As harrowing as it has been to watch bond yields jump, watching them sit still would’ve been worse for stock investors banking on a major revival in earnings this year.

Economic growth is picking up and the stock market is trending higher, but in a choppy fashion that lately resembles a “bunny” market more than a bull market.

It is commonly assumed that growth stocks are bigger beneficiaries of falling interest rates than value stocks, an assumption driven by a belief that growth stocks are much longer “duration” than value stocks due to the fact that more value in growth companies comes from relatively more distant cash flows.

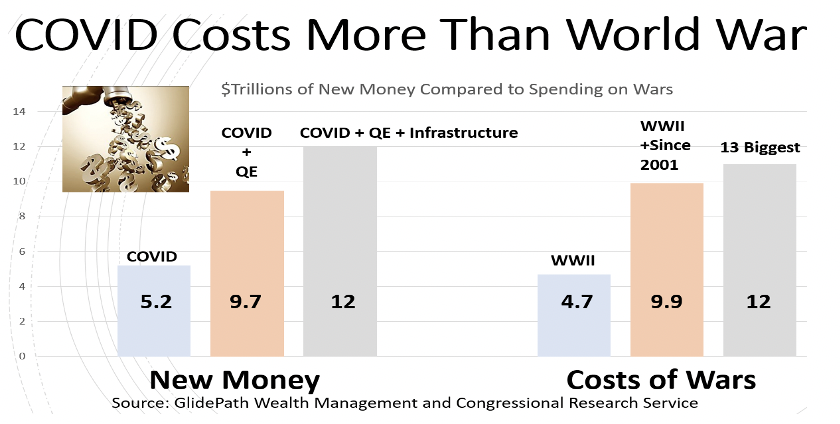

The government’s COVID relief programs have cost $5.2 trillion, more than World War II, which cost $4.7 trillion. Those mountains of money will cause inflation, raise interest rates and reduce in stock prices.

Global stocks and bonds are both expensive. U.S. stocks are trading at particularly elevated valuations with the CAPE ratio standing at 35x (vs. a 10-year average of less than 27x) while the Barclays Bloomberg U.S. Aggregate index offered a negative real yield at the end of February.

The Federal Reserve on 19 March announced that the temporary changes to its supplemental leverage ratio, or SLR, will expire as scheduled on 31 March.

Failure to boost vaccination programs could hurt the eurozone economy.

Stripped down to basics, the new consensus in economics goes like this: It’s fine for governments to borrow and spend more money -- so long as they can get hold of it cheaply.

The last few weeks have seen increased volatility in the equity markets as rates have begun to creep back up surrounding inflation fears and investors temporarily pulling out of big tech names that have driven the S&P’s performance for the past few years.

Real rates in the United States have moved sharply higher since the beginning of 2021.

Since the “Financial Crisis,” the hope was that inflating asset prices would trickle down into economic growth.

We are going to look at broken debt and broken measurements, and then look at how Fed leaders painted themselves into a corner by shifting to a reactive stance this week.

Wall Street thought 2020 was the Year of the SPAC, or special purpose acquisition company (SPAC). Turns out, this title was premature.

Taxable Municipal Bonds grabbed the attention of not only municipal bond market participants in 2020, but also of investors and financial professionals globally across the asset class landscape.

The stock market as measured by the S&P 500 is at an all-time high.

Last year featured a jaw-dropping list of extremes, from a once-in-a-century pandemic to record-breaking market moves. Howard Marks writes in his latest memo about approaching the investment environment left in 2020’s wake – one generating many questions and no easy answers.

The 60/40 portfolio saw investors through the cataclysm of the pandemic. The global recovery is now proving an even tougher test.

We expect the recent passage of the $1.9 trillion American Rescue Plan to be an extremely positive impulse for municipal credit stabilization and underlying fundamental improvement more broadly.

Is it possible to travel in two directions at the same time? Imagine walking to the restroom at the back of an airplane while in mid-flight.

The word “bubble” is tossed around quite a bit in the financial markets, but it’s rarely used correctly.

The recent rise in interest rates triggered a bout of volatility, but it’s not making the pros in the stock market run for the hills just yet.

This probably isn’t the start of a bear market, but it may feel like less a bull market compared with last year’s charge.

Chief Economist Scott Brown discusses the latest market data.

Will the Fed respond to inflation concerns?

Relying on only historical U.S. returns creates an unrealistic picture of retirement outcomes. Our analysis shows that U.S. data are an anomaly among the broader global universe, and that our low-yield environment forebodes lower-than-average equity returns.

In this article, I dissect Operation Twist. I also look back at Operation Twist 2.0 circa 2011- 2012 and assess its effectiveness and how it impacted various asset classes.

