The False Promise of U.S. Historical Returns

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits

Relying on only historical U.S. returns creates an unrealistic picture of retirement outcomes. Our analysis shows that U.S. data are an anomaly among the broader global universe, and that our low-yield environment forebodes lower-than-average equity returns.

Relying on only historical U.S. returns creates an unrealistic picture of retirement outcomes. Our analysis shows that U.S. data are an anomaly among the broader global universe, and that our low-yield environment forebodes lower-than-average equity returns.

Before we get into the details of those conclusions, let’s review why bond and stock return forecasts are so critical to the Monte Carlo methodology that is the basis for analyzing retirement plans.

A Monte Carlo Analysis is a statistical procedure that simulates a sequence of possible future investment returns. It is common to run a Monte Carlo analysis on hundreds or thousands of simulated retirements to estimate the impact of portfolio spending rates on the probability of running out of money. The projection typically assumes the withdrawal of a fixed amount each year from an investment portfolio that increases or falls by a random rate of return. It is common to base the distribution on historical U.S. returns on stocks and bonds.

If the return distributions of stocks and bonds resemble a bell curve, then most simulated returns will be close to their respective average. The estimated safety of a fixed-withdrawal strategy will not be accurate if the average assumed return in the Monte Carlo analysis is higher than the average return an investor is likely to experience. If the mean is a few percentage points lower than the historical average, these estimates can be very far off.

Real bond returns are likely to be significantly lower than their historical average over the next decade. Returns on risk-free bonds are a component of forecasted stock returns according to the capital asset pricing model (CAPM), meaning that lower bond returns should affect expected stock returns. Even if portfolio returns revert back to their historical average in subsequent decades, shifting the equity return distribution to the left at the beginning of retirement will have an outsize impact on outcomes.

While use of U.S. historical long-term averages may seem reasonable, those historical returns fail two important tests: They are not representative of global historical returns and they don’t reflect the current environment. Therefore, using historical U.S. returns is likely to result in unrealistic savings or spending goals.

Monte Carlo analyses should use a comprehensive global time series. Advisors should base projected safe-spending rates today using simulations that account for a lower return than U.S. investors were fortunate enough to experience in the 20th century.

Representative bias

Early research on safe-initial withdrawal rates (SWRs) predominately relied on the Ibbotson stocks, bonds, bills, and inflation (SBBI) dataset, which includes various U.S. asset classes going back to 1926. The seminal analysis by Bengen (1994), which introduced the “4% rule,” used this data.

Today many advisors use the SBBI historical time series when estimating required savings or optimal spending levels for clients. A longer time series of U.S. returns is now widely available. For example, Shiller has a dataset that goes back to 1870 on his website.

Tomorrow’s investors may experience the same returns that U.S. investors received historically, global asset return data provide an even larger sample size that can be used to create a more reliable distribution of expected future returns.

A decade ago, Wade Pfau demonstrated that international safe-withdrawal rates were often far lower than what American investors experienced in the 20th century using the Dimson, Marsh, and Staunton (DMS) dataset, which includes annual historical data for 21 countries going back to 1900. Another relatively new dataset, the Jordà-Schularick-Taylor Macrohistory (JST) database, has recently been made available for free online, and it includes data on 17 countries going back to 1870.

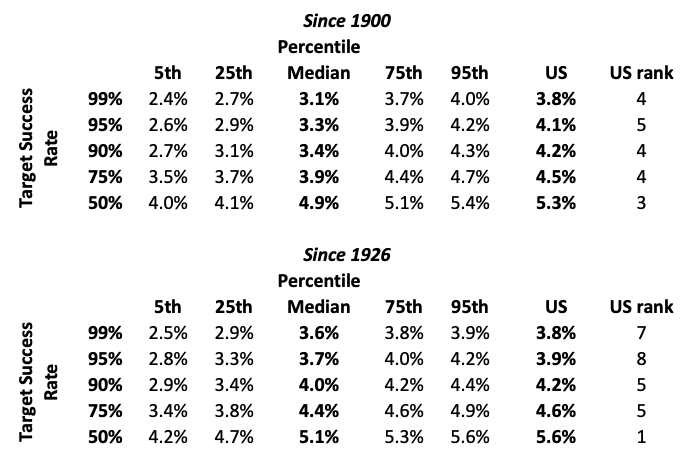

To demonstrate how using different country returns over different time periods can impact a financial projection, we performed an analysis using the DMS dataset (obtained from Morningstar Direct). The analysis estimates the SWR for a 50% stock/50% bond portfolio with 50 basis annual fees assuming a 30-year retirement period where withdrawals are adjusted for inflation (i.e., the analysis is in real terms).

