GLWB Lite: Lower Costs but Much Worse Benefits

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits There is an emerging interest in guaranteed income solutions (annuities) for retirees among financial advisors and defined-contribution (DC) plan sponsors. At the same time, though, market dynamics have created challenges with offering certain products that provide lifetime income, in particular products with a guaranteed lifetime withdrawal benefit (GLWB). In response, some of the newer GLWBs have been introduced with lower fees and notably weaker benefits, which I refer to as “GLWB lite” in this article.

There is an emerging interest in guaranteed income solutions (annuities) for retirees among financial advisors and defined-contribution (DC) plan sponsors. At the same time, though, market dynamics have created challenges with offering certain products that provide lifetime income, in particular products with a guaranteed lifetime withdrawal benefit (GLWB). In response, some of the newer GLWBs have been introduced with lower fees and notably weaker benefits, which I refer to as “GLWB lite” in this article.

I’ll provide an overview of GLWBs, some context around the changes in the GLWB space, and analyze the expected economic benefits of these annuities versus other common approaches to generating guaranteed income.

While the lower fees associated with GLWB Lite products make them seem more attractive, the expected income is significantly lower than other annuities available today (and the alternative approaches considered in this analysis). Financial advisors and plan sponsors should take pause before selecting these products for clients. Additionally, given the current low bond yield environment, delaying claiming Social Security is likely to provide the most income for retirees and should likely be considered and optimized before using a private annuity.

GLWBs: A brief introduction

Early research on the potential benefits of annuitization primarily focused on more traditional, relatively simple guaranteed income products such as single-premium immediate annuities (SPIAs), also referred to as immediate-fixed annuities, and deferred-income annuities (DIAs). Despite the noted benefits of SPIAs and DIAs and annuities in general, they remain relatively unpopular among retirees, an effect commonly dubbed the “annuity puzzle.”

While there are a variety of potential explanations for the annuity puzzle, one notable barrier to usage is the irrevocable design of many annuities (e.g., SPIAs), which require the annuitant to permanently cede the premium to receive the lifetime income. The irrevocable aspect of SPIAs and DIAs is likely a key reason that sales of the products have been relatively low.

One product that provides lifetime income and on-going access to the premium is the GLWB feature, also referred to as a guaranteed minimum withdrawal benefit (GMWB). This is common in variable annuities (VAs) and fixed-indexed annuities (FIAs) and could be offered with more traditional portfolios as part of a contingent-deferred annuity (CDA).

Introduced in the 1990s, GLWBs allow access to the contract value (i.e., they are revocable) and guarantee a minimum level of lifetime income (which could increase) even if (or when) the underlying account value goes to zero.

The income level for a GLWB is determined based on the payout rate, also known as the guaranteed percentage or lifetime distribution factor, to the “benefit base” (also called the income base). The payout rate is based on the age of the annuitant at the time of the first withdrawal, or the younger of the two annuitants if it’s a joint couple. GLWB payout rates typically increase at older ages at varying increments (e.g., some companies have five-year bands, other more granular levels) and are typically higher for single versus joint annuitants.

The benefit base is a “tracking account” (i.e., it is not accessible) to determine the income level. GLWBs have traditionally offered a “step-up” provision, where the income/benefit base is increased to equal the greater of the existing income/benefit base or the contract value, typically at least once per year. Some products have provided a minimum guaranteed annual increase in the income/benefit base (called a “roll up”).

