With the end of great inflation scare in sight, it's time the central bank hive mind contemplated what it might learn from the failure of its economic models.

The most obvious lesson: Steering multitrillion-dollar economies to land with laser precision onto a 2% inflation pin needs to be abandoned. Economic and geopolitical uncertainty necessitates a monetary system that can roll with the punches. A flexible inflation range that reflects reality should supersede an unhealthy fixation on one constant. Trying to fit all economic variables around one peg is futile.

I don’t mean that inflation should be allowed to rip. But price targeting could be put back where it belongs — as part of a wider monetary policy toolkit, not the one-tool-to-rule-them-all. The better solution lies in a combination of fiscal policy restraint and using a selection of monetary instruments — back to the future, if you will, as ranges used to be the norm. Happily, there is a recent precedent that the Federal Reserve trialed in the early part of Chair Jerome Powell's tenure.

Flexible Average Inflation Targeting was introduced by the Federal Open Market Committee in August 2020. It was abandoned amid the pandemic and surge in energy prices before it really had a chance to embed. Its initial aim was to allow the economy to run a little hot if the preceding period had been of too-low inflation, or indeed vice versa. No doubt with hindsight there may have been some drawbacks but a calm dissembling of what could work better in a more normal environment would be practical.

An external energy inflation shock evidently meant it wasn't the right time to fiddle with a new monetary regime. Now that it's subsided, a rethink is in order. A gradual wider range could deliver more predictable results. This could be tweaked if changing economic conditions dictated — without upending the benefits that rigorous inflation targeting have afforded for commercial and investment planning.

There's no mad rush and certainly some central banks, like the Fed, can do this when prices are undeniably under control. My Bloomberg Opinion colleague, Mohamed A. El-Erian, wrote last week the Fed should steer toward a slow "transition to an inflation target based on a range, say 2-3%.” That would be a conservative approach that could be widened over time. One size doesn’t fit all economies.

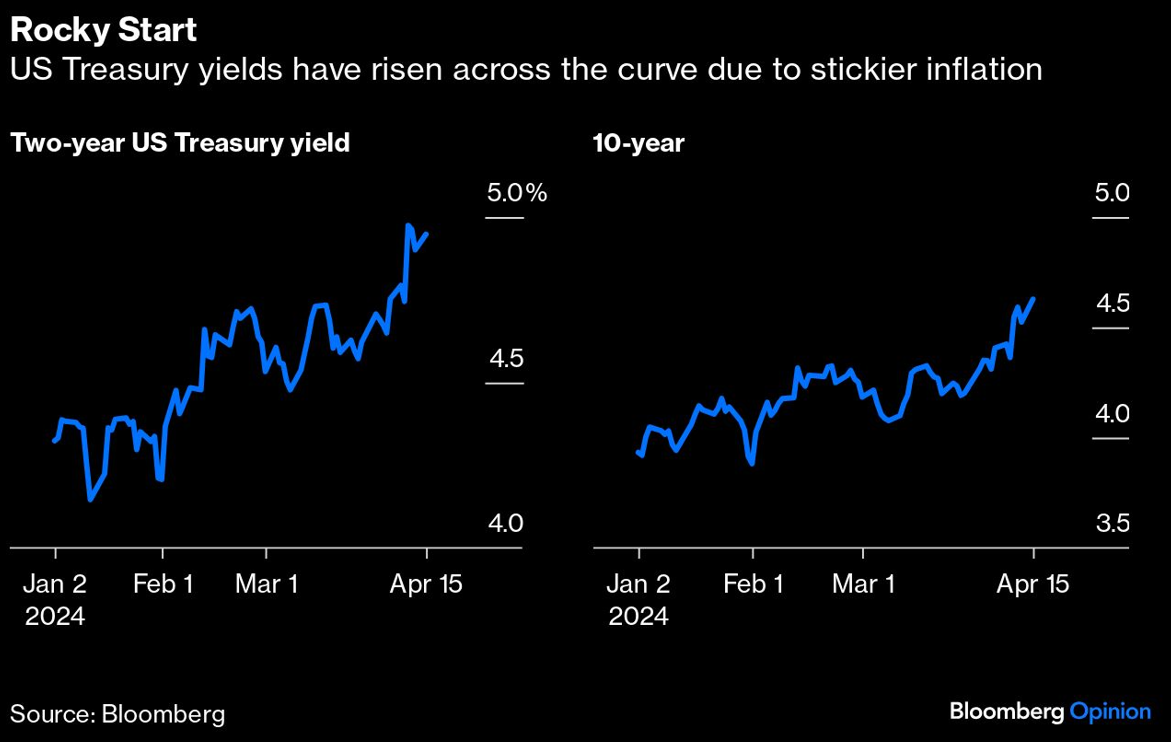

Some marginal forecast misses on US inflation this year have sent global interest-rate markets into a flat spin, which is now bleeding into equity markets. US Treasury yields have risen across the curve by up to 70 basis points in the past three months. That must come with a substantial economic cost as financial conditions ratchet tighter. The Fed’s work is being done for it.

