risk assets.

Mortgage-backed securities (MBS) have taken a hit over the last several weeks with the news of the Fed’s plans to shrink its balance sheet. Today's guest, Dean Smith of FolioBeyond, will discuss why the combination of the rise in Treasury yields and the widening of MBS spreads is continuing to increase the valuations of certain types of mortgage-backed securities. With the expectation that the pace of rate hikes will soon be more aggressive, Dean will explain how the actively managed rising rates ETF, RISR, will benefit and generate alpha. The FolioBeyond Rising Rates ETF (RISR) is up 26.55% YTD (as of 4/13/2022) and is ranked #1 by Morningstar among non-traditional bond strategies.

I didn’t start the fire.

How bullish are we feeling? If the American Association of Individual Investors’ weekly survey is anything to go by, not very. It has been carried out for decades and is much followed as a measure of sentiment. Retail investors are simply asked if they’re feeling bullish, bearish, or neither.

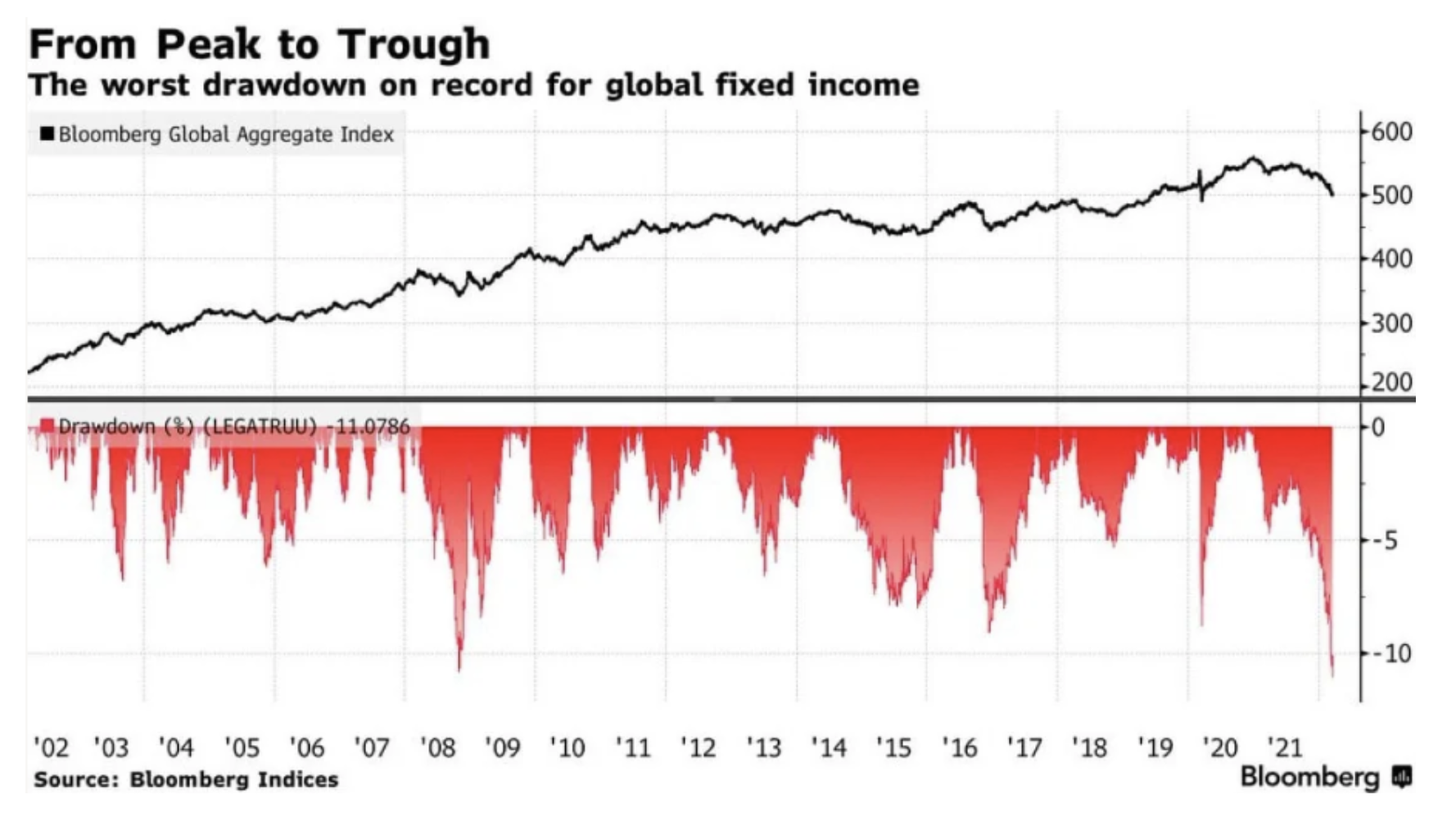

Traditional long-only fixed income managers had one of the worst quarters on record in Q1 2022 as higher interest rates left “bottom up” portfolios overweight duration.

