With 2022 finally over, and not soon enough, such is an excellent time to review our “investor resolutions.”

Advanced economies and emerging markets are increasingly engaged in necessary "wars" – some real, some metaphorical – that will lead to even larger fiscal deficits, more debt monetization, and higher inflation on a persistent basis.

Nikko Asset Management’s Global Investment Committee recently got together to discus their views heading into 2023.

U.S. equities closed out 2022 in the red, and all three major indexes registered solid losses on a yearly basis. The stock market posted its worst yearly decline since 2008.

George Milling-Stanley of State Street Global Advisors provides his outlook for gold in 2023, as well as the specific headwinds and tailwinds he expect to drive price activity moving forward.

Any way you slice it, 2022 was a turbulent year, from Russia’s invasion of Ukraine to historic inflation and jumbo rate hikes to multiple failures in the digital asset space.

Much ink has been spilled over the death of the 60/40 portfolio.

The February crude oil contract CLG23 was down over 2% in trading early Thursday.

Washington Policy Analyst Ed Mills outlines key components of the new legislation.

The Aiguille du Midi, neighboring popular Mont Blanc in the French Alps, is famous for having the highest vertical ascent cable car in the world, a vertigo-inducing ride that is equal parts scary and awe-inspiring.

U.S. stocks are rising in pre-market trading, looking to rebound from yesterday's drop.

We want to wish everybody a Happy Holiday season!

Bear markets end with widespread capitulation while a chorus of the stock trader’s prayer (God, if you get me out of this mess, I swear I will never buy another stock) spreads through out the land.

Enjoy the latest Newsletter from Harold Evensky.

Extremely harsh weather conditions from winter storm Elliot resulted in thousands of flight cancellations last weekend.

U.S. stocks continue to oscillate around the unchanged mark.

U.S. stocks are rising in pre-market action in the first trading session of the week following the long holiday weekend.

The market dislocations and skyrocketing inflation of the last year put longstanding retirement maxims to the test and that test isn’t over yet.

Managing your portfolio has more to do with gardening than you might imagine.

The big question heading into 2023 is the dreaded “R” word.

U.S. equities are modestly higher but near the unchanged mark in pre-market action.

Review the latest portfolio strategy commentary from Mike Gibbs, managing director of Equity Portfolio and Technical Strategy.

I’m not sure where I’m going these days.