The result is monetary policy that is probably too tight. Keeping interest rates unchanged further restricts financial conditions as lagged monetary tightening has yet to fully pass through the system. Powell is keeping a calm head by repeating the expectation of lower Fed Funds this year. A flexible inflation regime could bring a wider calm to monetary policy — as opposed to frenetic market gyrations with every drop of new data.

The Bank of Japan is ahead of the game. It signaled this week that less emphasis will be placed on ensuring its medium-term inflation outlook has to be 2%. Higher levels alone won't indicate a near-term hike. Having suffered three decades of persistent deflation, it knows that is far harder to control, let alone eradicate, than relatively brief bouts of inflation.

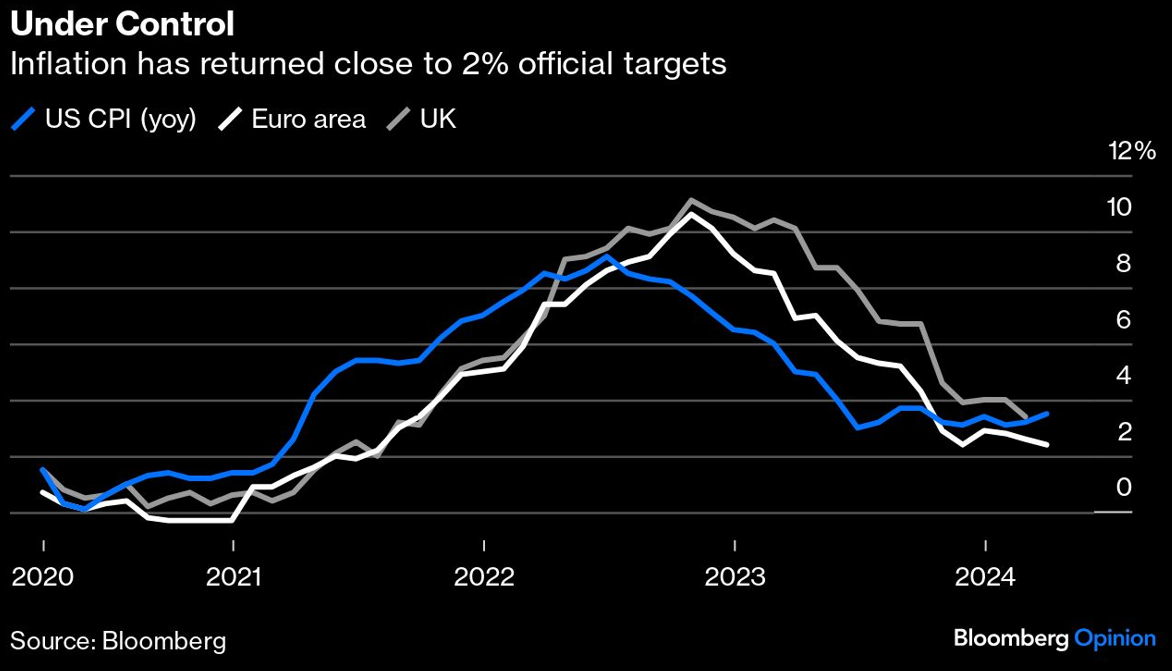

The Bank of England would be wise to pay attention, especially as the UK economy is coming out of a technical recession. Its former chief economist, Andy Haldane, recommended a more tolerant approach last summer. Time to clear out redundant practices. It’s opportune that Wednesday’s UK March CPI fell to 3.2%, with next month's expected to be close to 2%. Capital Economics estimates it could fall below 1% by the summer. Disinflation could turn into deflation.

It helps, too, that the European Central Bank is increasingly confident over its inflation forecast. Change is best enacted in a stable environment. French central bank head Francois Villeroy de Galhau in an interview in the French press last weekend said he’s more confident about the downward trajectory of euro-area inflation.

ECB President Christine Lagarde at least admitted last year the internal failure of its inflation forecasting. As Powell said in September: “Forecasting is very difficult. Forecasters are a humble lot — with much to be humble about.” The solution is in front of central banks — stop obsessing about every notch of inflation and take the broader view a range affords. The 2% target has passed its use-by date.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our podcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Marcus Ashworth