Wall Street has been caught by surprise by a rally in local emerging-market debt, an asset class that’s been largely abandoned by foreign investors after a decade of underperformance.

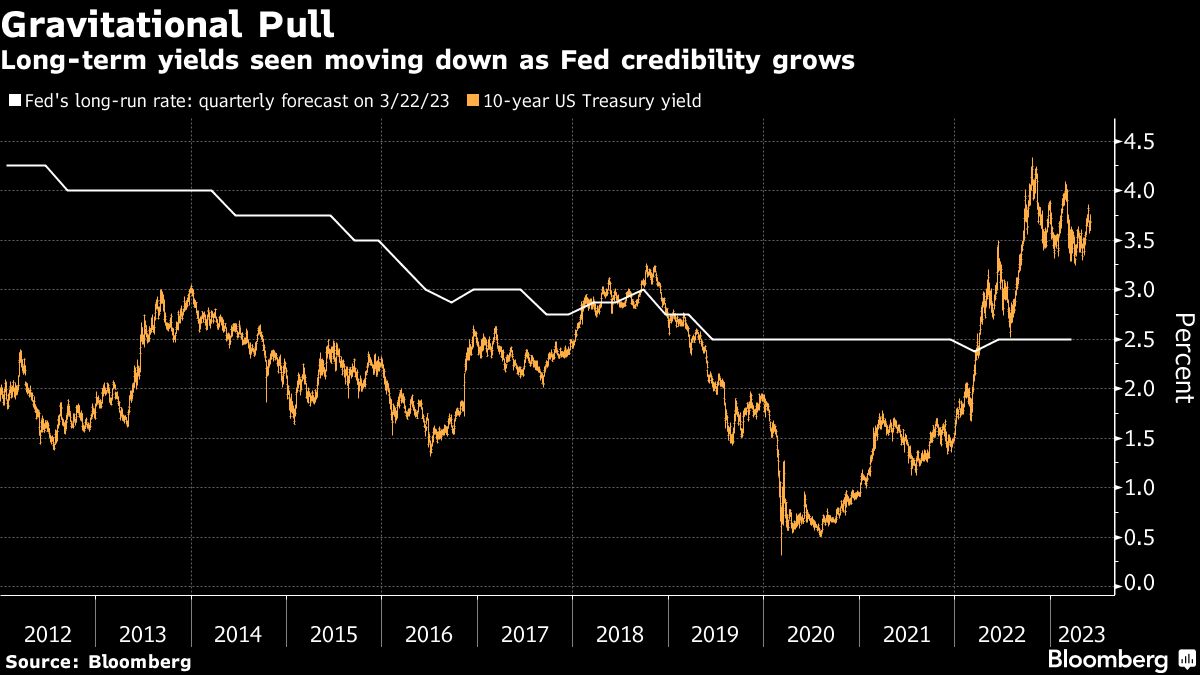

Two years after inflation surged, the Federal Reserve has made limited progress tamping it down. A coterie of investors in the bond market is betting not only that policymakers will win, but that they’re right in anticipating the era of low long-term interest rates will return.

Doug Drabik discusses fixed-income market conditions and offers insight for bond investors.

The passage of the debt-ceiling deal removes a significant threat to the economy and markets. The focus now shifts back to where it’s been for the past 18 months: inflation, the Fed, and recession risks.

The US debt ceiling negotiations brought considerable volatility to market prices.

Improved value proposition in credit.

For over a year, bond traders have been whipsawed by uncertainty about how high the Federal Reserve will push interest rates.

The industry group Airlines for America predicts that approximately 257 million people will travel on U.S. commercial airlines this summer, representing a 9.5% increase from last year. That would also set a new record, as volumes are projected to surpass the summer 2019 levels by around 2 million passengers.

The standoff between the White House and Congress over raising the US debt ceiling has been the talk of the town for months. Now that the government has reached an agreement, savvy investors will be on the hunt for opportunities—and we think there will be some attractive ones.

Choppiness in the equity market continues as investors look to see a debt limit deal approved.

Nick Goetze discusses fixed-income market conditions and offers insight for bond investors.

