It’s Time to Start Playing Investment “Small Ball” in Portfolios

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsKey takeaways

- The idea of bunting (“small ball”) in baseball is that you can, somewhat counterintuitively, build a game-winning strategy through conservative positioning.

- Since the GFC, financial markets had fallen into a dynamic whereby if economic growth, or markets themselves, dropped below trend, then developed market central banks came to the rescue, which allowed investors to take aggressive “home run” swings.

- Today, however, central banks have relatively high and sticky inflation as their focus, and cannot quickly ride to the market’s rescue, at least in the near term, and as such, the risks associated with taking big swings have risen dramatically. That requires a different approach than before for investment success.

Rick Rieder and team argue that a series of small, but more probable, wins in fixed income can pave the way for portfolios to outperform benchmarks in 2023.

The idea of bunting (“small ball”) in baseball is that you can, somewhat counterintuitively, build a game-winning strategy through conservative positioning. Baseball statistics suggest that this is especially important when the stakes are highest, and when margins are the narrowest. When home teams have attempted to bunt with the game tied or trailing by one in extra innings over the past couple of years, the hosts have a 76.9 win percentage when attempting to lay one down and just a 60.4 win percentage when swinging away. Conversely, in games with lower stakes and wider margins, it may not make sense to bunt. In youth baseball, for example, bunting reduces the team’s chance of having a big inning, and big innings often single-handedly win games.

Since the Global Financial Crisis, financial markets had fallen into a dynamic whereby if economic growth, or markets themselves, dropped below trend, then developed market central banks came to the rescue with policy easing, allowing investors to have more certainty in positive long-term outcomes. This widespread expectation created a “buy-the-dip” framework around financial assets, incentivizing many investors to take aggressive “home run” swings, knowing that volatility was contained on the downside.

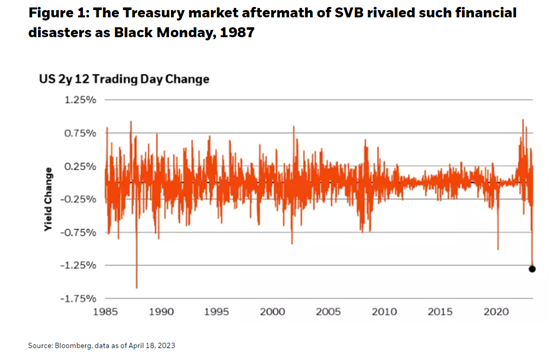

Today, however, central banks have relatively high and sticky inflation as their focus, and cannot quickly ride to the market’s rescue, at least in the near term. Furthermore, the margins between seemingly disparate economic outcomes like a “hard landing” and “soft landing” are as narrow as they have been in decades, not unlike a tied baseball game in extra innings (according to Bloomberg consensus forecasts, U.S. real GDP is likely to hover by a hairsbreadth above 0% for the second half of 2023 and first half of 2024). That, along with the natural economic and financial market stresses that come with the most rapid monetary policy rate hiking cycle in more than 40 years for developed markets, have resulted in historic market volatility (see Figure 1) and some breakages in areas. For investors, the risks associated with taking big swings have risen dramatically.

In the U.S. the most recent breakage began with the “digital bank run” on Silicon Valley Bank (SVB) on March 8, resulting in the largest bank failure since 2008. It wasn’t long before stresses were seen in European markets – by mid-March the Swiss National Bank had helped broker the sale of embattled Credit Suisse to rival UBS. On many measures, the month of March 2023 proved to be one of the most volatile on record. Yet, unlike anything we’ve witnessed in recent history, this volatility originated in risk-free rates. As a case in point, there have been just four days in the past 25 years that have seen the 2-Year U.S. Treasury yield move by 50 basis points (bps) or more on an intraday basis, and three were in the week of March 13 (the other was in September 2008). Rate volatility has been remarkably high, while at the same time, liquidity has been very poor. While we don’t think this recent market volatility will be the new normal, it requires more assertive risk management.

While higher interest rates and higher interest rate volatility have begun to injure certain sectors around the globe, broadly speaking, GDP is less sensitive to interest rate changes than is bank lending, where when rates are shocked higher (alongside an inverted yield curve), financial transmission can become less predictable and more volatile. Still, with the cost of financing has increased so sharply, it has left the value of riskier assets, and the cost of refinancing associated liabilities, more difficult to gauge with precision. When asset values decline relative to sticky or rising liability values, equity capital becomes impaired.