Introducing the GLWB lite

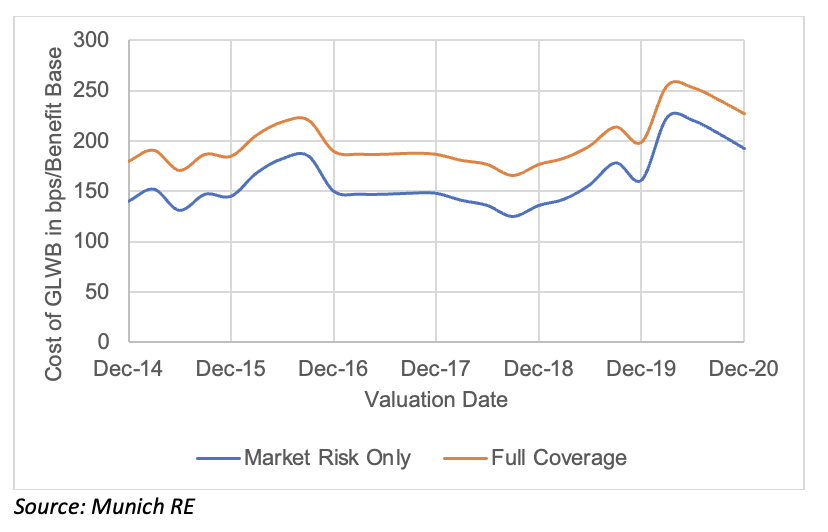

GLWBs have been out of favor, with a number of providers exiting the business, given the low bond yield environment and the rising costs associated with issuing and maintaining them. For example, Munich RE released research estimating how the reinsurance cost of GLWBs changed from January 2000 to December 2020, as shown below. The estimated cost of the product likely exceeds 200 basis points (bps) today, which is well above the rider costs common in the industry (closer to 100 bps).

In response to the challenging economics associated with issuing more traditional GLWBs, newer products are being introduced to maintain some of the more widely known attributes of GLWBs, such as a 5% payout of the income/benefit base for a single annuitant at age 65, but change other features that have been common.

For example, while GLWBs have traditionally offered an annual “step-up” provision (again, where the income/benefit base is increased to equal the greater of the existing income/benefit base and the contract value, typically at least once per year), more recent products only offer a step-up only once, at retirement. Under this arrangement, the income/benefit base value is compared to the contract value only at retirement, and that is the value used to determine the lifetime income amount. While these GLWB lite products typically have lower fees (i.e., can be less than 100 bps all-in, including the rider fees) the reduced payout approach significantly waters down the income benefit.

Other common changes include additional investment restrictions, in particular requiring the investor to use an investment that incorporates a managed-volatility strategy, which lowers the effective risk of the product and will negatively impact contract value growth.

A relatively newer product structure that I will also review is an approach I refer to as a protected income lifetime benefit (PLIB). PLIBs are similar to GLWBs, where the annuitant has access to the contract throughout retirement (i.e., the decision is revocable); however, the income benefit differs in that the income level varies each year based entirely on the credited performance of the account for the previous year (net of fees). For example, if the PLIB income was $5,000 and the net return of the account (including fees) for the prior period was +20%, the income level would increase by 20% to $6,000. The income changes annually based on performance. The payout structure is effectively similar to a liquid immediate variable annuity, with an assumed interest rate (AIR) of 0%. Once the contract has been depleted the income level from a PLIB is generally assumed to be constant and based on the income level the year before the contract is depleted.

Analysis

This analysis considers two cases, with a single individual who retires at age 65, but is either currently 55 or 65 (i.e., retiring immediately or in 10 years).

For both cases the portfolio balance is assumed to be $500,000 with an annual assumed portfolio fee of .5%. The base Social Security benefit at age 65 is assumed to be $25,000, although this is adjusted based on both actual claiming age and future realized inflation (which varies by run). The annual total retirement goal is assumed to be $60,000, which is also adjusted for inflation.

I used an econometric model to simulate future changes in bond yields, which dictate future bond returns. The model targets a 2.5% assumed constant (average) bond yield for the duration of the projection, resulting in approximately a 2.5% bond return and with a 6.0% annual volatility. The return for stocks and inflation is 7.5% and 2.0% respectively, with standard deviations of 15.0% and 1.0%, respectively. The implied correlation among the asset classes is zero. The analysis considers 1,000 runs and ignores taxes. Equity allocations are assumed to evolve based on the Morningstar Moderate index.

