The Federal Reserve’s latest 0.25% interest-rate hike has likely capped one of its most aggressive policy-tightening cycles in 40 years. And the cumulative 5% policy rate increase in just over a year is now starting to have an effect on rate-sensitive sectors and inflation.

Headline inflation has peaked in most major economies, mostly thanks to cheaper commodities. Core inflation, which excludes the more volatile energy and food prices, remains historically high but has leveled off. Consumers are already seeing improvements in real spending power. As a result, we expect inflation to continue to decline in the coming months—with ramifications for diversified multi-asset investment strategies.

Banking Woes Could Help Pull Inflation Down

Tighter credit conditions emerging from the banking sector crisis, which triggered a rapid repricing of interest-rate expectations in March, may add to disinflationary forces. We think the banking scenario certainly bears watching, but we don’t see this as a 2008-style meltdown. And with central banks pausing rate hikes there’s greater visibility on where rates are headed, which may add stability to financial markets.

Falling Housing Costs Finally Make an Impression

Housing has been one of the more persistent drivers of rising inflation over the past year, and we’re encouraged that the year-over-year increase in house prices may have peaked (Display). This was generally expected. Home purchase price increases as well as rents on new leases (green line), which show up in price indices (blue line) with about a one-year lag, peaked in early 2022. Based on broad indicators and our proprietary model (yellow line), we believe housing inflation will continue to normalize through 2023 and play a big role in bringing inflation down.

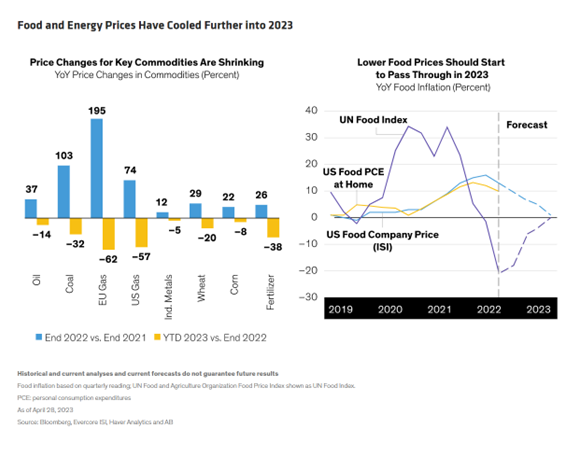

Lower Commodities Prices Are Being Felt Too

It can also take time for changes in input costs to pass through to end consumers. For example, global commodities prices have dropped significantly from their peaks, with wheat down 20% in the first four months of 2023 (Display, left). However, that decline is only now being passed through, especially to food prices (Display, right). Food commodity inflation rates (purple line), which have declined sharply since March 2022, are now well into deflationary territory.

But inflation in food costs for end consumers (gold line) peaked five months after food-commodity inflation reached its high point. Even if commodity prices stay at current levels, price increases from US food companies (blue line) are expected to drop back to normal ranges. In other words, we believe consumers will continue to see slowing price increases for consumer staples and food services over the next 12 months.

Aligning Equity Allocations to Inflation’s Changing Trajectory

Many inputs guide multi-asset allocation decisions, but the inflationary shock of the past couple of years has driven extreme volatility and disruption of cross-asset relationships. As the economic and investment climate shifts, tactical asset allocation decisions may enhance a portfolio’s risk/return profile.

Growth assets, such as equities, have become more appealing as inflation starts to normalize along with more stable policy rates. Corporate earnings growth has likely bottomed in the first quarter; about 78% of the S&P 500 companies reporting so far have beaten estimates, according to FactSet, and many expect to see improving earnings growth in the second half of the year. So, if inflation continues to normalize and a prolonged recession can be avoided, it could help drive a further recovery in equity markets.

We see uniquely attractive characteristics in each of the regional markets, such as the US for its high-quality fundamentals and margins, Europe for its cyclical growth, and now China. As the world’s largest emerging market, China is rebounding since lifting its zero-COVID lockdowns. This on its own should bolster global growth prospects going forward.

Adapting Fixed-Income Exposure and Portfolio Diversifiers

After a painful period of rapidly rising interest rates, bond yields may have peaked, making entry points for corporate and sovereign bonds the most appealing they’ve been in years.

We think moderate exposure to short-duration (or interest-rate risk) makes sense in this environment. We also favor US Treasuries, which have once again become effective diversifiers to equity exposure as peak policy rates come into view. Wide yield spreads for global corporate high-yield bonds keep them compelling, and we think the emphasis should be on issuers with solid corporate fundamentals, especially in a low-growth world.

Severe underperformance and the lack of a diversification benefit from bonds in 2022 prompted many investors to broaden the field of portfolio diversifiers. Real assets, such as real estate and commodities, as well as cross-sectional currency and equity factor strategies offer potential diversifying return streams. Within equities, given our expectation of a slow-growth, falling-yield environment, we think a tilt toward quality and profitability is warranted. We believe 2022’s US dollar outperformance is likely to unwind during the year while improving economic growth, which bodes well for the euro in the near term.

It’s been a frustrating two years of rising rates and inflation for investors, and the Fed’s stance remains cautiously optimistic. But we think data are consistent with the potential for further normalization in inflation, while sentiment points to some resilience in growth prospects. This will have implications for multi-asset strategies, requiring a dynamic approach that balances adjustments in strategic and tactical positioning.

The views expressed herein do not constitute research, investment advice, or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams, and are subject to revision over time.

A message from Advisor Perspectives and Vetta Fi: To learn more on this and other topics, check out our full schedule of upcoming CE-approved virtual events.

© AllianceBernstein

Read more commentaries by AllianceBernstein