In order to understand how these breakages might be resolved, it is important to understand how they occurred. As bank deposits surged in recent years due to pandemic-era stimulus checks and pent-up savings, banks could not make enough loans to keep up with deposit growth and instead purchased securities at low yields (relative to the 0% yields on deposits). Then, as the Fed rapidly raised policy rates to combat elevated inflation while also initiating Quantitative Tightening (QT), banks have struggled with mark-to-market losses on securities, as well as with the prospect of falling collateral values.

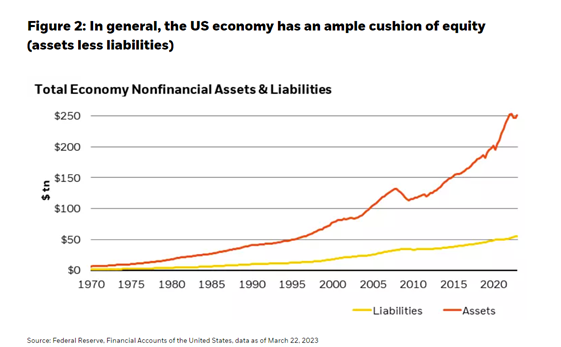

The fact is that attractive short-end risk-free rates have drawn money away from both bank deposits and risky assets, and QT has led to a contracting money supply, which could leave both the financial economy and the real economy vulnerable to a liquidity squeeze. If the restrictive monetary policy goes too far, then the thinnest parts of the capital structure (the equity slice) can become exposed, raising the risk of a shock that could become contagious, a glimpse of which we’ve seen in the regional bank space. Most sectors in the U.S. economy have an ample cushion of equity, but as monetary policy tightening continues to pass through the system, policymakers risk exposing (or even creating) imbalances (see Figure 2). The Fed must take on the difficult task of both continuing its inflation fight while remaining considerate of the broader risks to the economy.

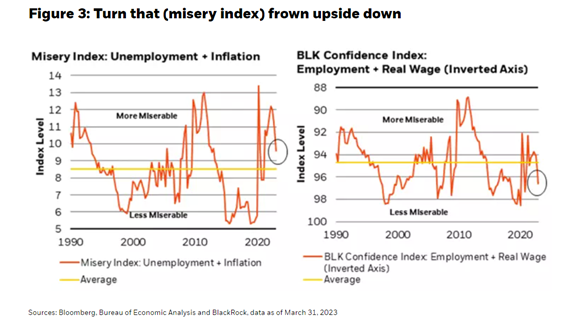

There are also significant positives that ought to be preserved, such as the health of the labor market. While the central bank’s mandate is to a) maximize employment, and b) maintain price stability, this could be rewritten as “to maximize real income growth for as many as possible.” If so, the “misery index” of unemployment and inflation, which isn’t very flattering, could be rewritten as a “confidence index” of employment and real wage growth (see Figure 3). While this is a subtle switch, it makes a material difference. The former is “more miserable” (than the average since the 1990s) and the latter is “less miserable” (than the average since the 1990s). The reason? While above-target inflation is generally undesirable, it’s not so bad if wages are outpacing inflation, which is in fact the case today. The real economy, especially the labor market, has been able to maintain enough flexibility to overcome this period of inflationary stress.

We believe it is not interest rates, excess savings, or commercial real estate that underpins the U.S. economy, but aggregate real wage growth. While the blunt misery index suggests we are in a situation closer to the 2008 GFC, our “confidence index” suggests we are closer to the pre-Covid period or even the late 1990s. From the perspective of employment and real wages, not a lot has to be done on the policy front from here, despite a surprisingly pervasive, perhaps even myopic focus, on inflation as the unilateral risk, goal, or objective of policy today. How the Fed interprets the tradeoff between inflation and employment from here is very important for investing.