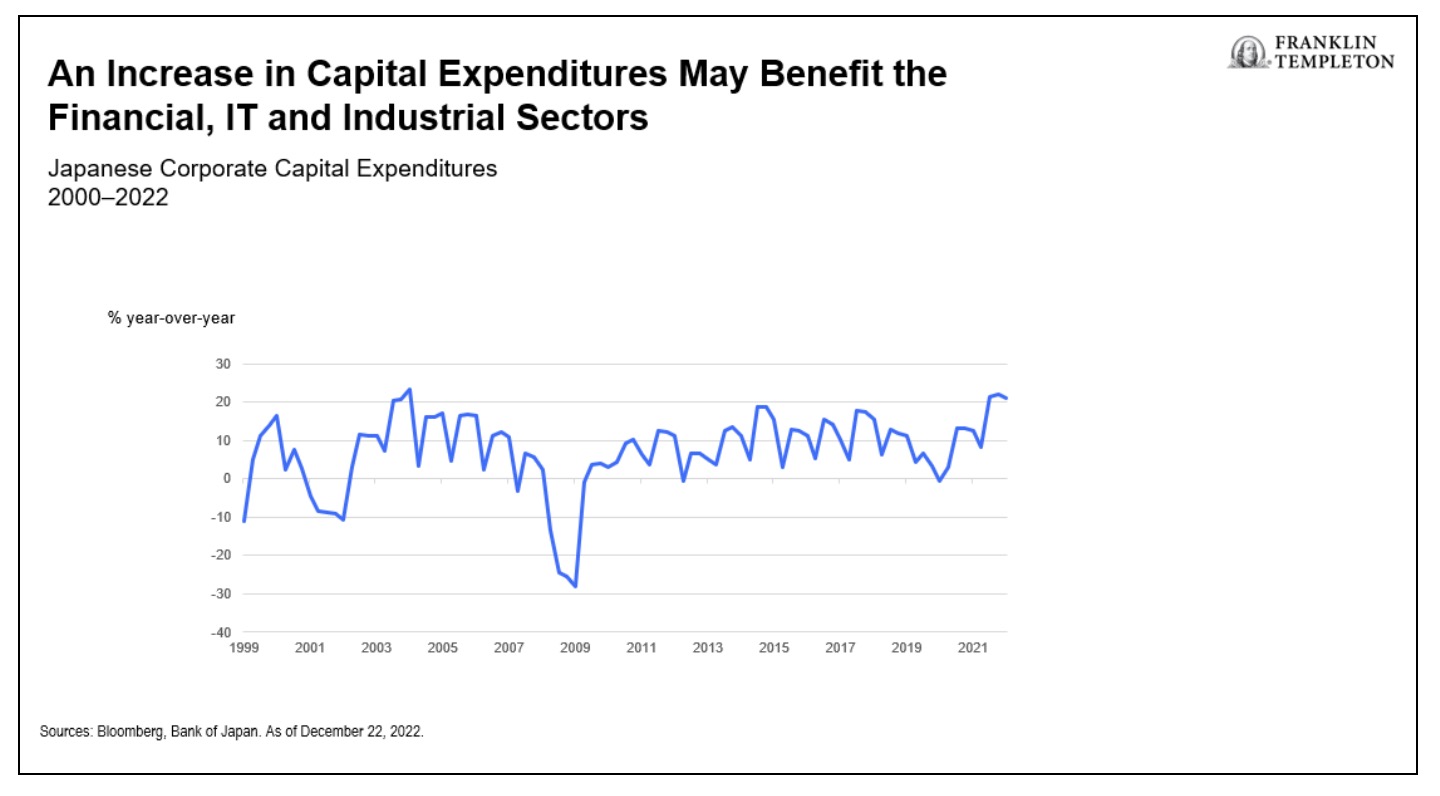

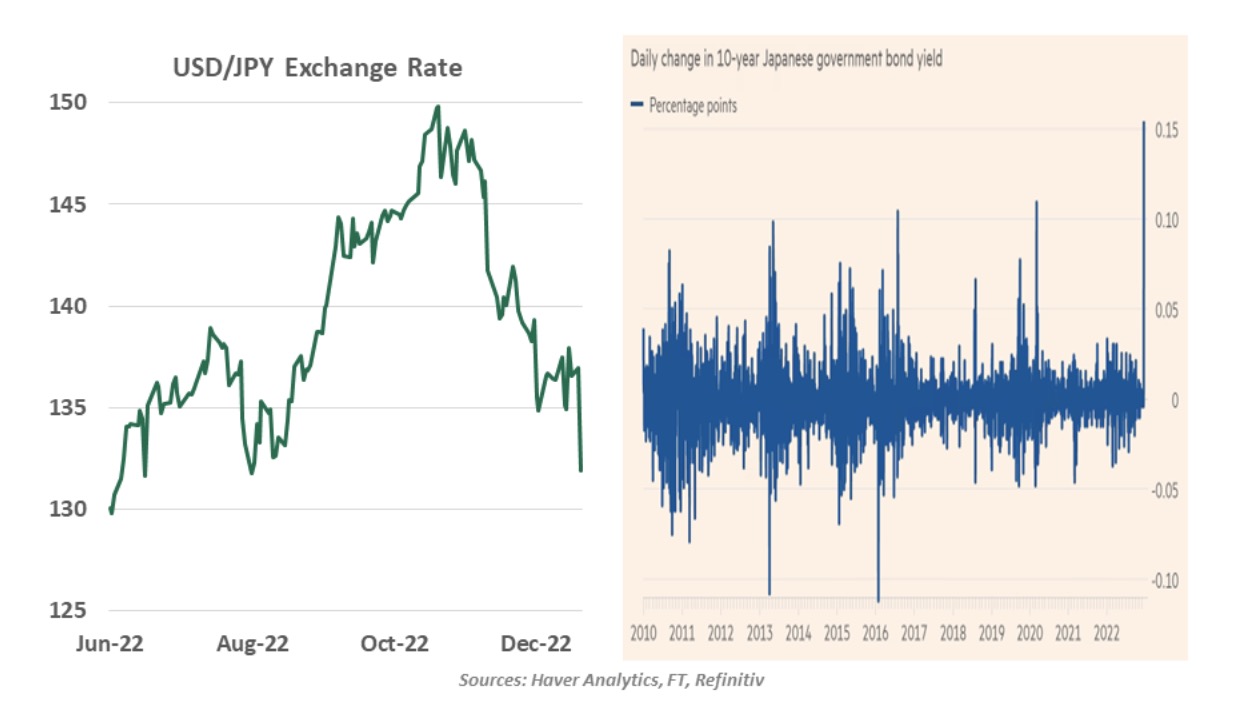

Templeton Global Equity Group weighs in on inflation’s emergence in Japan, recent monetary policy shifts, and the implications for investors.