Real Treasury bond yields fell into deeply negative territory in 2021.

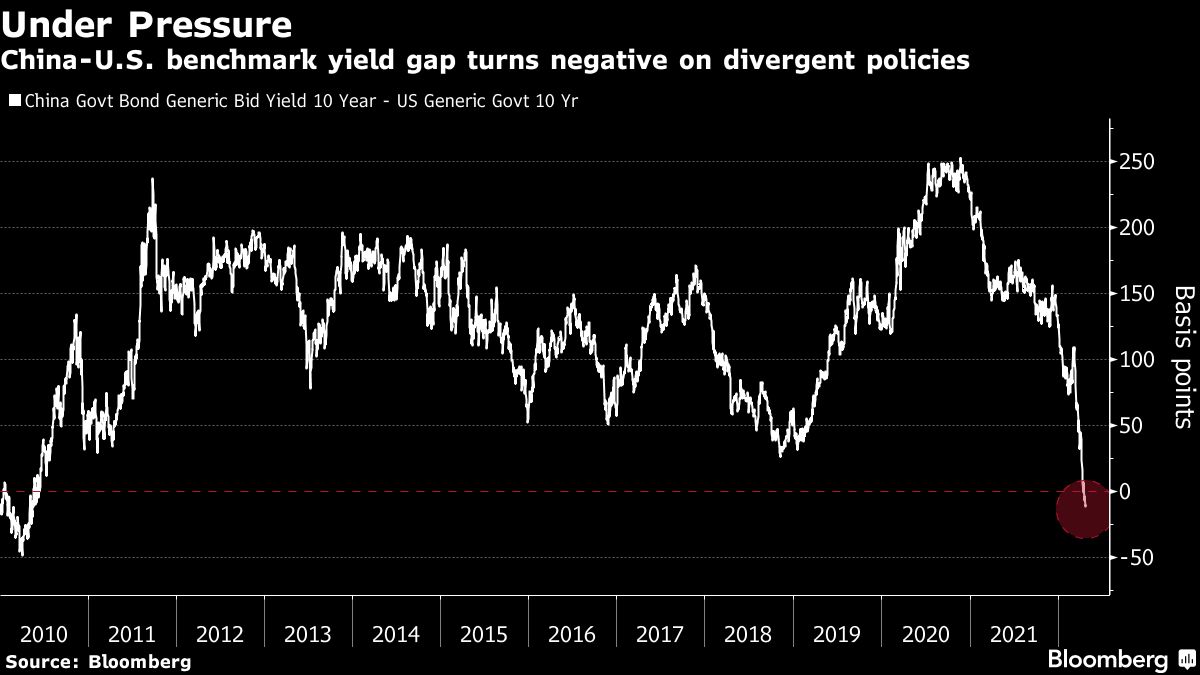

Asia’s two biggest central banks are having to grapple with the fallout from the Federal Reserve’s hawkish pivot.

An often overlooked and underutilized fixed-income alternative, preferred securities offer investors compelling diversification and income opportunities in today's volatile, rising interest rate environment. With yields and returns comparable to high-yield fixed income, today's preferred securities have evolved into a distinct and attractive income-generating asset class.

As we have noted in this space in the past, there is a lot of the world that cannot be captured by the most elegant and detailed of spreadsheets.

Russia’s invasion of Ukraine has exacerbated inflation, which was already rising. The big questions now are how far will the Fed be willing to go to slow inflation, and how will the market react as rates increase?

Something in the market changed about a half-year ago. A dandy old “truism” that had made the rounds for ages got scrapped.