Social Security retirement benefits are assumed to be claimed at age 65 unless otherwise noted (i.e., for the delayed claiming scenario). Social Security benefits are assumed to increase annually based on inflation for the previous year, which varies stochastically.

I considered seven strategies, five of which include an allocation to an annuity. While the annuities are assumed to be generic, they are each based on products that are available (they are not purely hypothetical). The annuity allocations are assumed to be 50% of the portfolio balance except for the DIA, which is 20%.

The seven strategies are:

- No annuity;

- No annuity, claim Social Security at age 70 (i.e., delayed claiming). Delayed claiming results in a 43% higher benefit than the base scenario (plus any additional inflation increases) but requires the portfolio to fully fund the retirement income benefit for the first five years of retirement;

- SPIA purchased at retirement with income commencing immediately and with a 15-year period certain benefit (to reflect the fact that very few annuities are life only). A model is developed so that the payout is based on prevailing bond yields at retirement. The payout for the assumed immediate purchase at age 65 is 5.82%;

- DIA purchased immediately with income commencing at age 80. Pricing model assumes a five-year period certain (to effectively replicate a cash refund provision);

- GLWB regular: Includes annual step-ups, both before and after retirement. 5% payout rate (based on income/benefit base), 60% equity allocation, 1.6% annual fee applied to the contract value;

- GLWB lite: No annual step-ups, 5% payout rate based on the greater of the contract value or initial balance at retirement (no assumed contributions), 60% equity allocation, 1.0% annual fee applied to the contract value; and

- PLIB: invested in 60% equities, a 1.25% annual fee applied to the contract value, and a 4.5% initial payout at age 65.

The outcome metric for the analysis is the mortality weighted net present value of income generated from the respective strategies, excluding the base Social Security retirement benefits. Mortality rates are based on the Society of Actuaries 2012 Immediate Annuity Mortality Table with full improvement both to and through retirement. The assumed real discount rate for the analysis is 2%.

Results

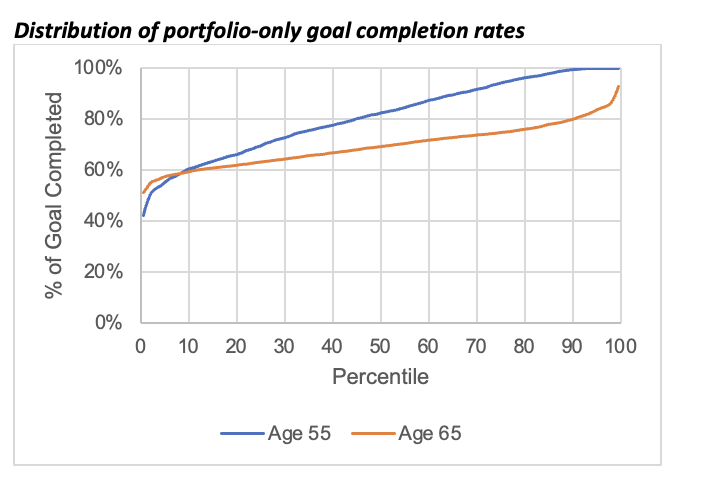

The exhibit below shows the distribution of the percentage of the retirement income goal completed across the 1,000 runs for the retiring-at-age-55 and retiring-at-age-65 scenarios for the portfolio-only strategy. The age 55 goal completion rate is higher than the age 65 goal completion rate because the target income goal is assumed to be the same, in real terms, for both, although the individual has 10 additional years for assets to grow.

