Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

The Federal Reserve is expected to lower interest rates, but the economy and stock market don't need stimulation. Treasury Bills yield 2.5% more than their historical average, while long-term bonds earn 0.5% less. Inflationary pressures from COVID spending could lead to an increase in long-term government bond yields and a debt spiral.

Everyone expects the Federal Reserve to “pivot” – to lower interest rates – primarily because inflation appears to be under control. But the economy and stock market are flourishing, so they don’t need stimulation.

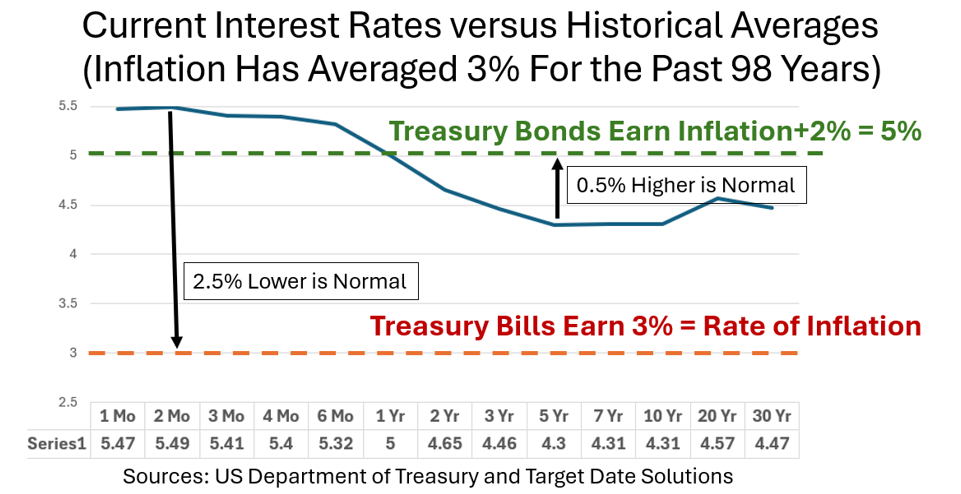

The real question: Where should interest rates be? History can be our guide. Over the 98 years from 1926-2023, inflation has averaged 3%, so about the current level. Treasury Bills have yielded the rate of inflation and Treasury bonds have returned 2% above inflation, about 5%.

As shown in the following, Treasury Bills currently yield 2.5% more than their historical average, so it’s reasonable to expect them to decline if inflation remains at 3%. But long-term government bonds are earning 0.5% less than the historical average, so they can be expected to increase, and to increase more than 0.5% if inflation increases.

Why the departures from averages?

The Federal Reserve controls the short end of the yield curve. It sets short-term interest rates. These rates are high by historical standards because the Fed is fighting inflation, so it wants to slow down the economy. Lowering interest rates would stimulate the economy and stock market, risking higher inflation.

Investors set long-term interest rates, and they expect interest rates to decline. They’ve priced in lower yields that create an inverted yield curve (that is not normal). Investors normally demand higher yield for taking on the risk in long-term bonds. Inversions don’t last long and usually precede a recession. It makes no sense for investors to buy riskier bonds that pay less.

If inflation increases

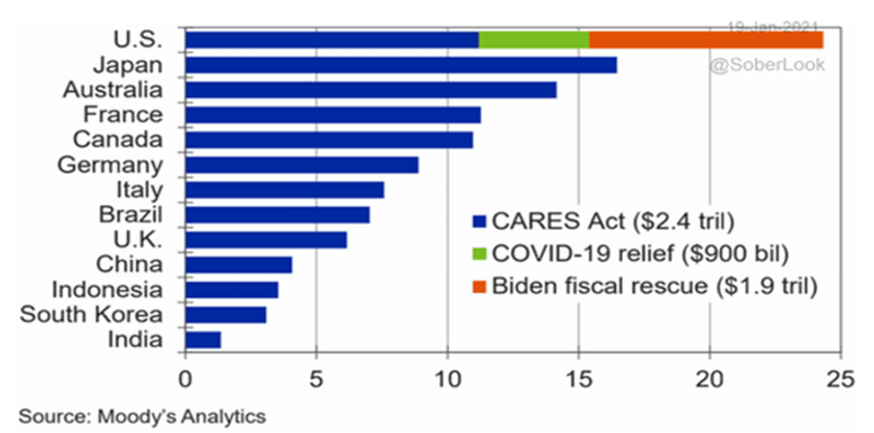

With $5 trillion in COVID spending working its way through the economy, it will create inflationary pressures.

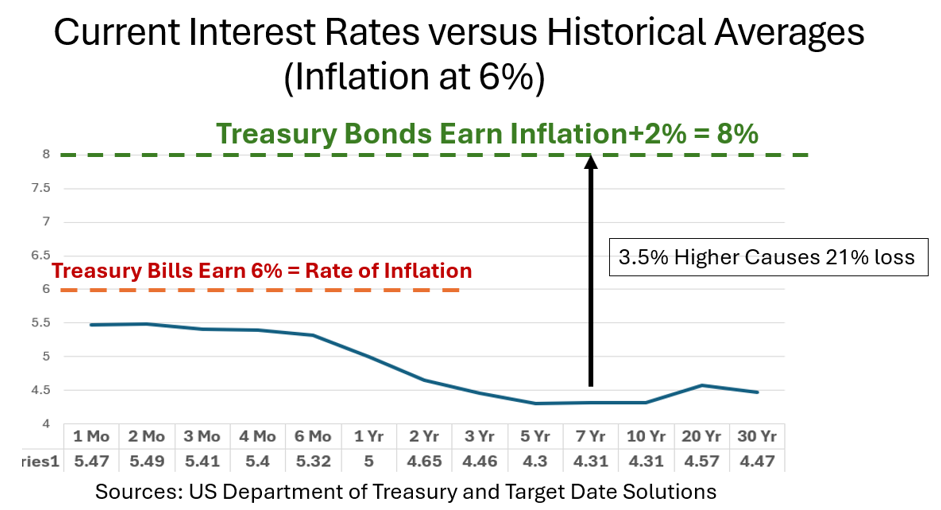

For sake of discussion, let’s say inflation increases to 6%. It was at 9% not too long ago in July of 2022. If that happens, long-term government bond yields will increase to 8% (2% above inflation). This 3.5% increase will generate a 21% decline in bond prices. And there would be little change in short-to-intermediate-term Treasury Bill yields; short-term interest rates are poised for 6% inflation.