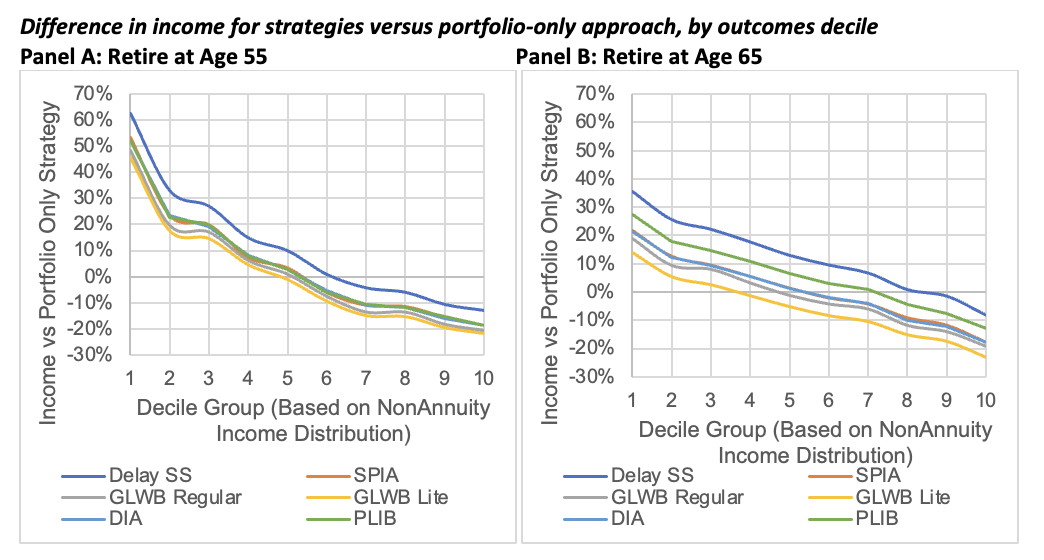

While the lower fees associated with GLWB Lite products make them seem more attractive, the expected income is significantly lower than other annuities.

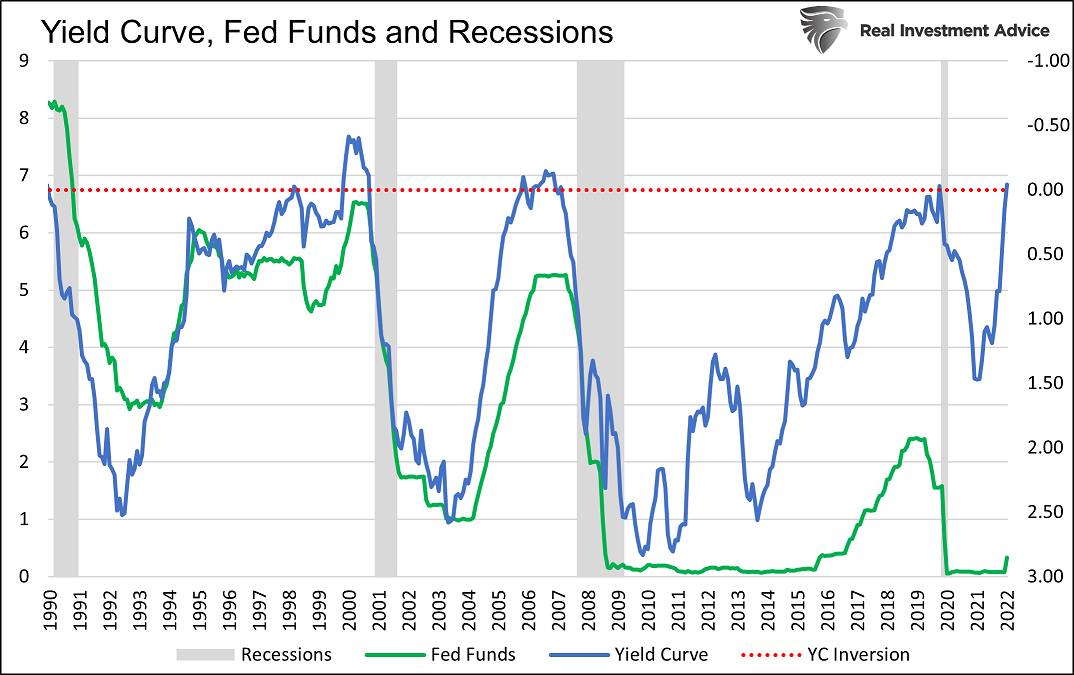

The war in Ukraine has further complicated the investment backdrop, and fears of a recession are rising now that the U.S. yield curve has inverted. Given so much uncertainty, we are focusing on what we can control and maintaining a defensive posture

The last decade and a half rewarded investors with healthy stock and bond returns. But high valuations, low interest rates and high inflation are signals to reassess risk tolerance and asset allocations.

U.S. government bonds dropped across the curve, with the two-year yield up two basis points to 2.47% as of 11:28 a.m. in New York. The 10-year yield rose two basis points to 2.85%, while a long-maturity Treasury ETF suffered a nearly 30% decline from a peak in August 2020 -- a record drawdown.

It’s Easter weekend, so we are going to revisit a 2018 letter about the yield curve. The yield curve is much misunderstood and misused by many analysts. This letter will give you the tools to understand the correct importance and relevance of the yield curve. And then, a few comments about Ukraine.

An unusually strong tug of war between economic forces is playing out in global markets, with a booming economy and low unemployment offset by the effects of the Russian invasion of Ukraine and expanded inflation. Expectations over the timing and magnitude of Fed interest rate increases rapidly evolved as clarity began to emerge around central bank responses to inflation.

Value has trounced growth this year, and high dividend companies have outperformed. Matt Wagner discusses the global dividend investment opportunity: emerging markets.

On Tuesday, the day that government-reported inflation hit 8.5%, Jeffrey Gundlach said it may reach 10% this year.

The more the Fed decides to dance with inflation and ignore the bond market and economy, the more we should expect stock prices to fall.

To start, let’s discuss what diversification is and what it is not.