Wall Street veteran Bob Michele is eyeing opportunities in intermediate government bonds and investment grade credit as the US edges toward a recession by the end of the year.

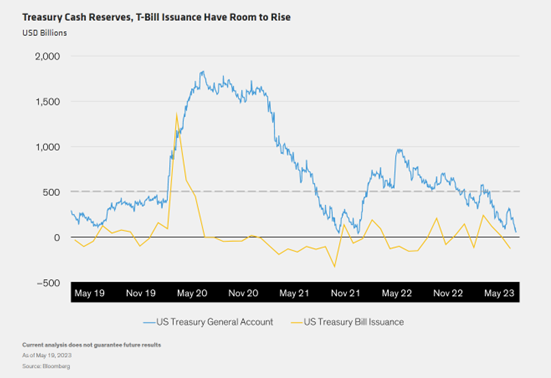

Investors have been loading up on T-bills and money market funds this year, but according to our Total Return team, that is not a sustainable strategy as it exposes investors to both reinvestment risk and inflation while creating an asset/liability mismatch.

Inflation has proven sticky, even as growth weakens. Markets are realizing that policy rates are set to stay higher for longer. We like quality in stocks and bonds.

I received many emails and questions on “why” we are adding the U.S. Treasury bond to our portfolios. The question is understandable, given its dire performance in 2022, where bonds had the biggest drawdown since 1786.

This week, the VettaFi Voices come together for an abbreviated chat about an important topic: the debt ceiling.

Treasury bills maturing in the first half of June rallied as trading resumed following the Memorial Day holiday after a deal to lift the debt ceiling eased concern over the prospect of a calamitous US default.

For this edition of Bull vs. Bear, Elle Caruso and Karrie Gordon discussed the pros and cons of investing in fossil fuels.

The financial markets are giving off mixed signals of late, and credit investors may wonder whether to be downbeat or optimistic.

VettaFi’s Stacey Morris drills into the energy sector and energy ETFs. Candriam’s Alexandra Russo goes in-depth on ESG investing, offering perspective on where it’s gone wrong over the past several years and what the focus should be on moving forward.

Swiss money manager Felix Zulauf is a crowd favorite at SIC. His 2022 presentation was right on target, so I asked him back to tell us what he expects for the rest of 2023 and beyond. Unfortunately, he thinks a slowdown is coming that will hit markets hard.

While we don't expect the U.S. government to default, the uncertainty may heighten market volatility in coming days. Here are answers to some of the questions we're hearing most often.

Republican and White House negotiators are moving closer to an agreement to raise the debt limit and cap federal spending for two years, according to people familiar with the matter, as time grows short to avert a catastrophic US default.

Bonds issued by government-sponsored enterprises can offer slightly higher yields than U.S. Treasuries, without requiring investors to take on too much additional risk.

Rick Rieder and team argue that a series of small, but more probable, wins in fixed income can pave the way for portfolios to outperform benchmarks in 2023.

The semiconductor cycle is dead, long live the super cycle!

Stocks are having a great year, but gold is doing even better. Year-to-date global equities are up roughly 9% in dollar terms; gold has advanced more than 10%.

The two primary styles of dividend investing are growth and yield. In the latter, investors embrace stocks with what are deemed above-average yields — often from slower-growth sectors, such as utilities and real estate.