U.S. stocks are falling sharply, giving up yesterday's rally.

Rick Rieder and team outline how to think about portfolios as we enter 2023.

Last week Zero Hedge achieved the impossible, they managed to make a report from the Philadelphia Federal Reserve go viral.

As of Friday, December 16, the S&P 500 Index is down -19.7% from the most speculative level of valuations in U.S. history – exceeding even the 1929 and 2000 extremes, based on the valuation measures we find best-correlated with actual subsequent market returns in cycles across history.

GMO 7-year asset class forecast: November 2022,

A surprising shift in Japan's monetary policy.

One of the most common complaints I hear from investors is that their advisors or brokers like to tell them when to buy a stock, but never tell them when to sell.

In a recent San Francisco Federal Reserve Publication titled “Monetary Policy Stance is Tighter Than Fed Funds Rate,” the authors argue that the “all in” policy rate is actually higher than the Fed Funds rate would suggest.

Capital represents the resources and labor used to produce goods and services.

As the second-largest economy in the world, China’s reopening has important economic and market implications. Here are some key considerations.

It appears to us at Smead Capital Management that investors are behaving in a way that will damage their capital and cause them to suffer stock market failure.

In 2023, the math of valuations suggests returns will likely be challenging as markets remain difficult to navigate.

What a difference a year makes!

The economics teams looks back at the most significant stories we covered during 2022.

The credit cycle and the economic cycle are excellent leading indicators of volatility.

Considering that a new year almost always brings surprises of one form or another, we've highlighted our top five that may define the global markets in 2023.

The Fed has massively inverted the yield curve. We explain why investors might be frontrunning themselves and why the long-term rate won’t budge.

Over the past two years, the US Federal Reserve has repeatedly erred in its analysis, policymaking, communications, and governance.