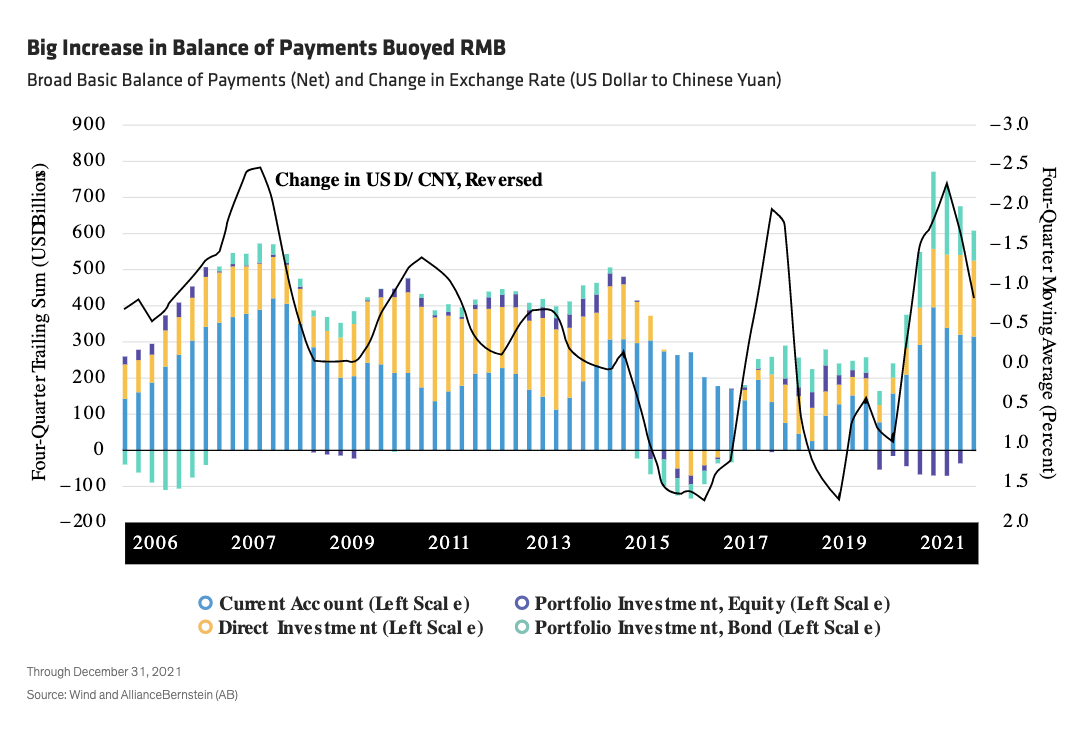

China’s currency, the renminbi (RMB), remains strong even though many of the factors that have driven its performance over the last two years have weakened.

The market was tough in the first quarter. Find out what it means for long-term investors.

Central to my market and macro outlook at present is the likelihood we are amid a growth cycle downturn that is looking to decelerate meaningfully in the coming months.

Now that inflation is back, it's not going away anytime soon. The Federal Reserve expects it to fall below 3% next year and eventually go back to 2%. But there are reasons to think that’s far too optimistic. We are living in a new world. Even after things get back to normal that could mean inflation averages 4% or even 5% for the foreseeable future.

It’s the next big market call that could enrich traders across Wall Street: The raging global energy crisis and ever-more hawkish central banks knock key economies into 1970s-style stagflation. It’s a long shot for now, but anxiety is building among money managers that this market scenario -- out-of-control inflation just as growth slumps -- will eventually come to pass, especially in Europe.

It’s not just interest rate changes that affect the markets, changes in the Fed balance sheet can also be a source of negative returns to equity and bond markets.

Covid-19, global supply-chain disruptions, frictions in reopening economies worldwide and now Russia’s invasion of Ukraine are spawning many winners and losers in economies, financial markets and political structures. Six of them are driven by transfers of incomes and assets. Five more are fundamentally the result of repricing goods and assets that I’ll cover in a separate column.

Easter 2022 arrives this week with its usual egg-hunting and chocolate-bunny traditions, but also with some bitter new realities. Major candy makers such as Hershey Co., Mars Inc. and Nestlé SA need to overhaul their production practices if they want to continue feeding the world’s chocolate habit.

There is a genre of investment research that continuously predicts economic disaster that I call “macro doom.” It has become very popular. It seems that everyone is an expert in macroeconomics today, and they’re all predicting a bust of some kind.

There was a little March Madness on Wall Street.

When interest rates go up, many analysts start to worry about recessions.

The Russian invasion of Ukraine has added pressure to the inflationary cycle that began in late 2020.

Markets rebounded in March, but it was not enough to offset earlier losses in January and February.

Antti Ilmanen’s Investing Amid Low Expected Returns updates his 2011 Expected Returns, a volume considered by many the definitive work on the subject.

Rising rates are a direct shot at your bond portfolio. But there's a real opportunity to address your equities and position them optimally for a rising rate environment.