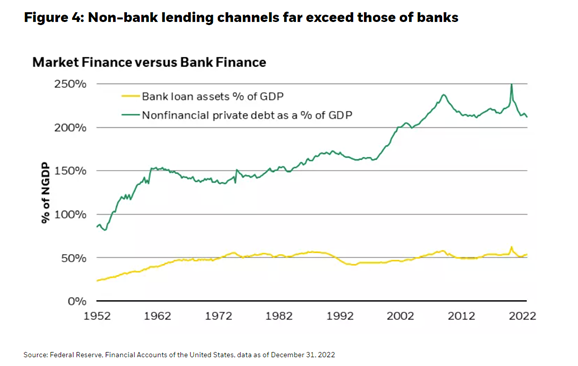

A third input into that tradeoff is financial system stability. When we’re thinking about whether the financial system is well capitalized, we need to look across a wide range of institutions. It’s important to recognize how the modern financial economy “spreads out” risks to different segments of the aggregate credit creation system. For instance, while the banking system in Europe is a critical channel of corporate credit funding (as it is to a degree in the U.S. too, particularly for small-to-mid-sized businesses), in the U.S. non-banking entities (often referred to as “shadow banks”) play an extraordinarily important role in credit intermediation (see Figure 4). Further, it’s important to note that this nomenclature is a bit misleading, as there is nothing “shadowy” about much of the non-bank sector, and many of these entities are unleveled, nor do they always have riskier funding profiles. The creation of a robust and varied non-banking sector, in fact, is a development that has reshaped policy and regulatory behavior, and in many respects, the system has proven resilient to most shocks.

At this stage in the economic cycle, we think that there’s roughly a 75% likelihood of avoiding a pernicious and systemic credit tightening this year so that the financial system stress we witnessed in March and early May alleviates over time and the economic/financial ecosystem adapts and adjusts to a new set of influences, including a structurally smaller regional banking credit creation channel. Within this more benign scenario, there’s still a decent chance that inflation remains sticky high, and the developed market central banks are forced to push rates higher than currently expected, which would lead to some market stresses, but not to a chaotic degree.

That leaves us with a 25% chance of potentially systemic credit tightening that leads to a vicious cycle of declining asset prices, increased refinancing costs for liabilities, and shrinking equity values in vulnerable sectors: essentially leaving global liquidity in short supply. Within this more dire scenario, we think there’s a significant chance (say about 80% odds) that inflation moderates as we enter a technical recession, and risk premia widen accordingly, prompting the Federal Reserve and European Central Bank (ECB) to reduce policy rates significantly, leading to rallying rates markets. The more troubling outcome is the possibility of stagflation: at a roughly 5% likelihood overall, it’s more than a mere tail risk, in which risk premia widens together with longer-dated interest rates, reflecting the persistence of inflation. This latter outcome is clearly not our base case, but it is a worrying possibility.

While the ECB is not yet finished tightening policy rates in its attempt to tame European inflation, there is a heightened focus on credit conditions after the Credit Suisse fire sale. The ECB recently reaffirmed a “separation principle,” whereby it argues that liquidity tools are most appropriately used for financial stability concerns, while the interest rate tool is the primary focus of monetary policy. Thus, while credit creation in Europe is turning down rapidly, absent a sudden stop in credit flow from a major financial stability event, the ECB will likely continue on its current path of rate hiking. We like having some exposure to the Euro in sympathy with a potentially longer ECB hiking cycle and narrower U.S.-EU rate differential.

What does playing “small ball” in Fixed Income mean?

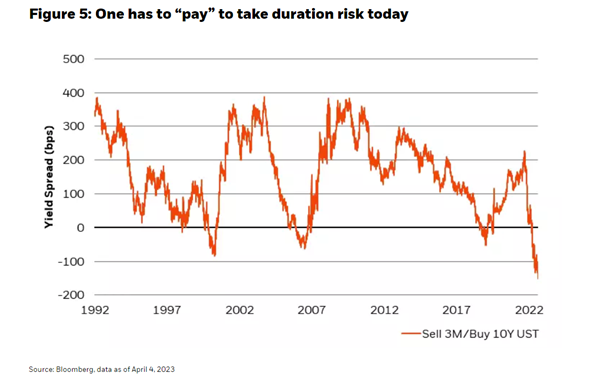

The compensation for taking duration (interest rate) risk in Fixed Income is the least it’s been in decades due to severely inverted yield curves (see Figure 5). Put another way, the cost of owning duration today is high relative to holding cash. Indeed, 9- to 12-month commercial paper markets in the U.S. are yielding around 5.75%, with minimal duration, credit, or liquidity risk in many cases, whereas the highly interest-rate sensitive 10-Year U.S. Treasury is yielding less than 3.50%, a remarkable contrast. So, high-quality and more liquid assets should today comprise a greater portion of a portfolio. Still, the hedge effectiveness of duration has been restored to portfolios overall, given the non-zero downside risks to the economic outlook in our view, so modest duration positions can help protect the equity portions of balanced portfolios (i.e., use duration as a hedge rather than an investment).

To that end, the higher-quality segments of shorter-end Investment-Grade credit positions in U.S. and European corporates also look attractive. And while we think it makes sense to be very selective in high-yield positions, which should be modestly sized, we prefer Euro area high yield today.