U.S. economic growth is accelerating as vaccinations rise and social-distancing measures ease, but hopes for a long-lasting spending boom may hit a couple of speed bumps. Vaccine rollouts in major countries are proceeding at different speeds, but stock market performance contradicts what vaccination data would seem to imply for investors. Meanwhile, inflation-adjusted longer-term Treasury yields have risen as investors anticipate stronger economic growth.

A little over a hundred years ago, the United States emerged from the double whammy of a world war and deadly pandemic. Eager to get back to “normal” life, Americans went on a decade-long spending splurge, buying cars and radios and stocks.

I believe we have passed the point of no return. Changing policy now would create a recession as big as Paul Volcker’s in the early ‘80s. There is simply no appetite for that. Further, the national debt and continued yearly deficits force monetary policy to stay accommodative.

Republicans are invoking the threat of inflation to attack President Joe Biden’s spending plans, after he won approval for $1.9 trillion in virus relief ahead of a broader recovery package that may cost even more.

Don’t fear Treasury yields killing off the stock market’s golden goose just yet.

It’s been a long time since investors have had to worry about inflation.

There is significant variation in how countries have handled the pandemic, managed fiscal and monetary policy, and supported their economies, according to Templeton Global Macro.

Even as credit spreads have narrowed, further value remains.

Global risk assets rose in the wake of positive developments on the two main fronts that have dominated headlines over the past 12 months – pandemic and stimulus.

Over the past month, the expectations of growth in the year ahead have surged, with fixed income markets repricing and investors shifting allocations in anticipation of growth.

A key measure of U.S. consumer prices rose less than expected in February as costs of used vehicles, clothing and transportation services declined from a month earlier, suggesting broader inflationary pressures remain tame.

Russ discusses why gold has not been an effective hedge recently.

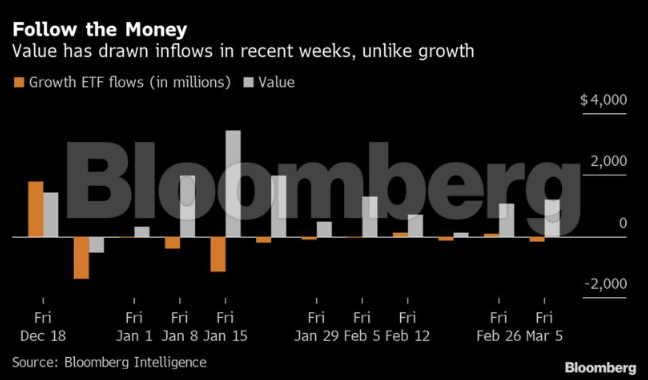

The left-for-dead value trade has roared back to life to wipe out all its pandemic losses, with its revival reshaping the $2 trillion world of factor investing.

In an online discussion, Fed Chair Powell repeated that the central bank is a long way from achieving its inflation and employment goals (implying no change in short-term rates or the money pace of asset purchases anytime soon).

As the latest COVID-19 relief bill winds through the U.S. Congress, some economists have been warning that too much stimulus could lead to the economy overheating

Headline CPI inflation is almost certain to rise above 3% in June and July, according to Jeffrey Gundlach. It could even top 4%, he said, which would “really spook the bond market.”

“Bull markets are born on pessimism, grow on skepticism, mature on optimism and die on euphoria.” -Investor and mutual fund manager Sir John Templeton

A rapid souring in financial markets on Monday highlights how even the most positive news for the world economy is no fillip to risk assets weighed down by the anchor of the global bond market.

Concern is mounting in corporate credit markets globally as longer-term Treasury yields continue to rise, leading borrowers from New York to Tokyo to delay bond sales and strategists to warn of trouble ahead.

Longer-dated Treasury yields have climbed as markets consider whether economic growth and inflation expectations might accelerate more rapidly. We believe inflation pressures will remain in check and bond yields will be range-bound.

Rising yields and a steeper yield curve are par for the course as an economy enters the recovery phase of the global credit cycle.

Treasury yields rocketed higher in February, with the move again concentrated in longer maturities. Volatility spiked as liquidity dried up in the Treasury market, especially after a very weak 7-year auction that briefly pushed 10-year Treasury yields to 1.60%. The news flow was largely the same direction: an improving economy, increased vaccine rollout with deaths and hospitalizations turning sharply lower, and a continued march toward a substantial fiscal stimulus plan.

How does risk management work when risks change rapidly?

There may be some incredible opportunities for investors in companies that produce the metals, minerals and other raw materials that will be needed with an increase in spending.