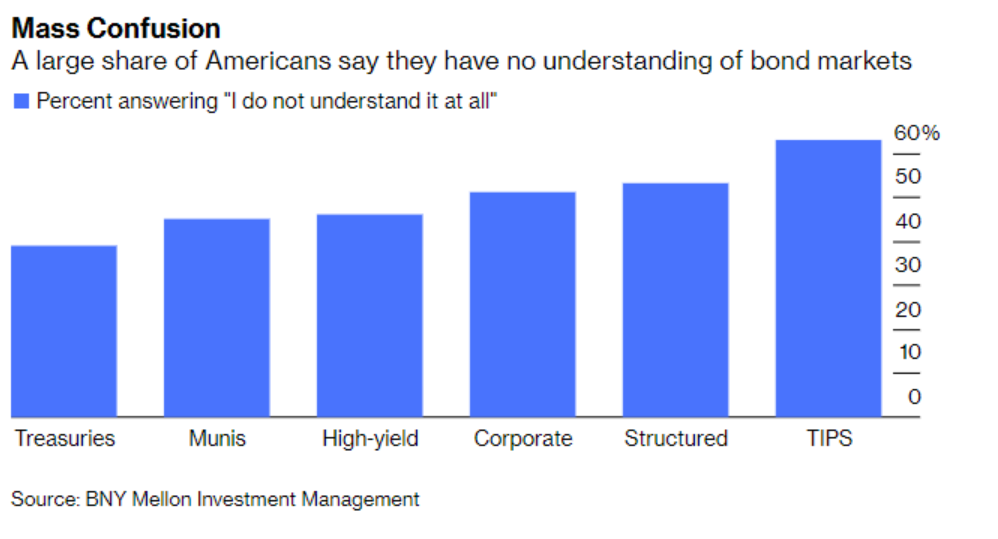

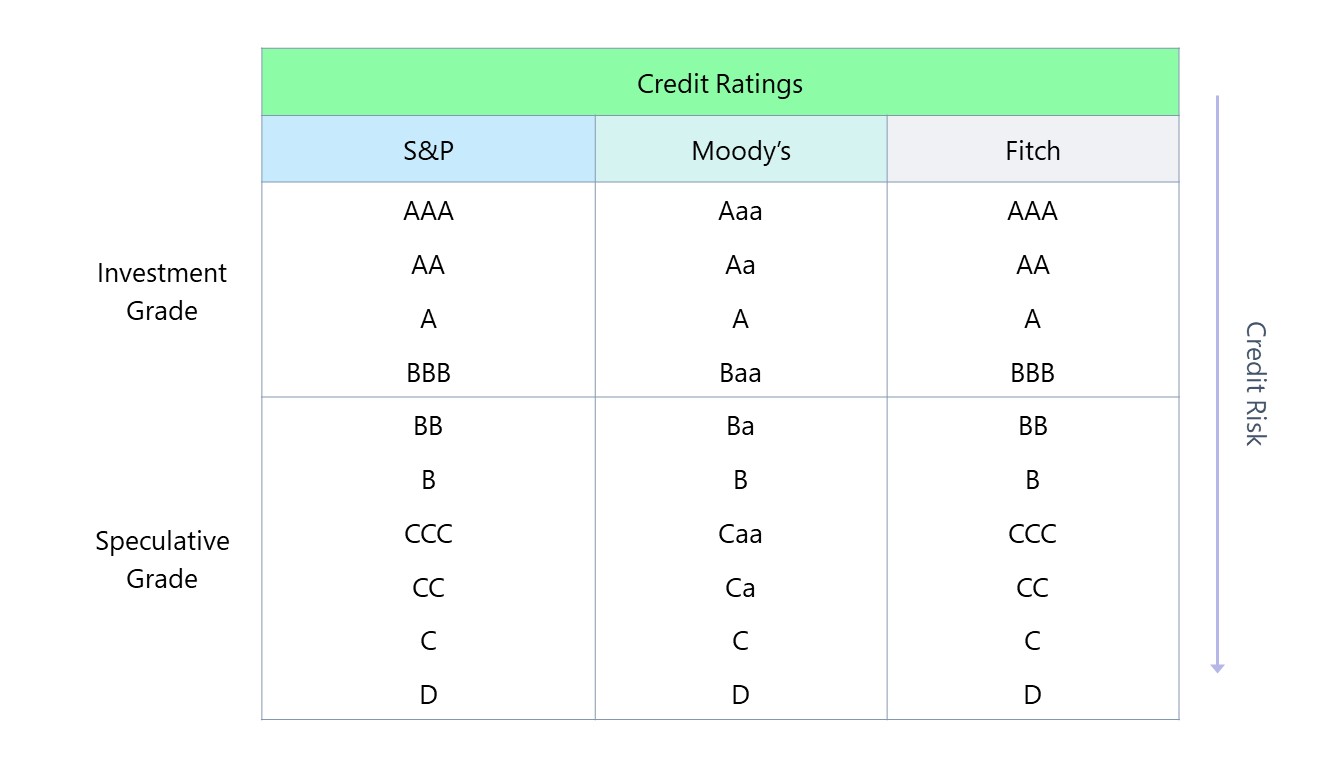

Investors should rely on the wisdom of crowds as expressed through bond yields, not credit rating agencies, to judge fixed-income credit risk.

