Plot Twist

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsThe U.S economy seemed headed for a fairy-tale ending in late 2023. Inflation was cooling and economic growth had begun to moderate after a series of interest rate hikes by the Federal Reserve.

But the narrative has taken a turn in 2024. The economy and labor market have maintained a heady pace. Measures of inflation have either stalled or are showing signs of reflation, leading to a significant repricing of expected rate cuts by the Fed.

As the last mile of the inflation recovery proves to be the hardest, the higher-for-longer outlook has taken hold. Sticky inflation has delayed but not derailed rate cuts. While the soft landing is still our base case, it may take longer than expected to materialize.

Following are our thoughts on recent data and developments.

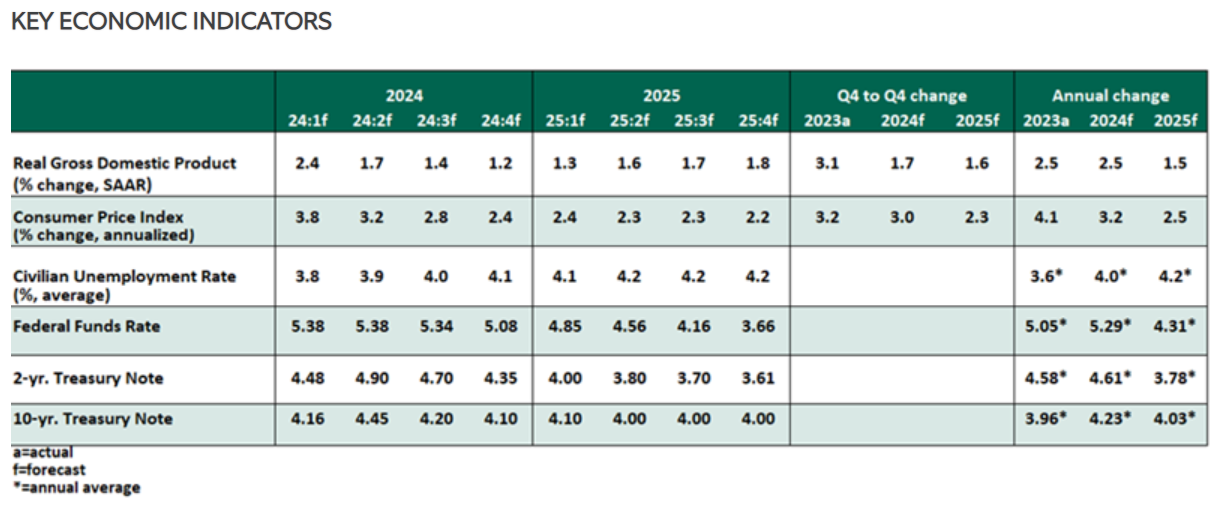

Influences on the Forecast

- Progress against inflation has halted. Readings on consumer prices have risen by 0.4% for three months in a row, pushing the year over year rate up three-tenths to 3.5%. Though gas and shelter costs contributed more than half of the monthly increase, price gains were broad-based. Core services excluding housing continued moving upward.

While seasonal and one-off adjustments likely led to the firmer readings at start of the year, March’s upside surprise has raised concerns that a new trend is starting. We don’t agree, but incremental progress has been disappointingly slow.

- The labor market has shown no signs of a let-down. Nonfarm payrolls again beat expectations, increasing 303,000 in March, the biggest rise in nearly a year. The unemployment rate fell one-tenth to 3.8%. The surge in immigration explains the extranormal increases in job gains. Immigrants are contributing to increased labor supply, addressing a short of workers in sectors like hospitality and healthcare. Many newcomers typically fill lower-paying jobs, keeping wages gains tame. This explains why despite strong job gains, the annual increase in average hourly earnings continued to decelerate to 4.1%. Though moderating, wage gains are still too high to be consistent with the 2% inflation target.

Job openings remained elevated, while the rates of hires and quits settled into ranges consistent with pre-pandemic turnover. The layoff rate increased slightly, but remains below pre-pandemic levels.

- At the March Federal Open Market Committee (FOMC) meeting, the Fed left its target rate range unchanged. An updated Summary of Economic Projections reaffirmed that the median Committee member expected to make three rate cuts in 2024. But persistently high inflation readings appear to have sent officials back to an uneasy holding pattern. Recent comments from Fed officials have shown varying degrees of concern that the job of bringing inflation down is not yet done.

With the economic backdrop still solid and inflation stickier, we have pushed the timing of the first rate cut from June to September. The Fed will need to see a clear slowing of inflation momentum before it starts easing rates. We also expect the FOMC to announce slower pace of quantitative tightening in May with execution to follow in June.

- The U.S. economy shows no signs of significant cooling. Retail sales, which represent about one-third of all household spending, rose in March for the second consecutive month. Sales were up across several categories, underscoring the strength of the consumer. Real gross domestic product (GDP) growth for the first quarter is tracking at a pace of close to 3%, well ahead of expectations.

Steady consumption is one more reason why completing the last mile of inflation progress may take longer than expected.

- The higher-for-longer outlook for interest rates has pushed Treasury yields upward and added strength to the dollar. While these developments will take the edge off demand and inflation, it also has risk of spillover for the housing market. Mortgage rates have been drifting higher, amid a market constrained by fewer homes for sale and rising prices. The spike in rates is also making builders more cautious, reflected in the notable decline in both housing starts and building permits in March.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2024 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All