While all Treasury yields have climbed this year as the Fed began what’s expected to be an aggressive series of rate increases aimed throttling high inflation, in the past two weeks the baton has been passed to inflation-protected notes and bonds. Their yields are termed “real” because they represent the rates investors will accept as long as they are paired with extra payments to offset inflation.

An estimated 30,000 people attended this week’s Bitcoin 2022 conference in Miami, which is rapidly becoming a major global crypto-finance hub.

“Anatomy of a Bear Market” by Russell Napier is a “must-read” manuscript. Given current market dynamics, a review seems timely.

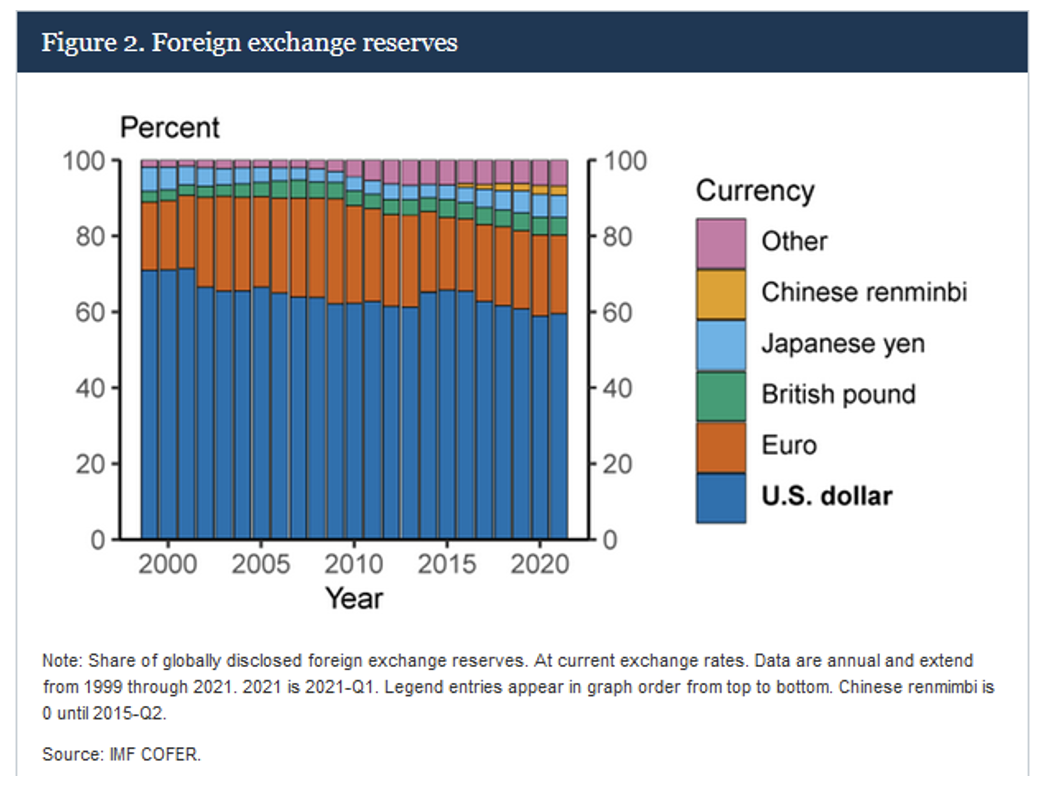

This article explores the problem vexing Russia and its trade partners. I explore how the threat and use of sanctions may force some countries to contemplate weaning off the world's reserve currency.