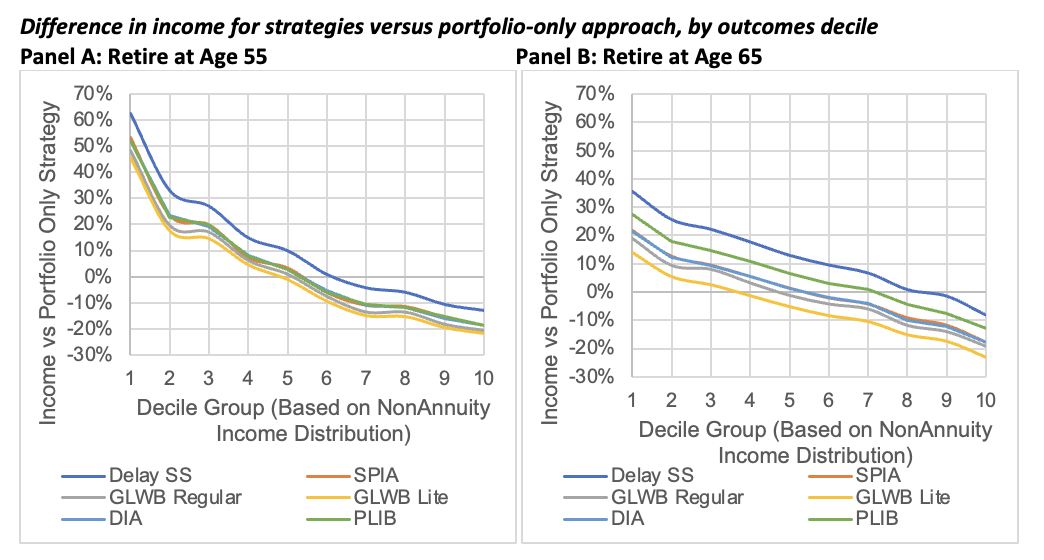

Each run in the subsequent analysis is grouped into deciles based on the relative respective performance of the portfolio-only strategy. For example, the decile 1 group would be the 100 runs where the portfolio-only strategy resulted in the lowest levels of income. This grouping approach allows us to contrast the benefits of allocating to guaranteed income based on different outcome environments, in particular when it is likely most needed (i.e., when the portfolio-only strategy fares the worst).

The exhibit below includes the average difference in mortality weighted net present value of income for the various strategies compared to the base strategy.

Allocating to guaranteed income results in more income when the portfolio does relatively poorly, and vice versa. This context is important; while an annuity isn’t necessarily going to result in more income, on average (since it is a form of insurance), it does result in more income when it is most needed: when the retiree would be most likely to have a shortfall.

The results are relatively monotonic across percentiles, where delayed claiming of Social Security retirement benefits clearly results in the most income, followed by the PLIB strategy, and the SPIA and DIA (which are effectively tied), the GLWB regular strategy, and the GLWB lite is clearly worst among the strategies considered.