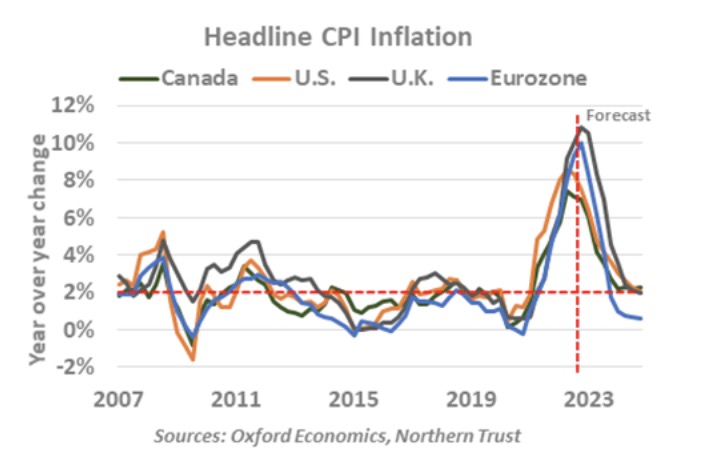

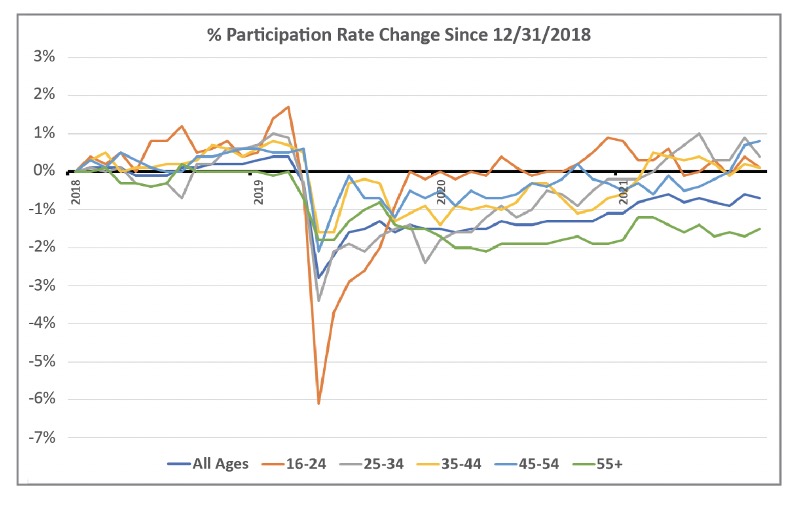

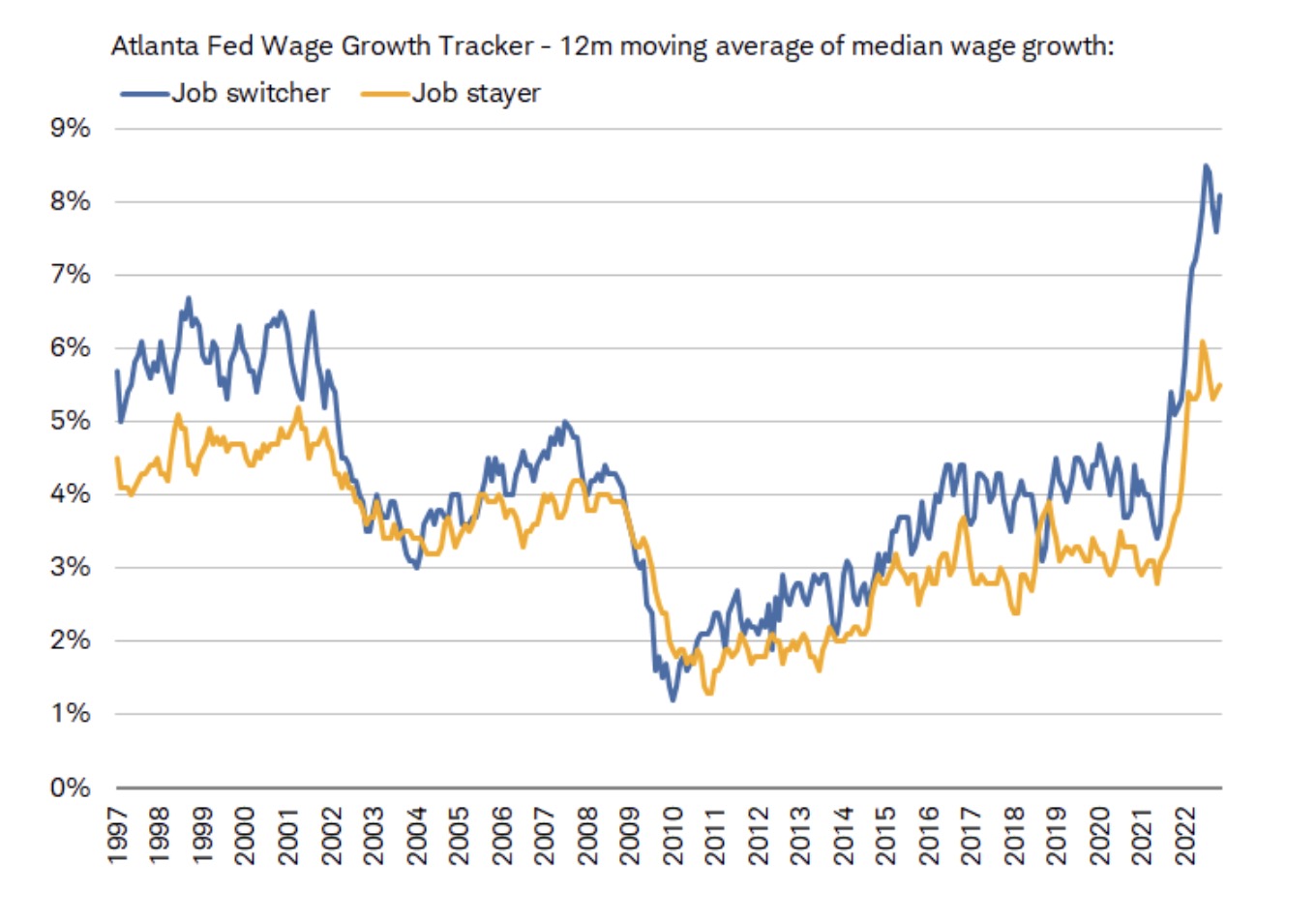

Structurally tight labor markets are providing support for tighter monetary policy, but the Fed may be fighting an uphill battle.

Inflation trends are moving in a favorable direction, but the change is likely too slow for the Fed to take its foot off the brake anytime soon.

This fall was a memorable time in the Halverson household.

As investors hope for a Santa Claus rally in the days ahead, the Grinch is looking to steal their holiday cheer.

This will be my last letter of 2022. I want to use this letter as a set-up for my annual forecast issue the first week of January. That means we will touch on a variety of topics, kind of a snapshot into where my mind is today. Get ready to travel the world but let’s start at home with the Federal Reserve meeting this week.

This important milestone is the culmination of decades’ worth of research and lots of trial and error, and it makes good on the hope that humanity will one day enjoy 100% clean and plentiful energy.

Chief Economist Eugenio J. Alemán discusses current economic conditions.

Stephen Dover, Head of Franklin Templeton Institute, shares his scorecard on some market prognostications for 2022, and what his team is watching in 2023—from blockchain to balanced portfolios.