When the Federal Reserve flooded the economy with cash during the Covid-19 pandemic it exacerbated a problem for America’s largest banks: What to do with all the extra deposits.

Now that interest rates are set to fall four years later, the payoffs from the differing approaches at JPMorgan Chase & Co. and Bank of America Corp. are abundantly clear: The former’s choice to keep spare cash in money markets or at the Fed turned out to be the much more lucrative strategy than investing in bonds.

The lesson is to keep your options open in the face of great uncertainty, although it would be wrong to criticize Bank of America too harshly: There has been little opportunity to lend into the economy instead and Bank of America’s choices about what to do with all that money were similar to the rest of the sector. JPMorgan stands out more from the crowd. Today, the good news for the economy is that both still have abundant resources to meet demand for credit when it returns.

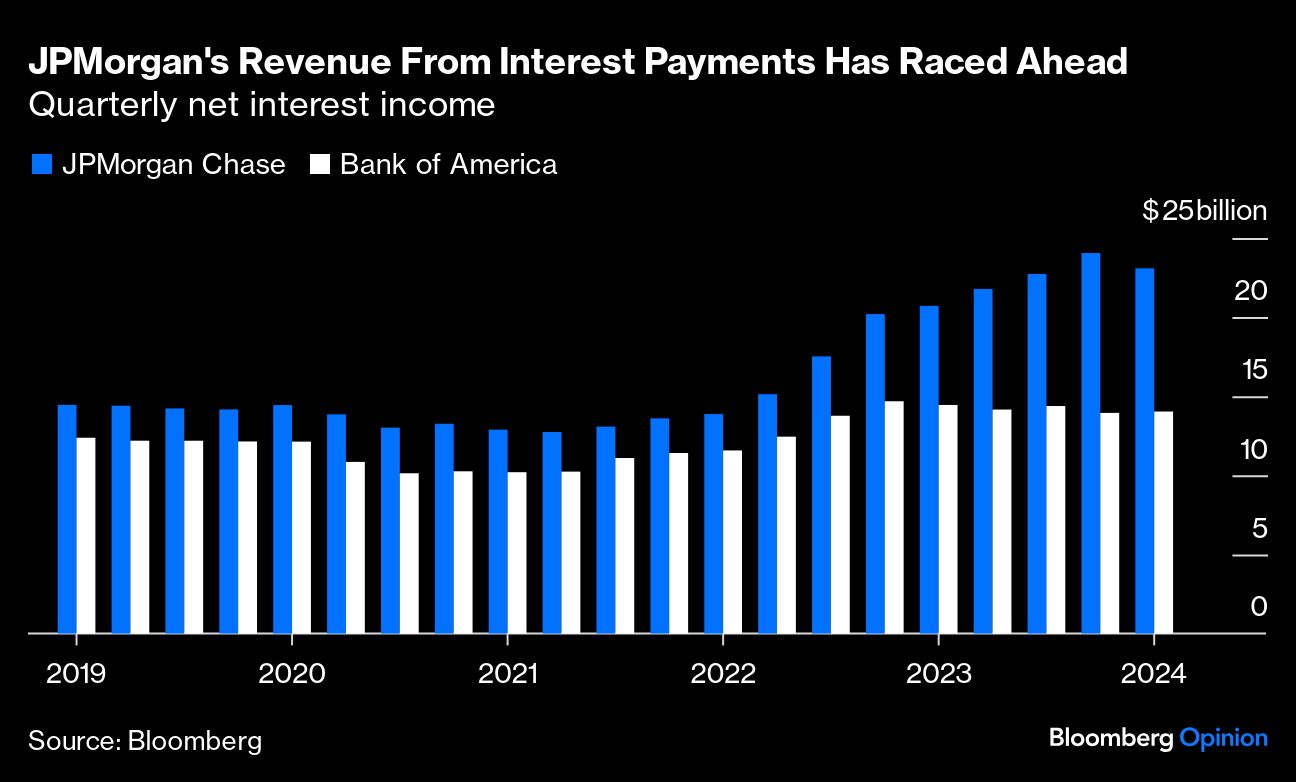

To see what happened, look at net interest income, which is the revenue banks earn from loans, money markets and bonds after paying depositors and other interest costs. JPMorgan’s NII in the first quarter of this year was 60% higher than the quarterly revenue it earned before the pandemic. Bank of America’s NII was just 12% higher.

That gap is much greater than the difference in the deposit growth at each bank: Bank of America still had 41% more deposits at the end of the first quarter this year than at the start of 2019, while JPMorgan had 65% more. It did get some extra deposits and loans from its rescue of First Republic last year, but neither is enough to account for JPMorgan’s extra income.

It’s worth stopping for a moment to take in the scale of these banks after the pandemic and the regional bank crisis last year. JPMorgan’s total deposits stood at $2.4 trillion at the end of March and Bank of America’s were $1.95 trillion. Together, that’s equivalent to one-quarter of all deposits in the US.

