The Case For Preferred Securities in a Rising Rate Environment

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsExecutive Summary

An often overlooked and underutilized fixed-income alternative, preferred securities offer investors compelling diversification and income opportunities in today's volatile, rising interest rate environment.

With yields and returns comparable to high-yield fixed income, quality nearing that of investment-grade credits, and low correlation with the fixed income and equity markets, today's preferred securities have evolved into a distinct and attractive income-generating asset class—boasting a variety of structures and serving as a meaningful component of an investment portfolio.

Preferred securities are a specialty of Bramshill Investments, differentiating our firm from others in the fixed income investment management arena.

An Underutilized Asset Class

Currently valued at $750 billion, the universe of US preferred securities is modest in size relative to the $4.7 trillion US investment-grade corporate bond market and the $52 trillion

US equity market. Due to their perceived complexity in structure, preferred securities are often overlooked by income-seeking investors without access to the expertise needed to capitalize on the return and yield opportunities preferred securities offer.

From a capital structure standpoint, most preferred securities are senior to equities but subordinate to senior corporate debt. However, certain hybrid securities can be issued along the capital structure spectrum.

Originally conceived as an intermediate form of capital issuance and primarily used to finance growth in utilities, preferred securities offer fixed payments or dividends from after-tax profits. These preferred share dividends are interrupted only if dividends to common shares are discontinued and do not trigger a default as would occur for an interruption in debt service. Not only may preferred securities serve as a high-quality source of consistent income for investors, but they may also offer favorable tax treatment advantages:

- Because dividends on preferred securities are paid from after-tax profits, investors may also enjoy the tax benefit of Qualified Dividends (or “QDI”), which are taxed at favorable capital gains rates.

- Certain corporate investors may be able to deduct up to 70% of the income from their income tax, the “Dividend Received Deduction” or DRD for preferred securities.

The Evolution Of Preferreds

Preferred securities have evolved over the years beyond their original use to fund utilities' capital needs. They were also used later in the 1980s by financial firms to build capital structures that met everchanging regulatory requirements.

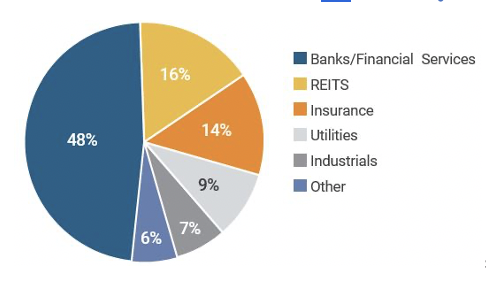

As the following chart shows, they are now widely issued by banks, REITs, insurance companies, utilities, industrials, and other sectors of the economy to raise capital.

Preferred Securities Issuers By Industry

Source: BofA Global Research as of 4/13/21.

A Variety Of Structures

As a hybrid security with both equity and fixed income characteristics, preferred securities appear more appropriately placed in an investor’s fixed income allocation.

The evolution of preferred securities has resulted in a variety of newer structures. Some are exchange-listed and traded like traditional preferred securities, while others tend to be structured more like debt offerings. These various structures provide investors with many investment options, but confusion often arises on how these financial instruments can play a part in an overall portfolio allocation.

The range of preferred securities structures available includes:

- Perpetual Fixed Rate Preferreds: Long duration instruments with typically fixed coupons for life. Most are non-call 5-year or non-call 10-year securities.

- Perpetual Fixed-To-Floating Rate Preferreds: Instruments that carry fixed coupons for a short period, and then a floating rate coupon spread over a benchmark such as LIBOR or SOFR.

- Fixed-To-Reset Preferreds: Instruments with a fixed coupon for 5 or 10 years, at which time they are either called or the coupon "resets" to a spread over matched duration Treasuries.

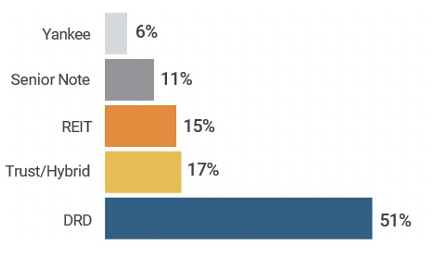

These preferred securities structures can be issued by a variety of entities and with differing characteristics. For example:

- DRD Preferreds

- Preferred Securities Characterized as Senior Notes: which are effectively bonds.

- Trust and Hybrid Preferred Securities: which combine debt and equity.

- REIT Preferred Securities: interest payments are paid from after-tax profits but do not receive the DRD privilege due to other tax benefits available to REITs.

