Investors are plowing into technology-tracking ETFs at a record clip as conviction builds that the market’s biggest stocks can thrive in almost any economic cycle.

Panagram’s John Kim goes in depth on the collateralized loan obligation market and CLO ETFs. VettaFi’s Zeno Mercer highlights recent earnings reports from several of the biggest players in artificial intelligence and discusses AI-related ETFs.

Momentum traders are modeled to buy equities over the next week regardless of market direction, according to Goldman Sachs Group Inc.’s trading desk.

While high-yield implies higher risk when it comes to bonds, HYD, which turned 15 years old in February, isn’t excessively risky.

Various methods to estimate this key bond market gauge differ on details but appear to signal rising investor compensation.

Rising temperatures will soon render increasing parts of the world uninhabitable.

This week is part two of our conversation about alternative investments. As I pointed out last week, this space has evolved into a distinct asset class of its own. I believe investors need to understand the good, the bad, and the ugly aspects of investing in alternatives.

In case you missed it, a $5 trillion tax hike looms over American households and businesses in President Joe Biden’s latest budget proposal, which would include a 25% annual minimum tax on unrealized capital gains for individuals with incomes and assets exceeding $100 million.

Amid higher interest rates and consequently higher yields, investors have piled into cash. My guest today will explain why it’s time to make a move. His position is that cash should be an asset to provide for short-term (less than 12 months) liquidity needs. Beyond that, investors should consider an appropriately diversified portfolio to achieve their financial goals. While short-term performance may work in investors’ favor, he will argue that over the long term, the benefits of being invested outweigh the potential short-term benefits of sitting in cash.

As equity volatility and market uncertainty continue, investors increasingly turn to equity income strategies for opportunity.

Free cash flow ETFs VFLO and SFLO can be used to introduce factors to a portfolio. The funds offer exposures to quality, value, and growth.

With inflation up, economic growth down and two-year Treasury yields testing 5%, Bill Gross sensed the music in markets was fading, and said it was time to get over the likes of the Magnificent Seven.

Markets are supposed to be forward-looking, so it’s a bit of a mystery that bonds sold off as dramatically as they did on evidence that bad first-quarter inflation was worse than previously understood.

Why should anyone be allocating to investment-grade corporate bonds right now?

Demand for Treasuries is holding up as the US government floods the market with more than $180 billion of new debt this week, a testament to the appeal of high yields for shorter-term notes.

We believe high-yield munis carry additional risks, but are worth consideration by investors in higher tax brackets who are comfortable taking added risks.

The market has been highly tuned to news from the Fed or developments in artificial intelligence technology to set expectations.

It was an irresistible pitch. Give us your money, executives at Ray Dalio’s Bridgewater Associates and other hedge funds said, and we’ll funnel it into a money-minting, sure-thing strategy for the long haul.

Don’t believe the economic consensus, according to David Rosenberg. A recession is much more likely than a soft landing, and investors should allocate to 10-year Treasury bonds instead of stocks.

We demystify the credit risk transfer securities market.

The dynamics of fiscal and monetary policy are now entering a new phase. Due to the emergence of negative Net National Saving (NNS), the law of diminishing returns can no longer fully capture the harmful effect of debt on economic growth.

Even if higher-for-longer interest rates are applying downward pressure on prices, bonds still look enticing.

Timing has never been a crucial undertaking for fixed income allocations dedicated to asset preservation largely because this is a long-term endeavor dedicated to keeping an investor’s wealth intact.

Rising interest rates and the fear of giving back stock market gains are pushing pension fund managers to move capital from stocks to bonds.

In this article, Russ Koesterich discusses why a higher rate environment may still allow stocks to end the year higher.

We put the recent market movements in perspective, which have been driven by time (it has been a while since we had a 5%+ pullback), overly optimistic, complacent market sentiment, and higher Treasury yields amid persistent inflationary pressures and signs of a more patient Fed.

The world’s financial markets are encountering a force they didn’t bet on for 2024: A strong dollar is back and looks set to stay.

When the Federal Reserve flooded the economy with cash during the Covid-19 pandemic it exacerbated a problem for America’s largest banks: What to do with all the extra deposits.

The melding of yield and rate risk mitigation is available in the Vanguard Intermediate-Term Bond ETF (BIV).

The Federal Reserve is expected to lower interest rates, but the economy and stock market don't need stimulation.

Our outlook on the 11 S&P 500 equity sectors.

Monetary authorities saved the day again in the first quarter, but over-reliance on them is looking to be increasingly risky for investors. The new boss is geopolitics and that is where investors should be looking for guidance.