The tension around the US debt-limit negotiations ratcheted up after Fitch Ratings warned the nation’s AAA rating was under threat from a political standoff that’s preventing a deal.

The 60/40 portfolio – and diversification in general – is undeniably justified.

Most of us spent moments of our childhood, crayon in hand, connecting numbered dots that gradually revealed a picture that we couldn’t deduce simply by looking at the separate dots. With experience, we got better at looking at those isolated dots and mentally connecting them into a coherent “gestalt.”

We prefer private to public credit long term on better return potential. It’s the mirror image in equity: We prefer public stocks as risks fade in the medium term.

The deadline for the #debtceiling is quickly approaching. Where does each side stand? What does each side have to lose? Will a deal get done despite the hardening of partisan lines? Check out what it all means for investors.

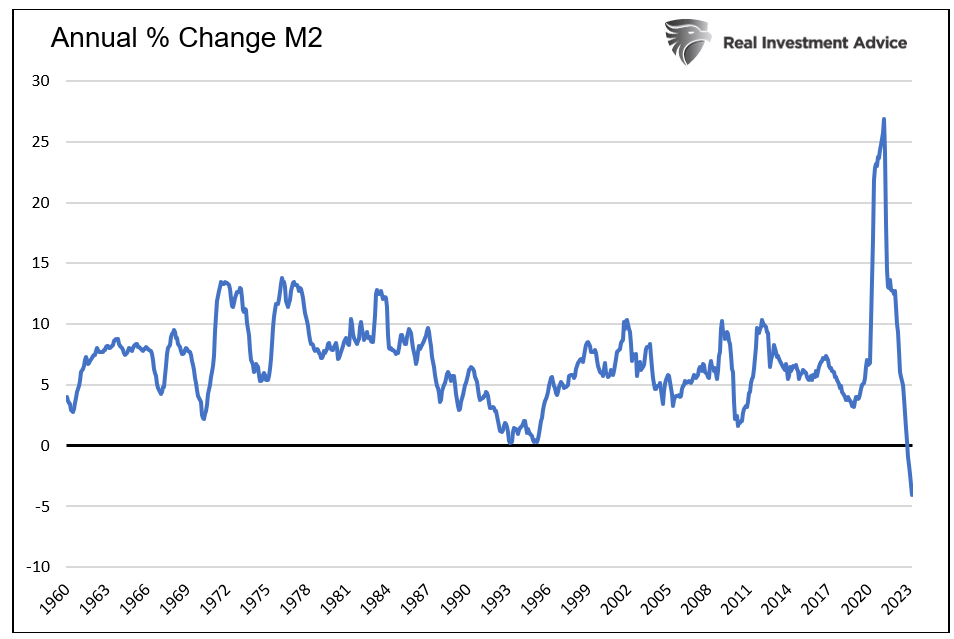

The Fed failed to recognize the danger of its loose monetary policy in 2021. We are seeing its pernicious effect, as the money supply and velocity combined to inflict non-transitory inflation.

Banks and financial institutions are big issuers of preferred securities, so the recent banking industry volatility has had an impact. Our guidance on preferreds is unchanged but with some caveats.

Negotiations among lawmakers in Washington, D.C., to raise the debt ceiling might trend in a more favorable direction.

What generally follows that expression is a succinct synopsis. We’re always trying to be concise; however, distilling complex economic and investment matters usually requires several pages.

When markets turn volatile, it’s not time to despair. Stephen Dover, Head of Franklin Templeton Institute, offers some judicious perspectives on how to turn volatility into opportunity.