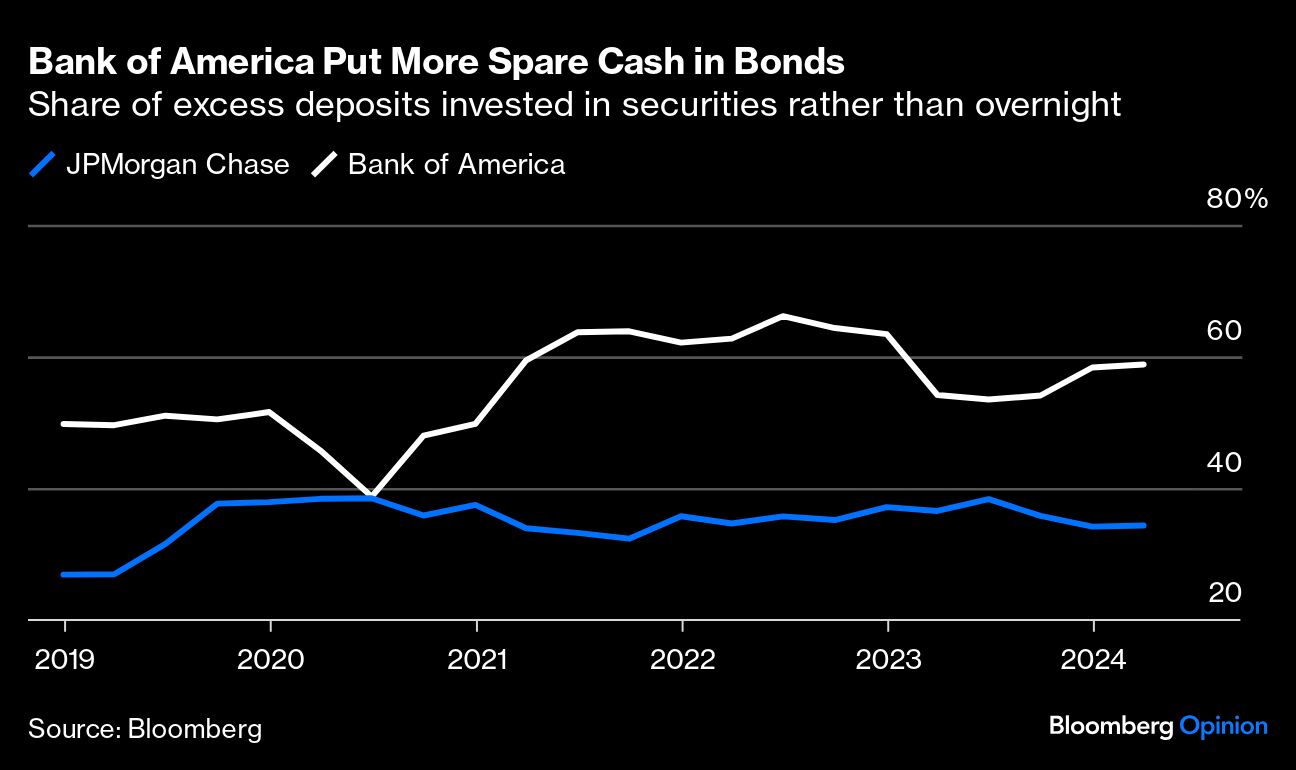

During 2020 and 2021, government cash was flooding into people’s and companies’ bank accounts while they were stuck at home spending less and often paying off some debt. In this period, all banks bought more Treasuries and agency bonds, but in the second half of 2020 Bank of America started to tilt its excess funds toward securities and away from cash, whereas JPMorgan leaned toward cash and stayed there. At their point of greatest difference in late 2021, the former had nearly two-third of its excess deposits in securities and the latter less than one-third.

At first, Bank of America looked smart: The Fed didn’t start raising rates until March 2022 and the effective Fed Funds rate in markets didn’t overtake Treasury yields until November. But as more hikes came through, the yield JPMorgan was getting on its cash helped its net interest income begin to accelerate away from its rival’s.

For Bank of America there were other issues, too. As bond yields climbed higher, their value tumbled, which led to capital hits for all banks. But for Bank of America this bought bigger questions about the size of unrealized losses from bonds that it planned to hold to maturity, especially after the collapse of Silicon Valley Bank last year. In late 2023, Bank of America was carrying $131 billion of unrealized bond losses to JPMorgan’s $34 billion. The chances of Bank of America ever having to book those losses were incredibly slim given its vast cash reserves available for any deposit withdrawals. Still, there were some awkward headlines, and analysts were still asking last week whether changing bond values in its available-for-sale book could hurt its capital base in the future.