- Non-US Firms Preferred Securities: denominated in dollars, referred to as Yankee preferreds.

A Range Of U.S. Preferred Securities Structures Chart Here

Source: BofA Global Research as of 4/13/21.

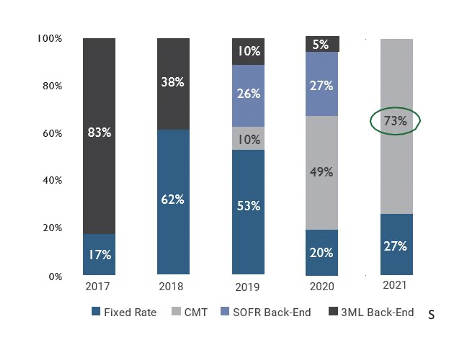

Fixed-To-Reset Preferreds - CMT Structure

Another important new preferred structure that, as the chart below shows, has significantly dominated issuance recently, is the Fixed-To-Reset Preferreds CMT (Constant Maturity Treasury) structure that offers reset rates linked to Treasuries. The importance of this new structure in a rising rate environment will be examined in more detail on page 4 of this white paper.

US Bank Preferred Issuance By Structure

Source: Bloomberg Finance L.P., J.P. Morgan as of 1/31/22

Performance, Volatility, & Correlation

The diversification benefits of preferred securities when compared to high-yield bonds within a fixed income allocation appear much greater with comparable returns and less volatility.

- From a return perspective, for the past 10 years ended 12/31/21, the annualized total return for the preferred securities asset class, as measured by the Bank of America Perpetual Preferred Index, was 7.10%, and was comparable to the 6.72% annualized total return for the US high-yield bond sector, as measured by the Bank of America US High-Yield Index.

- In terms of volatility, preferred securities have shown significantly less volatility than the equity and high-yield bond markets. For example, the Bank of America Perpetual Preferred Index has exhibited volatility of 5.63% compared with 13.10% for the S&P 500 Index for the 10-year period as of 12/31/21 date.

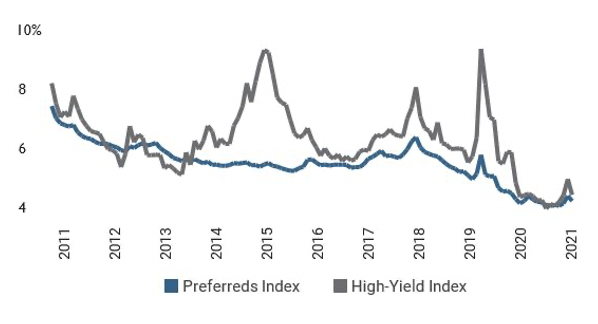

YTM of Preferreds Index Versus YTW High-Yield Index

Source: Bloomberg as of 12/31/21

- From a yield perspective, as the chart below shows, preferred securities provide competitive yields comparable with high-yield fixed income.

A Competitive Fixed Income Alternative

Source: Morningstar as of 3/28/22.

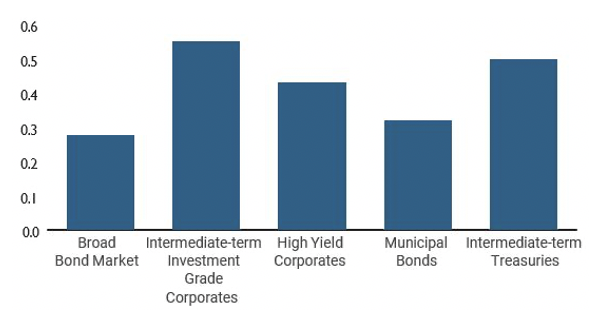

- From a correlation perspective, as the following chart illustrates, preferreds act more like investment-grade corporates than either government bonds or high-yield.

Correlation Of Preferreds To Other Fixed Income Assets

Source: Stifel

High-Quality, Risk Mitigation

Rating agencies typically treat preferred securities as a form of debt in their ratings and usually rate preferreds two or three levels below senior debt securities. However, because most issuers of preferred securities are themselves investment-grade, many preferred securities carry investment-grade agency ratings. This fact, along with the fact that default rates are lower than high-yield debt, confirms that preferreds are usually of higher credit quality than high-yield debt.

In addition, the overall improved financial quality of preferred securities issuers (regulated financial institutions are the largest single issuer of preferreds) and lower default risk since the financial crisis is notable. For example, since the financial crisis of 2007-2008, banks have increased their capital position through issuing preferred securities, retaining earnings, and limiting leverage, with the objective of achieving a much more stable financial structure that annual stress tests by the Federal Reserve have periodically confirmed.