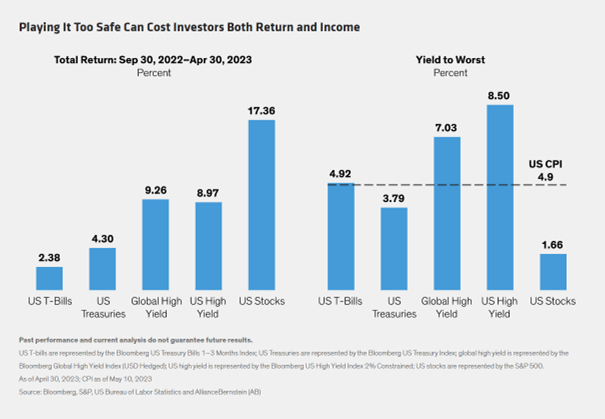

Parking your fixed-income assets in cash may seem like a safe choice in today’s volatile investing environment, but it’s actually a risky proposition. Here are three reasons why sitting on the sidelines can be a dangerous game.

Despite economic uncertainty, we see compelling value in high-quality, liquid assets that we view as more resilient in the face of a potential recession.

Markets are still facing uncertainties regarding the impact of the Federal Reserve’s aggressive rate hikes and quantitative tightening, a potential economic slowdown, and the likelihood of other unforeseen consequences of financial disintermediation.

The Federal Reserve’s latest 0.25% interest-rate hike has likely capped one of its most aggressive policy-tightening cycles in 40 years. And the cumulative 5% policy rate increase in just over a year is now starting to have an effect on rate-sensitive sectors and inflation.

The current economic and investing environment remains one of the most challenging and difficult to navigate in recent times. We have stubborn inflation, economic resilience, geopolitical tensions, tight labour markets, rising interest rates, higher for longer monetary policy, QT, bank failures, overwhelming bearishness and now, issues surrounding the debt ceiling.

VettaFi’s vice chairman Tom Lydon discussed the Global X Russell 2000 Covered Call ETF (RYLD) on this week’s “ETF of the Week” podcast with Chuck Jaffe of “Money Life.”

Rising rates in today's fixed-income markets have led to more attractive bond prices and higher yields, alleviating some of the challenges facing income investors.

If 2022 was the zenith of the post financial crisis bull market, the intervening year and a quarter is a relatively short period from which to conclude that a turn in the secular tide has taken place. That said, several indicators have already begun to signal a change in trend.

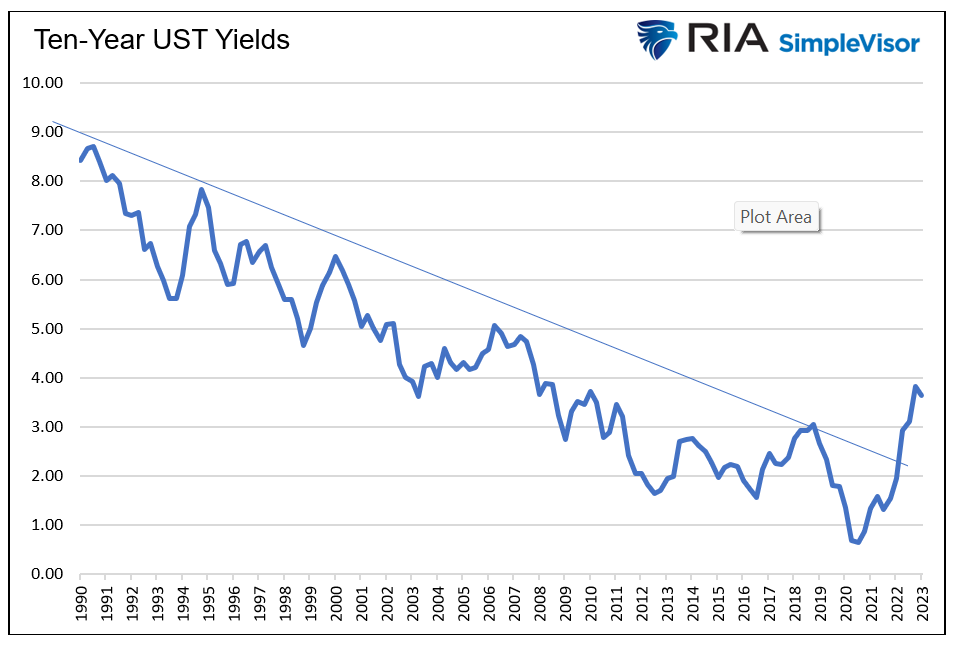

Long-term Treasury bonds are an excellent investment. But timing the purchase of bonds is difficult because three headwinds are keeping rates higher.