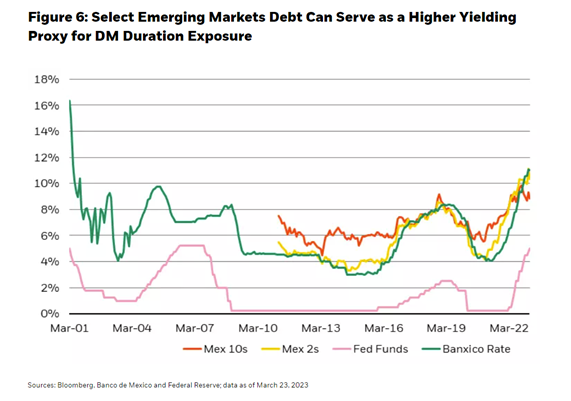

Another area where we’re finding select opportunities today is in the locally denominated debt of some Emerging Markets countries, such as Mexico, Brazil, and South Africa. While EM can be a highly volatile asset class, with greater degrees of unpredictability to it, some regions of the market also strike us as a much higher yielding proxy for developed market duration exposure. In fact, historically speaking the Mexican central bank (Banxico) policy path tends to migrate toward that of the Fed over time, with both central banks likely nearing the end of their hiking cycles imminently (see Figure 6).

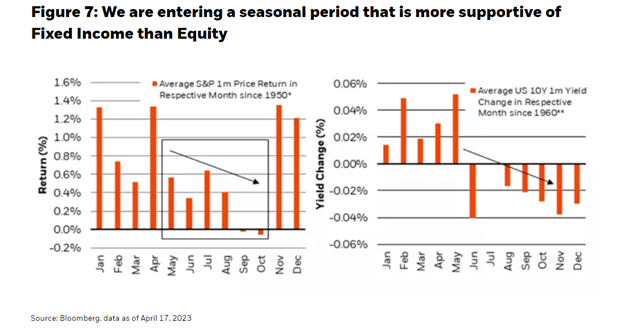

In a nutshell, 2023 has been typified by shocks to the system, a lack of conviction, and inconsistent levels of liquidity. Historically, hitting a home run has often meant getting more yield in small, less liquid markets like high yield, but today we like the valuations and the depth of high-quality, liquid markets, particularly at this time of year, as seasonal patterns turn more challenging (see Figure 7). In our view, when the opportunity to take a smaller, but much more certain, win comes around, it ought to be taken.

Over the past 15 years, it has been difficult to find ‘small ball’ or high-quality opportunities where large chunks of short-duration assets and high levels of liquidity threw off as much income as they do today. Are investors guaranteed to ‘score runs and win the game’ here? No… but we believe that by taking a conservative approach, it would be difficult not to eventually find a path to victory, either now or in the future. By playing a lot of ‘small ball’ (holding a defensive posture) and owning some duration in portfolios, we think it could pave the way for hitting some “home runs” through aggressive carry in EM and/or higher beta through select equities.

Investing involves risks, including possible loss of principal. Past performance is no guarantee of future results. Index performance is shown for illustrative purposes only. It is not possible to invest directly in an index.

Fixed income risks include interest rate and credit risk. Typically, when interest rates rise, there is a corresponding decline in bond values. Credit risk refers to the possibility that the bond issuer will not be able to make principal and interest payments. International investing involves risks, including risks related to foreign currency, limited liquidity, less government regulation, and the possibility of substantial volatility due to adverse political, economic, or other developments. These risks may be heightened for investments in emerging markets. International investing involves risks, including risks related to foreign currency, limited liquidity, less government regulation, and the possibility of substantial volatility due to adverse political, economic, or other developments. These risks may be heightened for investments in emerging markets.

This material is not intended to be relied upon as a forecast, research, or investment advice, and is not a recommendation, offer, or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of May 8, 2023, and may change as subsequent conditions vary. The information and opinions contained in this commentary are derived from proprietary and non-proprietary sources deemed by BlackRock to be reliable, are not necessarily all-inclusive, and are not guaranteed accurate. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by BlackRock, its officers, employees, or agents.

This commentary may contain “forward-looking” information that is not purely historical in nature. Such information may include, among other things, projections, and forecasts. There is no guarantee that any forecasts made will come to pass. Reliance upon information in this post is at the sole discretion of the reader.

Prepared by BlackRock Investments, Inc. LLC. Member FINRA

©2023 BlackRock, Inc. All rights reserved. BLACKROCK is a trademark of BlackRock, Inc., or its subsidiaries in the United States and elsewhere. All other marks are the property of their respective owners.

A message from Advisor Perspectives and VettaFi: To learn more about this or other topics, please check out our most recent white papers.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All