Safe-initial withdrawal rates are estimated for each country, either starting in 1900 when the DMS dataset begins, or 1926, when the SBBI dataset begins. The distribution of SWRs across various target probabilities of success are included below, along with the results of the U.S. for comparison purposes.

SWR Distribution for a 50/50 Portfolio Using International Historical Returns

Source: Dimson, Marsh, and Staunton dataset, Author’s Calculations

There are a few important takeaways from the analysis. First, SWRs in the U.S. have been considerably higher than other countries. For example, targeting a 90% success rate, the U.S. historical SWR would be 4.2% since 1900 versus the 21-country median of 3.4%. The U.S. ranks approximately fourth (out of 21 countries) since 1900 and fifth since 1926. U.S. investors’ experience has been in the top quartile of all countries.

This outperformance may persist, but the U.S. experience has been better than average. If investors in each country ran retirement projections using their historical returns, their results would be very different. The asset-return correlations among countries have increased significantly over time, and the differences in international returns observed in the historical data are unlikely to continue. As investors across the globe hold internationally diversified portfolios, U.S. market returns will increasingly resemble those in other countries.

The investing reality

Bond yields are significantly lower today than their historical averages. We (along with Wade Pfau) previously estimated the surprising sensitivity of Monte Carlo failure rates to bond-return assumptions.

The CAPM estimates expected returns on risky assets as a function of the risk-free rate and the risk premium. Rates of return on safe bonds are known and will affect the return on stocks. While valuation metrics such as the CAPE ratio do not consider the impact of today’s bond yields, accounting for today’s yields provides a more accurate forecast of future stock returns.

Lower fixed-income yields mean the returns on bonds are going to be lower (the asset is called “fixed” income for a reason). While bond yields could increase, which would increase the yield on bonds, the increased income would be offset by the decrease in price. Therefore, any increase in future interest rates will have a negligible impact on realized bond returns.

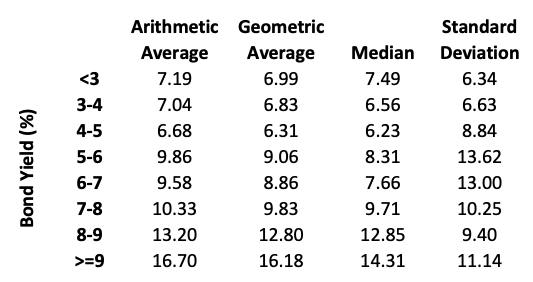

Bond yields have also had a surprising relation to stock returns. To provide some context, we performed an analysis using primarily the JST dataset (although we supplemented it with other sources in a few instances) from 1870 to 2019. The JST dataset includes government bond yields and stock market returns for 17 countries. For the analysis, the future five-year return on equities is estimated where all countries are grouped based on levels of prevailing bond yields, in roughly 1% increments. In other words, all countries where bonds yielded less than 3% at the end of the previous year would be placed in “<3%” bin and the future five-year equity returns were estimated for the entire group.

The results are the average of the five starting points to estimate future five-year returns (i.e., they are based on non-overlapping periods). The average of the five periods were used to avoid potential selection bias with any one starting period.

Bond Yields and Future 5-Year Equity Returns

Source: Jordà-Schularick-Taylor Macrohistory Database; Dimson, Marsh and Staunton dataset; OECD; MSCI; Morningstar, Authors’ calculations

There is a positive correlation between initial bond yields and the subsequent five-year returns on stocks. A regression predicting future stock return using initial bond yield has a slope of approximately 1. In other words, a 1% in reduction in bonds yields has corresponded to a 1% reduction in equity returns. Bond yields are approximately 350 bps below their long-term average. This suggests return expectations for equities should be approximately 350 bps less than their long-term average. The standard deviation of returns has also been lower during periods of low bond yields.