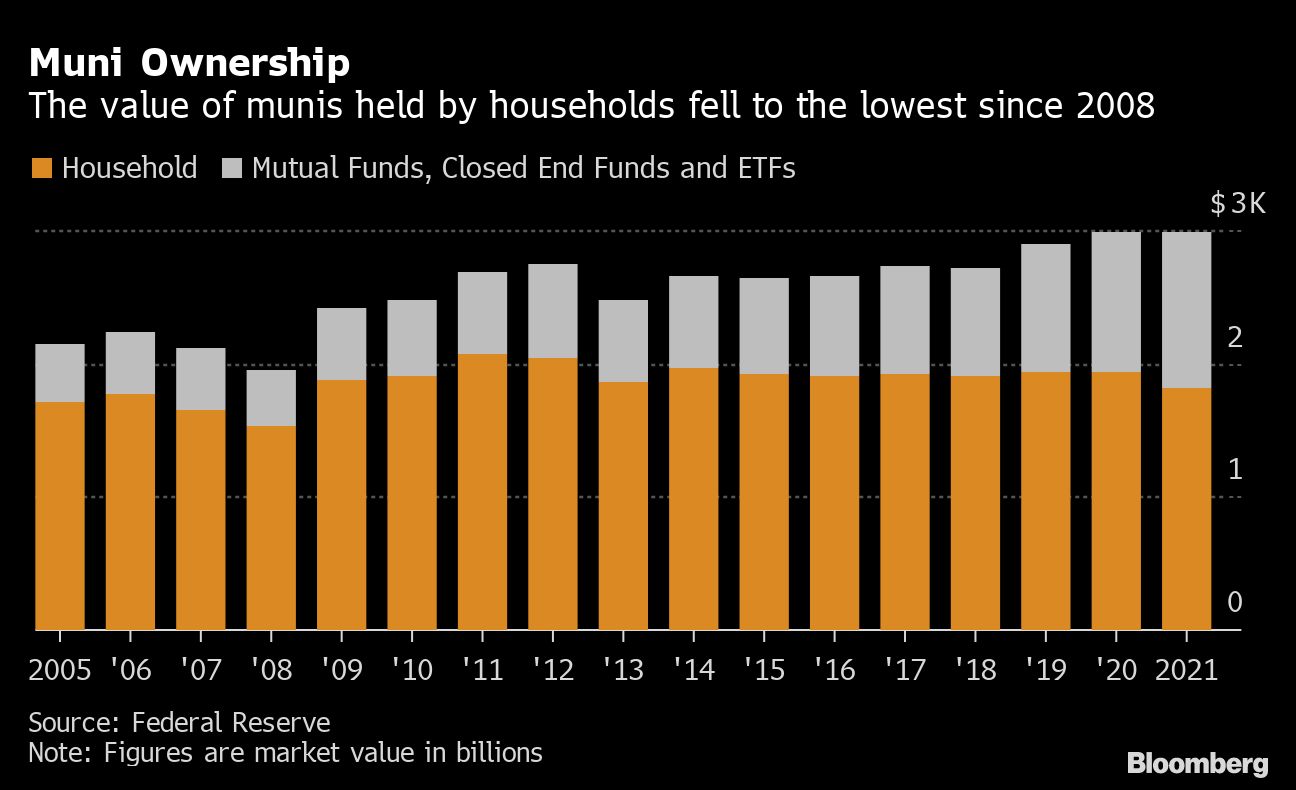

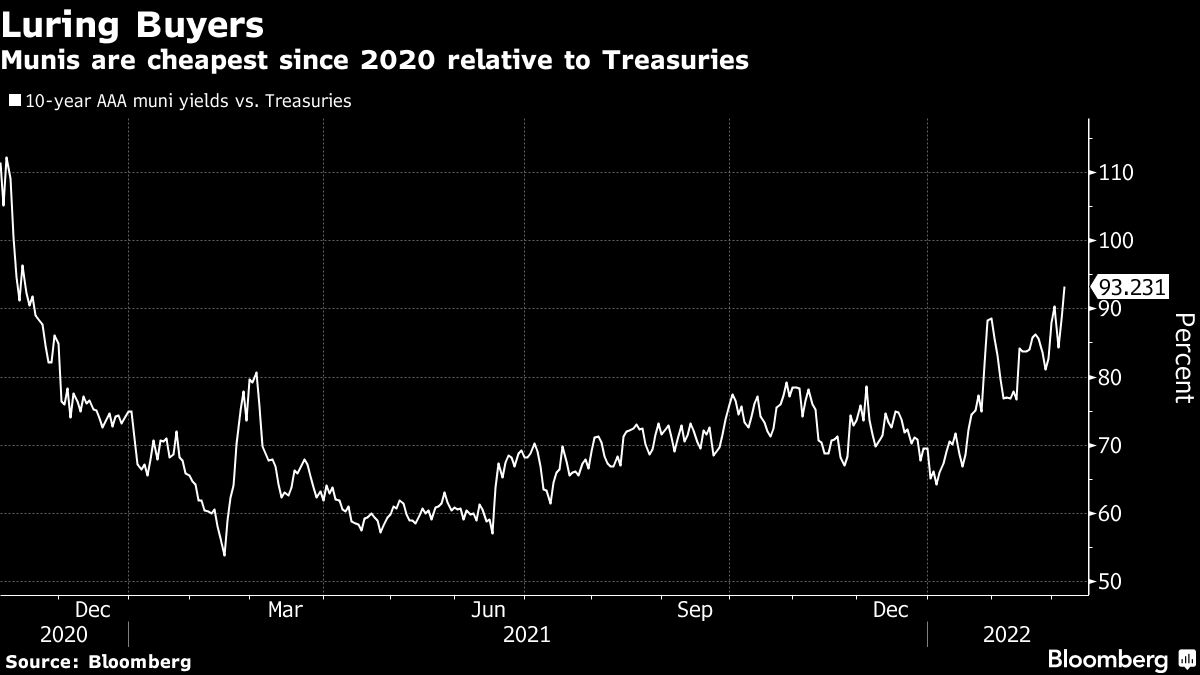

The value of bonds directly owned by households fell by $18 billion in the fourth quarter of 2021, dropping to the lowest level since 2008, according to Federal Reserve data. Instead, those buyers are moving toward mutual funds and exchange traded funds, which have roughly doubled their muni holdings over the last decade.

