Drew O’Neil discusses fixed income market conditions and offers insight for bond investors.

Fed Funds Rate According to Bloomberg calculations based on where Fed Funds futures are currently trading, there is a 20% chance that the FOMC cuts the overnight rate in June and a ~50% chance that they cut in July. Looking ahead to year-end, these calculations are pricing in 25-50 basis points of total cuts by the end of 2024 with one 25 basis point cut in September or November and roughly a 50% chance of a second 25 basis point cut in December. On January 1st of this year, markets were pricing in between 125 and 150 basis points of total cuts in 2024.

Inverted Curve The Treasury curve is approaching two years of being inverted (short-term yields higher than long-term yields). The 10-year/2-year spread has been negative (inverted) since July 5, 2022 and is currently at -37 basis points. An inverted Treasury curve has historically been a predictor of a coming recession although the timing of when recessions have started with relation to the yield curve inverting has varied.

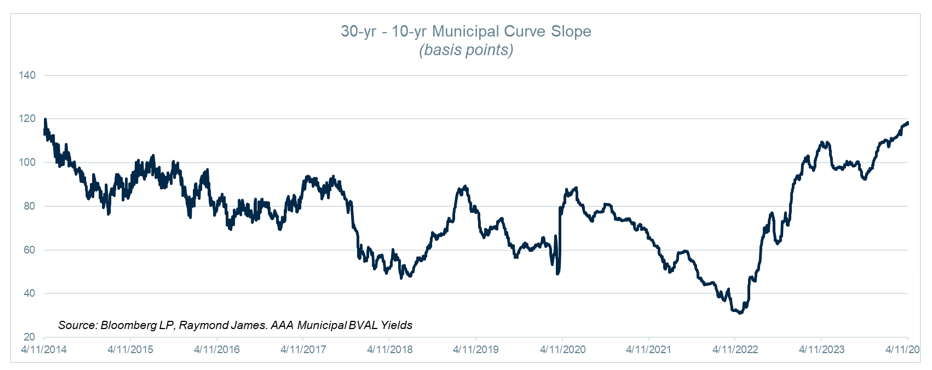

Long Municipals Municipal bonds on the longer part of the curve offer attractive yields relative to intermediate maturity bonds. The yield pickup of a 30-year maturity over a 10-year maturity is currently 118 basis points. The higher this spread is, the more investors are “rewarded” with more yield by extending out into longer maturity bonds. Out of the ~2,500 trading days over the past 10 years, the 30-year/10-year yield pickup has only been higher on 4 days (from 4/11/14 to 4/11/24). Taxable equivalent yields on the long end of the curve for high tax bracket investors can reach into the 6 to 7% range, an attractive proposition for A to AAA rated municipal bonds.

Yields Yields across the fixed income landscape remain at some of their highest levels of the past ~15 years. The 10-year Treasury is currently ~4.59% which is over 200 basis points higher than its average since 2010 of 2.41%. Year-to-date, the 2-year, 10-year, and 30-year Treasuries are all higher by over 60 basis points. Despite spread tightening, the increase in benchmark yields has pushed corporate yields higher as they continue to offer some of the best income opportunities in ~17 years.

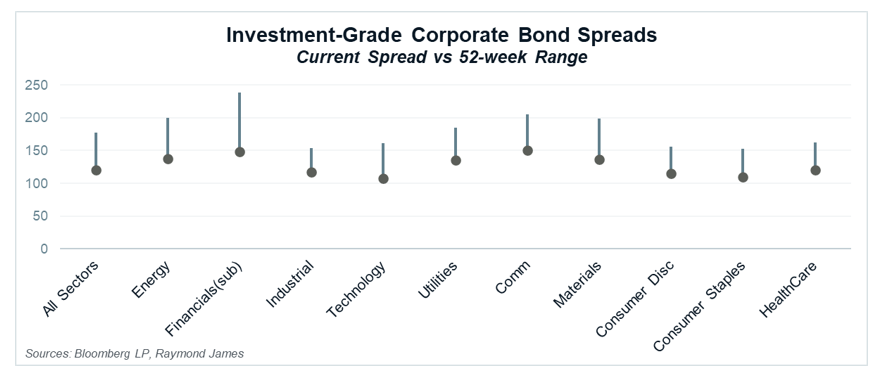

Corporate Spreads Demand for high-quality corporate bonds has pushed spreads tighter. Fund flows into taxable funds and ETFs have been positive every week of the year so far, with an average of $10.8 billion of inflows per week. Spreads for investment-grade corporates are near their tightest levels of the past year across all sectors. Investment-grade spreads overall are at ~120 basis points with a 52 week range of 116 to 175.