Using historical global returns to estimate withdrawal rates

Using a larger sample of global return data (i.e., more than just U.S. historical averages), it is evident that subsequent stock returns have declined when initial bond yields have been lower, consistent with the CAPM. This means investor expectations should be lower today to incorporate the lower bond yield environment. Although any single year’s return is subject random variation, the distribution of the expected return should be reduced.

Next, we leveraged the JST dataset to combine the previous two analyses, where we estimated SWRs based on the initial bond yield environment. Like the initial analysis using DMS data, we assumed a 50/50 portfolio where retirement lasts 30 years and withdrawals are increased annually for inflation. Like the return analysis, we grouped the respective outcomes based on the initial withdrawal rate at the beginning of the 30-year period. Within each bond-yield group, we estimated the initial withdrawal rate that would result in various target probabilities of success (e.g., for an initial bond yield of less than 3%, a SWR of 3.4% has a 50% chance of success). The results are included below.

SWR Based on Initial Bond Yield and Success Target

If we use historical periods that resemble today’s low-yield environment to estimate the range of potential withdrawal rates (less than 3%, which is the first row and is well above where rates are today), we see that even targeting a 50% success rate results in an initial withdrawal rate of 3.4%. If you’re targeting a 90% success rate, the SWR is closer to 2.2%. While a 2.2% SWR may seem implausibly low, it is what global investors would have experienced historically in a low-yield environment.

There are many oversimplifications with this analysis. For example, it assumes spending increases annually by the rate of inflation, retirement is a fixed period, retirees won’t adjust withdrawals, and that even if the retiree falls $1 short, they would have failed. These issues need to be considered when determining the appropriate withdrawal rate, but the historical evidence paints a depressing picture about what is a reasonable SWR, especially in a low bond-yield environment.

What if yields rise?

It’s not clear how long low bond yields will persist. Using historical data back to about 1900, bond yields have been somewhat mean reverting after about 15 years. In other words, while they drift over time, they tend to return to their long-term average (which has been about 5% for 10-year government bonds globally).

However, using very long time series, there is evidence that lower bond yields may persist into the future (and potentially get worse). For example, Schmelzing (2020) demonstrated that bond yields have persistently declined since 1311 and that the bond yields at the end of 2018 (a real yield of approximately 0%) is relatively consistent with the (super) long-term relation.

We don’t know how long this new bond-yield environment will persist. Advisors may be hesitant to assume that bond yields will remain low forever and unsure how incorporate a reversion to historical returns in their financial plans.

One approach is to use an average by blending near-term forecasts with a long-term average. If yields today are 1.5% and long-run yields are 5%, why not project 3%? But this approach does not accurately capture return expectations for investors with different time horizons. For example, an investor with a five-year investment horizon is stuck with today’s lower returns. The returns for an investor with a 50-year investment horizon are far less certain. Using the same average return for both risks an outcome that is inconsistent with either period.

Therefore, an approach that better captures the uncertainties of longer term investing is to create two sets of return assumptions: a short-term (conditional) set of values that incorporate the current market environment and long-term (unconditional) set of values that reflect longer term expected returns (that are based on long-term fundamentals). Most investment shops that release forecasts only provide conditional estimates (return forecasts for the next five to 10 years).

Conclusions

Using only historical U.S. returns seems reasonable, but it creates a false sense of safety for a financial plan and can lead to bad decisions. Unrealistic future return assumptions also distort potential tradeoffs when advisors are developing a retirement income plan. Not only could overoptimistic projections lead to the risk of spending too much, assuming government bonds will yield 4.5% (the approximate long-term U.S. average) improperly discounts the benefits of delaying claiming Social Security retirement benefits and the use of immediate and deferred annuities.

David M. Blanchett, Ph.D., CFA, CFP®, is head of retirement research for Morningstar’s Investment Management group and an Adjunct Professor of Wealth Management at The American College of Financial Services.

Views expressed are his own and do not necessary reflect the views of Morningstar Investment Management LLC. This blog is provided for informational purposes only and should not be construed by any person as a solicitation to effect or attempt to effect transactions in securities or the rendering of investment advice.

Michael Finke, PhD, CFP®, is a professor of wealth management, WMCP® program director, and the Frank M. Engle Distinguished Chair in Economic Security at The American College of Financial Services.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All