Various Transaction Avenues

At Bramshill, we view the US preferred securities market to be an asset class that is highly differentiated from other fixed income areas in that it offers a variety of structures, uncorrelated returns, and, in addition, numerous liquidity outlets to transact.

There are two par amount price structures with which preferred securities are typically issued.

- Ø Preferreds of $25 par structures, are typically considered for retail investors and trade on the New York Stock Exchange. To transact, an investor can use a broker, a market maker, an OTC block desk, or an algorithm. Due to continued retail investment and seasonality effects, many opportunities will present themselves during periods of volatility.

- Ø $1000 par structures, are typically placed with institutional investors and are traded over the counter by institutional market makers and investment banks from their investment-grade trading desks, crossover desks, or electronic bond trading platforms such as MarketAxess, where both “buy-side” and “sell-side” investors directly participate.

Due to varying preferred securities investor fund flows, different avenues to transact, and differentiated investor bases, there are often relative value mispricings within the same corporate capital structure or specific preferred securities sector, providing compelling investment opportunities. Bramshill constantly assesses relative value between the $25 par and $1000 par markets and often exploits opportunities which become more apparent during volatile market periods. For example, Fixed-to-reset preferred securities have been predominantly issued in the $1000 par market. Because of Bramshill’s consistent investment process and concern over the past year with rising interest rates, its investment team has been able to direct the vast majority of its preferred exposure within this limited duration structure.

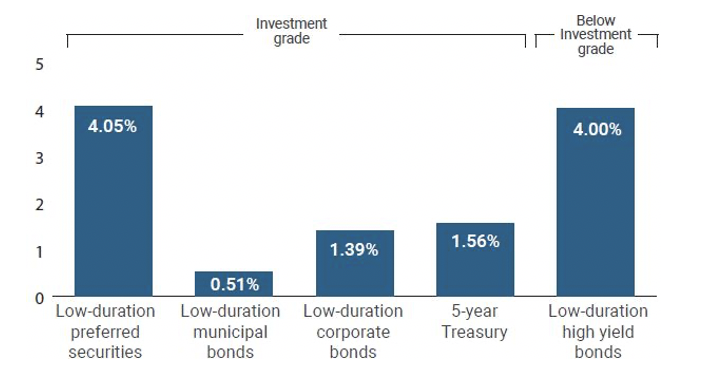

Preferred Securities In A Rising Rate Environment

Similar to bonds, yields of preferred securities and interest rates are highly correlated. A rising rate environment brings increased interest rate risk for investors in long duration, perpetual fixed rate preferreds, as well as increased price volatility. In the following grid, which details the year-to-date performance of five perpetual fixed rate preferred securities, the dramatic impact of rising rates and duration extension on such securities is apparent.

The Impact Of Rising Rates And Duration

Source: Bramshill Investments Research as of 3/29/22

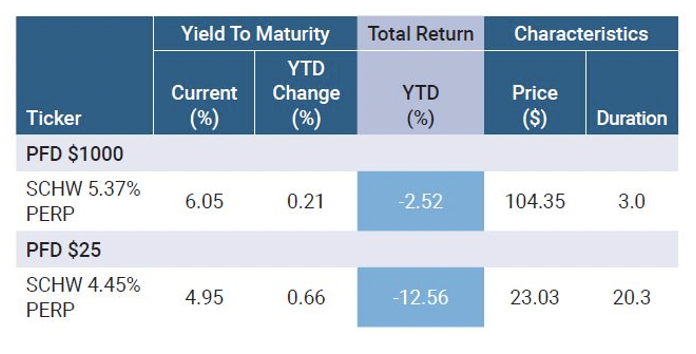

However, it is important to note that this is not the case for fixed-to-reset or CMT-structured preferreds. Following is an example of preferreds with distinct structures that have acted very differently this year. While the perpetual fixed rate preferred shown is down -12.56%, the fixed-to-reset structure is down only -2.52% as of 3/7/22.