Copper is trading at a 52-week high, oil is above $90 a barrel and the S&P 500 Energy Index just hit a fresh all-time high.

Inflation concerns are top of mind again, with consumer prices and producer prices rising higher last week.

So far this year, the US equity market has shown remarkable resilience and US inflation has remained sticky. Against this backdrop, a recent survey of our chief investment officers offers analyses and perspectives on key areas, such as Federal Reserve rate cut expectations, geopolitical risks, uncertain corporate earnings and opportunities in different asset classes.

Three months of discouraging inflation data coupled with some hot economic data points are considered headwinds for U.S. Treasurys.

A string of disappointing inflation data has forced the Federal Reserve to reset the clock on its first interest-rate cut and re-evaluate the trajectory of price growth.

Ben Graham, the value investor and Warren Buffett mentor, famously said the market is like a voting machine in the short run, but “in the long run it becomes a weighing machine.”

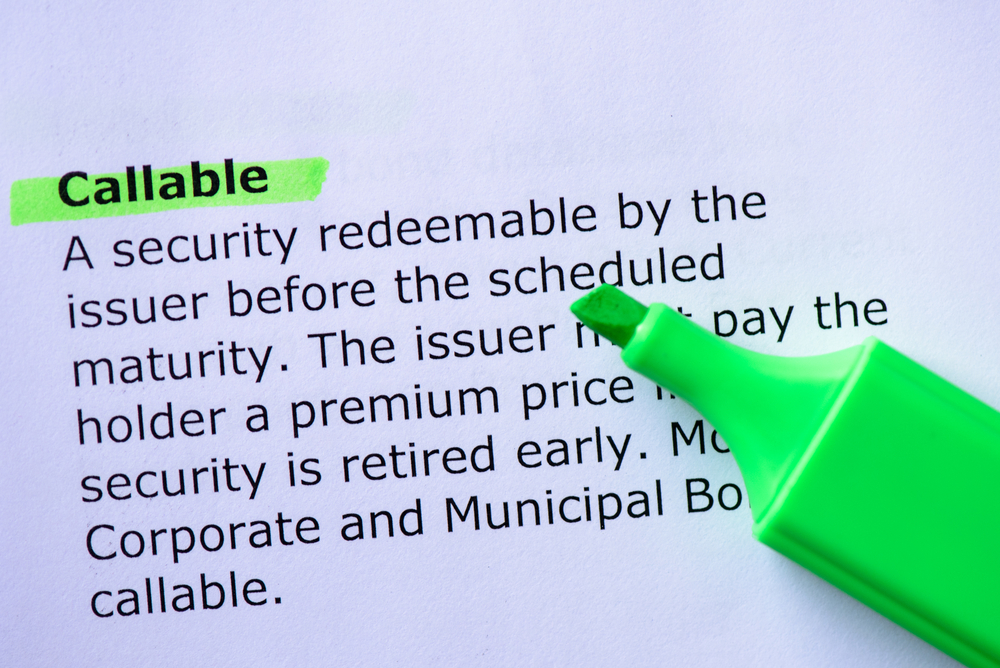

Reviewing the basics can keep you from being caught off guard if your investment is returned to you before the stated maturity date.

In this edition of Bull vs. Bear, staff writers Nick Wodeshick and Nick Peters-Golden ask whether rate cuts will still happen in 2024.

Q2 weakness is causing traders to up their bearish bets on bond prices, but it presents an opportunity for value-seeking investors.

When does a strong dollar become too strong? “Right now” would be the cry of most emerging-market currencies, not to mention policymakers in Japan. Even the European Central Bank says it’s paying attention to the foreign exchange market.

The highest US yields since November are beginning to attract some opportunistic buyers, even as negative sentiment remains firmly entrenched throughout the Treasury bond market.

The Northern Trust Economics team shares its outlook for U.S. growth, employment, interest rates and inflation.

The Chinese yuan is softening in line with the nation's economic outlook.

Advisors weigh in on how you should approach account withdrawals after retirement in order to make your assets last.

It appears investors are heading for the exits on U.S. Treasuries and towards the entranceway of European bonds.

Federal Reserve Chair Jerome Powell is making life tougher for his peers around the world as the prospect of higher-for-longer US interest rates reduces room for easier policy elsewhere.

With the end of great inflation scare in sight, it's time the central bank hive mind contemplated what it might learn from the failure of its economic models.

Fed Funds Rate: According to Bloomberg calculations based on where Fed Funds futures are currently trading, there is a 20% chance that the FOMC cuts the overnight rate in June and a ~50% chance that they cut in July.