Chief Economist Scott Brown discusses the latest market data.

In an online discussion, Fed Chair Powell repeated that the central bank is a long way from achieving its inflation and employment goals (implying no change in short-term rates or the money pace of asset purchases anytime soon). Asked about the recent rise in bond yields, Powell said, “I don’t want to be the judge of a particular level of long-term interest rates,” but he added that he “would be concerned by disorderly conditions in markets or a persistent tightening in financial conditions broadly that threatens the achievement of our goals.”

Nonfarm payrolls rose more than expected in February (+379,000 overall, +465,000 private), despite the impact of poor weather. However, we are about 9.5 million jobs below where we were a year ago, and we would have added up to two million more jobs if not for the pandemic, leaving us a very long way from full employment. The unemployment rate edged down to 6.2%, but the broader U-6 measure remained at 11.1%.

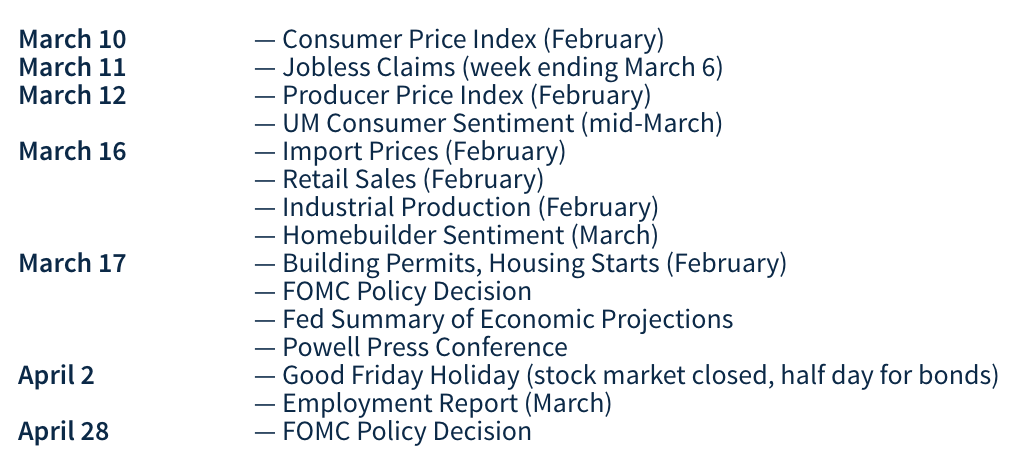

Next week, Fed officials are in the quiet period ahead of next week’s Federal Open Market Committee meeting, but inflation concerns are likely to remain an issue for financial market participants. The Consumer Price Index is expected to reflect higher gasoline prices in February, but core inflation is likely to remain low, due largely to modest gains in homeowners’ equivalent rent. Pipeline inflation pressures should be more evident in the PPI, but it takes a very large increase in commodity prices to have even a small impact on inflation at the consumer level.

Indices

Consumer Money Rates