The increase in long-term yields would be necessary to attract investors. As I explained in America's biggest bond buyers aren't buying bonds, China and the Federal Reserve – the two largest buyers – are not buying, so “Without these two seemingly bottomless sources of demand for American bonds, Uncle Sam has to offer higher yields than it otherwise would have, to get the money it needs from investors.” The Treasury issues bonds to finance the deficit.

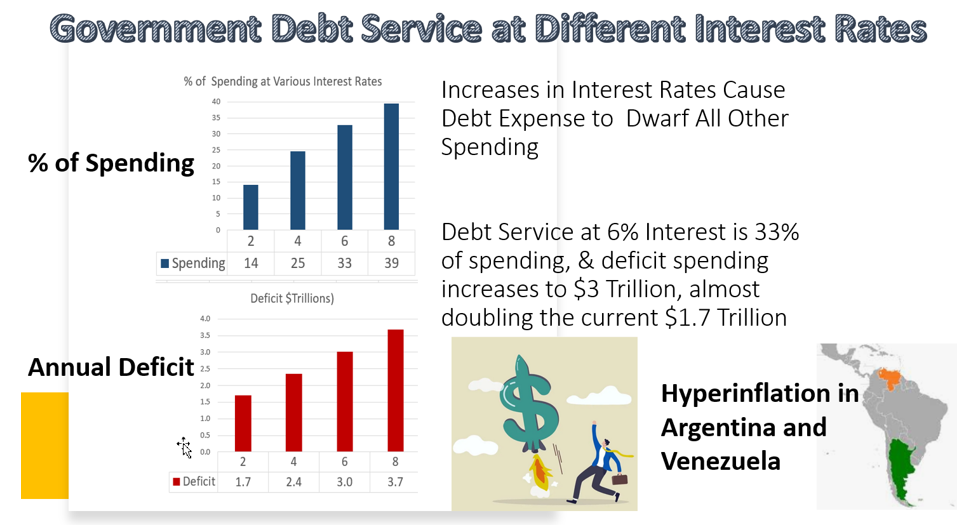

A debt spiral

Interest on our $34 trillion debt is $870 billion, which is 2.6% of the debt because the Fed has engineered a zero-interest rate policy (ZIRP). Approximately $616 billion of the $870 billion is paid out of $4.4 trillion in tax revenues and the remaining $254 billion is added to the deficit, which is running around $2 trillion in total.

If inflation increases, debt service crowds out other spending, like Social Security, and increases the deficit, as shown in the following:

Conclusion

We all hope inflation is under control. If it is, short term rates will come down to approximate inflation. But long-term rates are currently below their historical average of 2% above inflation, so they will trend upwards.

If inflation increases, long-term bond yields will increase significantly, and a debt spiral will ensue. Preparing for this possibility is discussed in my article, “When Stocks and Bonds Won’t Do.”

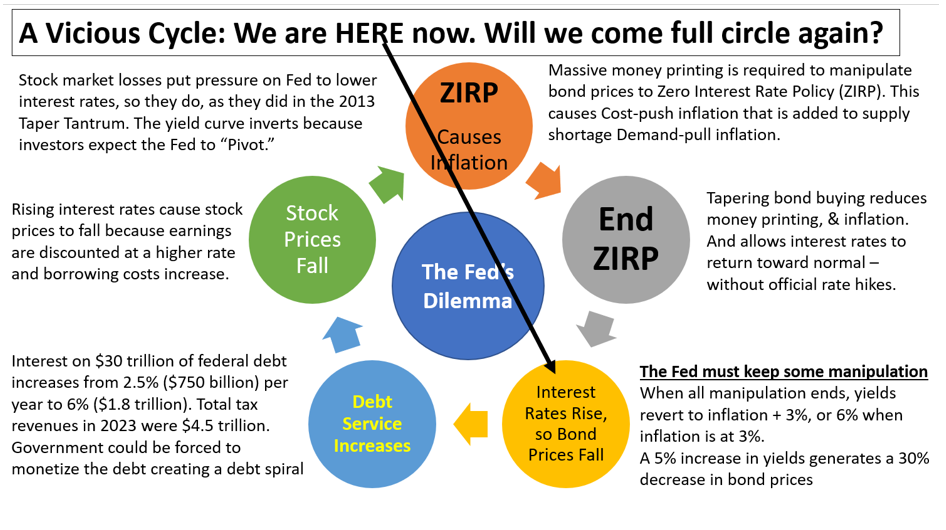

The Fed is trapped in a cycle. How do you think it will escape?

Ron Surz is president of Target Date Solutions, developer of the patented Safe Landing Glide Path and Soteria personalized target date accounts. He is also co-host of the Baby Boomer Investing Show. His passion is helping his fellow baby boomers at this critical time in their lives when they are relying on their lifetime savings to support a retirement with dignity, so he wrote a book, Baby Boomer Investing in the Perilous 2020s, and he provides a financial educational curriculum.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our podcasts.

Read more articles by Ron Surz

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.