Preferred Structure Matters

Source: Bramshill Investments Research as of 3/7/22

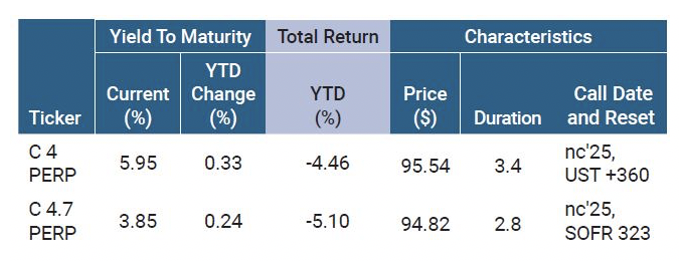

We currently see a relative value opportunity in fixed to reset CMT structures over fixed to float LIBOR/SOFR structures. The market is putting little differentiation between a CMT structure and a SOFR floating rate structure as can be seen in the table below. These two securities are from the same issuer thereby having the same credit risk, with similar call dates. The main difference is the first security resets after the call date at a spread off 5-year US Treasury, while the second security floats after the call date at a spread off SOFR. Currently there is a 220bp difference between the 5-year US Treasury and SOFR.

Additionally, the reset spread is higher in the CMT structure. At this time the CMT structure is more likely to get called at the call date and if not called, the “step-up” coupon is substantially higher in the CMT structure. However, due to forward curves and Fed expectations, the market is ignoring this differential and assuming that SOFR will be comparable to the 5-year US Treasury in the near future. While possible, we think this is too aggressive of an assumption, and thus feel these structures should not trade so close in price.

The CMT Structure's Relative Value Opportunity

Source: Bramshill Investments Research as of 3/29/22

A Compelling Opportunity With CMTs

We believe CMT-structured and low duration preferred securities represent an underappreciated opportunity for income-oriented investors in a rising rate environment.

- CMT structured preferred securities offering resets rates at specific basis points above Treasuries are one of the most compelling fixed income alternatives available today.

- Low duration floating rate preferreds at discount prices, can also provide attractive opportunities for income-seeking, rate-sensitive investors.

- High coupon short call preferreds also provide compelling opportunities in a rising rate environment.

With impending Federal Reserve rate hikes in 2022, we expect each of these preferred securities structures to outperform from a yield, return, and volatility perspective—potentially mitigating interest rate risk, providing relatively attractive yields, and effectively positioning an investment portfolio for future income opportunities.

Conclusion

Due to a variety of structures and an eclectic investor base, the preferred asset class can provide a great deal of investment opportunities in different market environments and volatile regimes. Due to our multi-decade relationships, execution capabilities, quantitative modeling, and research analysis teams, we believe Bramshill maintains a competitive advantage in this asset class which will continue to serve our clients well over many different market cycles.

About The Contributors

Art DeGaetano | Chief Investment Officer & Founder

Mr. DeGaetano is the Chief Investment Officer and Founder of Bramshill Investments. He has over 30 years of investment experience with a focus on fixed income and preferred securities.

Derek Pines | Portfolio Manager & Analyst

Mr. Pines is a Portfolio Manager & Analyst at Bramshill Investments where he co-manages their flagship Income Performance Strategy. He has over 20 years of investment experience, including a focus on fixed income and preferred securities.

About Bramshill Investments

Bramshill Investments is an alternative fixed income asset manager with over $4.8 billion in assets under management as of February 28, 2022.

Founded in 2012 and headquartered in Florida, with offices in California and New York, the firm offers an alternative to traditional fixed income investment management featuring a variety of strategies across various debt and fixed income markets and specializing in preferred securities.

Disclosure

Bramshill Investments, LLC (“Bramshill”) is an asset management firm and investment adviser registered with the U.S. Securities and Exchange Commission (“SEC”). Registration with the SEC does not imply any skillset of Bramshill or its employees . All statements and opinions are subject to change as economic and market conditions dictate. Investing involves risk, including the potential loss of principal, and the profitability of any particular investment strategy or product cannot be guaranteed. Our view and opinions are accurate as of the date of this letter and are provided for informational purposes only and are for the sole use of the intended audience/recipients, all of which are or represent current or potential investors in one or more investment vehicles or mutual fund (each a “fund” and collectively the “funds”) managed by Bramshill. The data and information presented herein has not been audited (except as otherwise expressly indicated) and is subject to subsequent adjustment. Bramshill has no obligation, express or implied, to update any of the information or to advise you of any changes. Similarly, Bramshill does not make any express or implied warranties or representations as to the completeness or accuracy, or accept responsibility for inaccuracies, errors or omissions. Past performance is not necessarily indicative of future results. No representation is being made that any fund or portfolio managed by Bramshill will or is likely to achieve profits or losses similar to those shown. Further information regarding the funds and investment strategies are available upon request. For more information, please refer to www.bramshillinvestments

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All