Profit margins have remained elevated in the U.S. for a decade, and in a new white paper, GMO’s James Montier examines why that has been the case, ultimately finding the culprit in fiscal deficits.

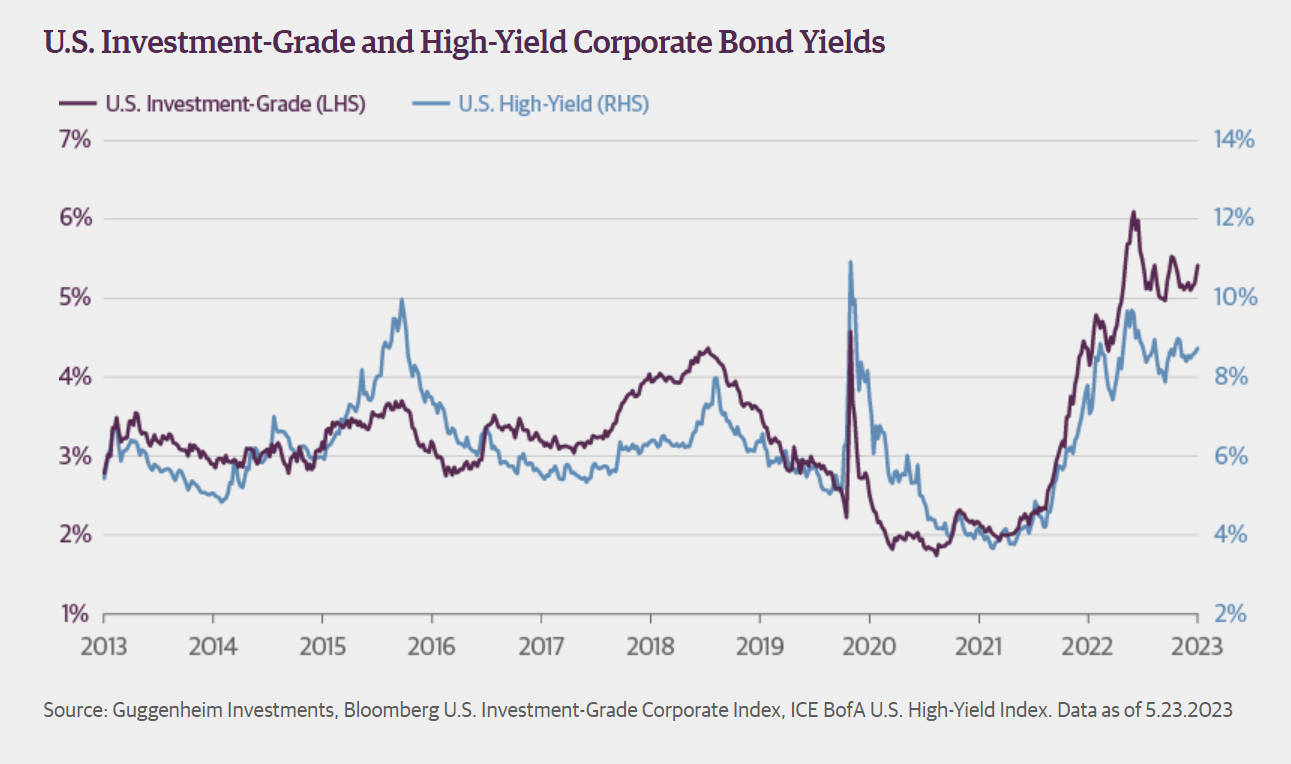

As the US economy begins to feel the weight of the Federal Reserve’s rate hikes, investors have grown leery of US high-yield corporate bonds. On the surface, that makes sense. Historically, credit conditions soured when growth slowed.