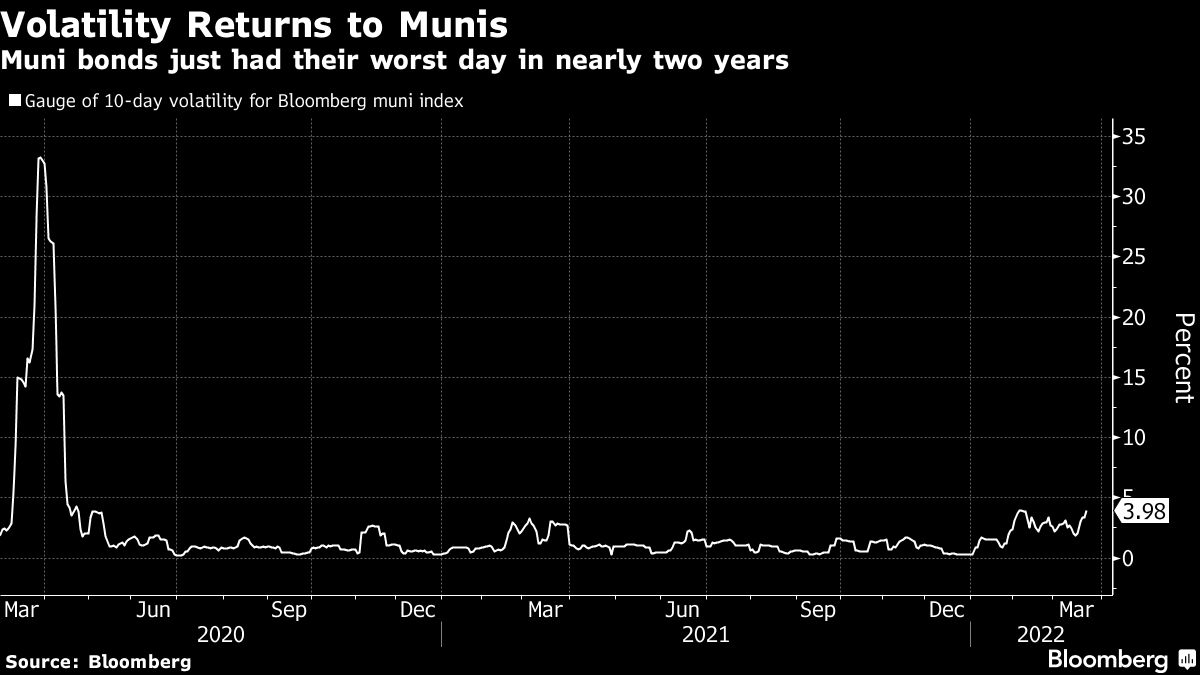

The $4 trillion state and local-debt market just logged its most volatile 10-day period since the early 2020 selloff, according to data compiled by Bloomberg. Benchmark yields rose as much as 11 basis points on Tuesday, driving the market to its worst day of performance since April 2020. AAA yields rose as much as 2 basis points as of 4 p.m. on Wednesday.