I asked Alastair Borthwick, Bank of America’s chief financial officer, whether he now second-guessed decisions to move more cash into bonds. “If we had known absolutely two-to-three years ago everything that was going to happen, could we have done a better job? Of course,” he said. “But we’re very comfortable with where we are.”

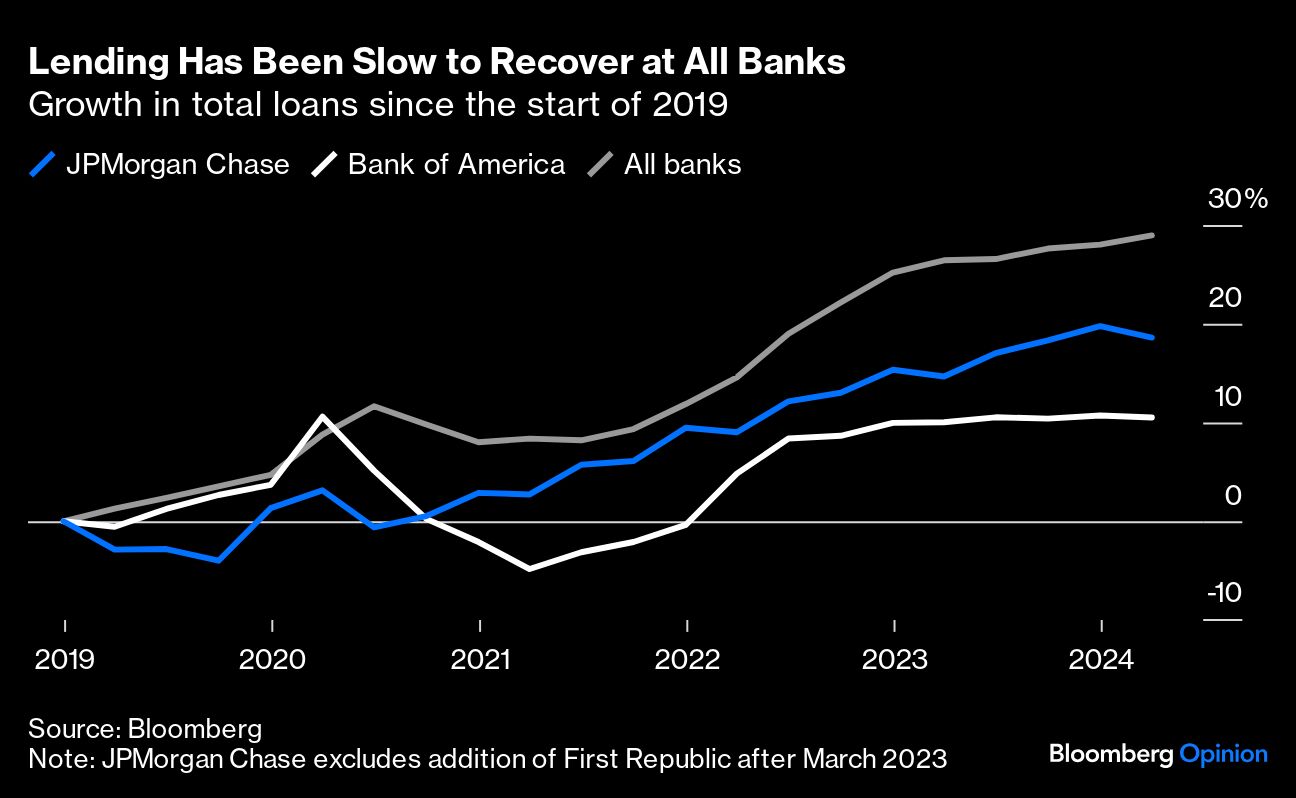

The question for the wider economy is how this affects either banks’ ability or appetite to lend. In short, it shouldn’t, and the banks themselves insist they would loan more if demand were there. Across all banks, commercial and industrial loans were about 20% higher at the end of March than they were at the start of 2019, while consumer loans were up 28%. JPMorgan’s total loans have grown nearly 20% over the same period (excluding First Republic, which added 14 percentage points of growth). Bank of America’s loan growth lags the sector at 11% to the end of March.

JPMorgan has been helped by running the US’s biggest credit-card business, which has seen borrowing recover much more strongly than other types of lending. But on first-quarter earnings calls, both banks said demand for corporate loans in particular remained muted.

That is likely to change this year as all the spare cash that consumers and companies had from the pandemic is finally running out. Once the cost of borrowing starts to fall again, too, demand for credit should pick up. Banks should have no trouble meeting it: For JPMorgan and Bank of America, loans accounted for less than 55% of deposits at the end of the first quarter, much lower than the almost 70% at the start of 2019. Their combined cash and bond holdings, meanwhile, added up to a staggering $3.2 trillion. That can’t all go to lending, but plenty could.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our videos.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.