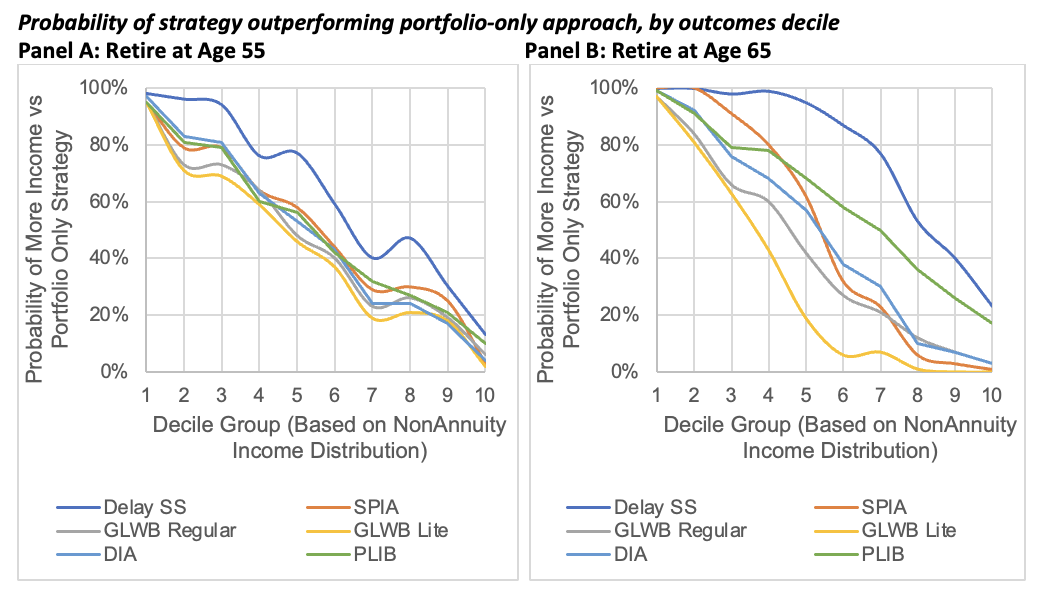

Another perspective is to compare the probabilities of the strategies to generate more income than the portfolio-only approach within each decile. This information is included below.

These results are very similar to the relative-income analysis, where the delayed claiming of Social Security retirement benefits does the best and the GLWB lite does the worst. There is a slight difference in the age-65 scenario, where the SPIA is the second-best strategy (followed by the PLIB) for the lowest four decile groups. This is due to the fact the PLIB strategy income is linked to the market and therefore more negatively affected by lower initial returns than allocating to a SPIA.

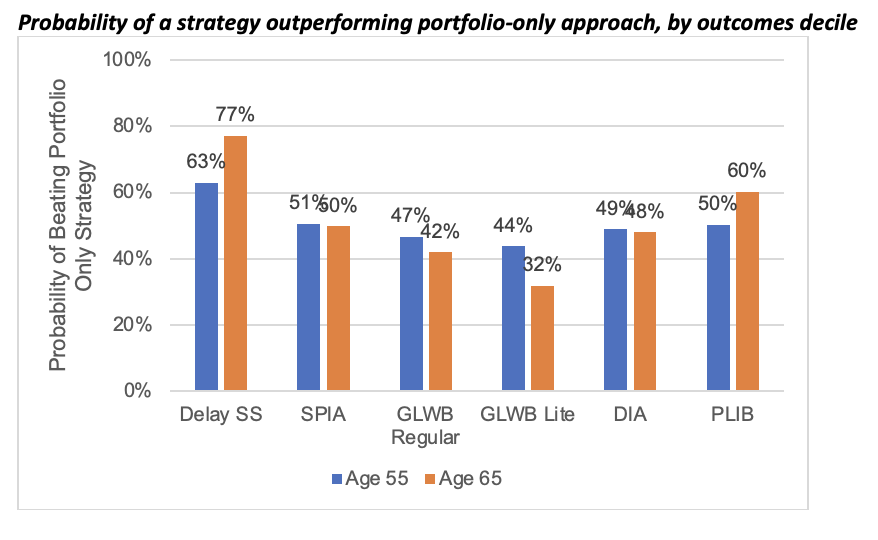

Finally, I provide some context for the probability of the strategies outperforming the portfolio-only approach across all runs below.

Again, these results clearly demonstrate that delayed claiming of Social Security retirement benefits is the most advantageous way for retirees to generate additional guaranteed income. Other approaches can benefit retirees; however, the benefits vary notably by strategy. For example, the outcomes associated with the GLWB lite strategy were categorically the worst almost regardless of the metric considered.

Conclusions

Like any product, all annuities are not created equal. This analysis explores the potential benefit of a variety of approaches to generating additional guaranteed income for a retiree. Delaying claiming of Social Security retirement benefits was clearly the best strategy, while the GLWB lite was clearly the worst. Not only should delayed claiming of Social Security benefits be more actively considered when thinking about allocating to guaranteed income, but conducting due diligence on the expected outcomes of various guaranteed income strategies is also essential before selecting a particular product for a retiree (or DC plan).

David Blanchett, PhD, CFA, CFP®, is managing director and head of retirement research at PGIM DC Solutions. PGIM is the global investment management business of Prudential Financial, Inc.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All