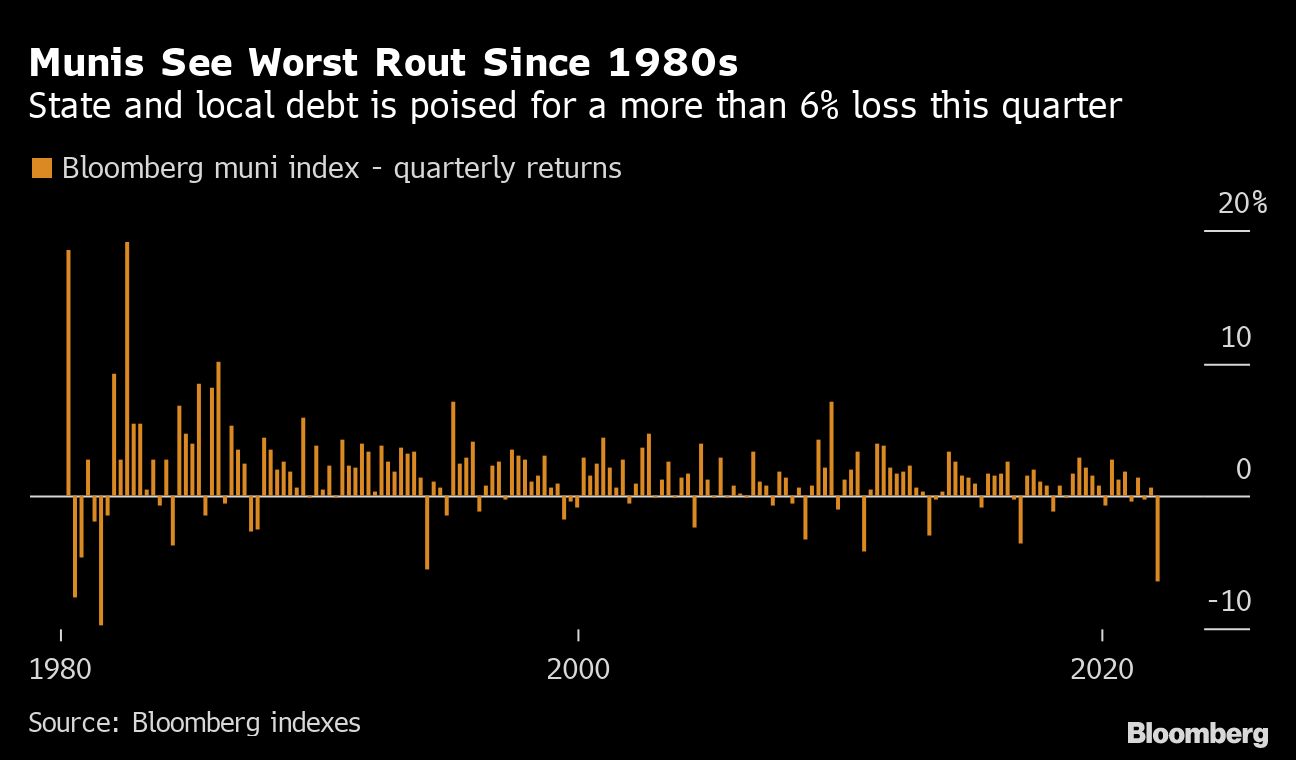

The municipal-bond market is ending its worst quarter in about 40 years with a 6.4% loss, a dramatic pullback for an asset class that investors favor for its stability. The loss so far this year is in line with bonds globally as central banks increase interest rates to combat the fastest inflation in decades. The municipal market is still underperforming U.S. Treasuries, heightening investor concern.

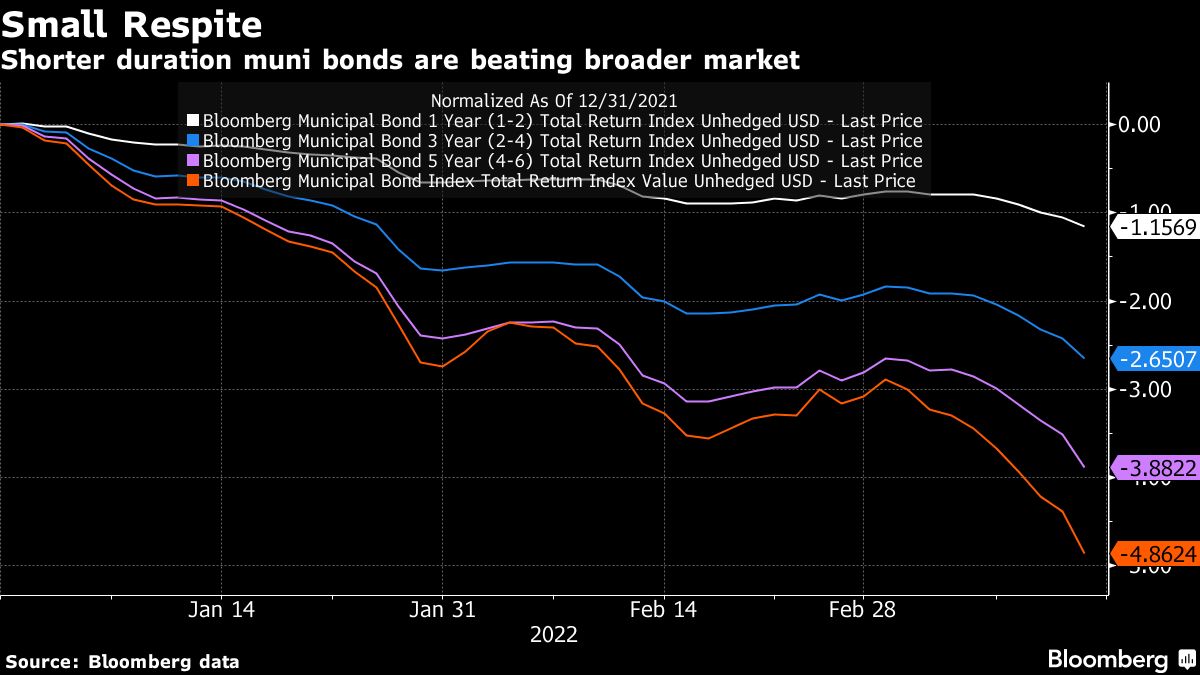

It’s been a bleak stretch in the $4 trillion municipal-bond market, with returns slumping, retail investors dumping bonds and volatility giving issuers pause. But some portfolio managers are jumping into the fray.

The muni market has posted a loss of 4.9% this year, with the 10-year benchmark yield hitting the highest mark since the pandemic-induced tumult of March 2020. But some market participants are seeking relief at the shorter end of the curve.