Energy infrastructure has long been attractive for its generous yields, but it offers other benefits that are particularly relevant today, including real asset exposure in an inflationary environment.

With the equity market trading near record highs and bond yields near historic lows, explore how we think a third alternative – ASYMmetric returns – may be able to help de-risk your portfolios.

The recent sell-off in short-term U.S. Treasuries has created an opportunity for savvy savers unseen in more than two years.

For the better part of a decade, credit investors like David Sherman have been waiting for the market to come back down to earth.

This Halloween season, Rick Rieder and team shed light on today's market ghosts, ghouls and goblins and how to build a resilient investment portfolio around them.

Successful international investing includes measuring financial risks and rewards caused by events in an affected country. Stephen Dover, Head of Franklin Templeton Investment Institute, discusses how macroeconomic and political research complemented by environmental, social and governance (ESG) research provides investors additional prisms to view a country’s financials, impacts on climate change, and geopolitical risk.

The volatility that has roiled short-term bonds signals a shift in expectations for central bank policy in developed markets.

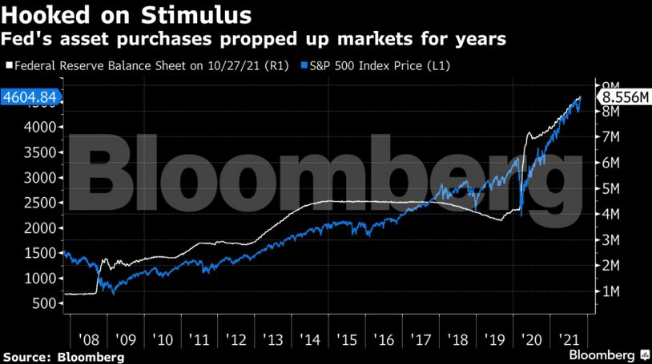

Jim Cielinski, Global Head of Fixed Income at Janus Henderson Investors, discusses concepts surrounding the current bond market environment, including the US Federal Reserve and their lessons learned from past tapering discussions.

The 60/40 is not dead, will never die, and you can’t kill it. That won’t stop the financial media and investment firms from staging mock funerals.

Earnings reports were mixed. Bond yields declined, as market participants generally expect the Fed to raise short-term interest rates earlier to get inflation under control.

Michael Glachun shares why he thinks this cycle has three distinctive features that could propel a faster pace and greater magnitude of Fed tightening than the market seems to expect.

We believe the traditional 60/40 portfolio will face significant headwinds in meeting investor objectives as we move through this decade and the next. Against this backdrop, Scott Welch discusses how WisdomTree seeks to challenge the traditional 60/40 approach.

As is the case with Evergreen, our partner firm Gavekal encourages an environment of “opinion exchanges”. In the latter case, much of that stems from the inherent philosophical divergences regarding economics and politics between its three co-founders.

These “perfect storm” disruptions have created numerous headaches for shipping and logistics companies. But as is often the case, bad news is good news, especially for investors who have seen shares of container lines surge in the 18 months since the pandemic began.

September lived up to its reputation as a bad month for stocks. Global equity markets declined more than 4%, making September the worst month since the start of the pandemic. Beyond seasonal weakness, many attributed equity losses to higher interest rates.

Robert Horrocks, PhD, discusses how he navigates and invests in a challenging environment, especially in China amid recent regulatory actions.

Is the Fed’s aggressive policy, which purposely goes against its mandate, hiding something?

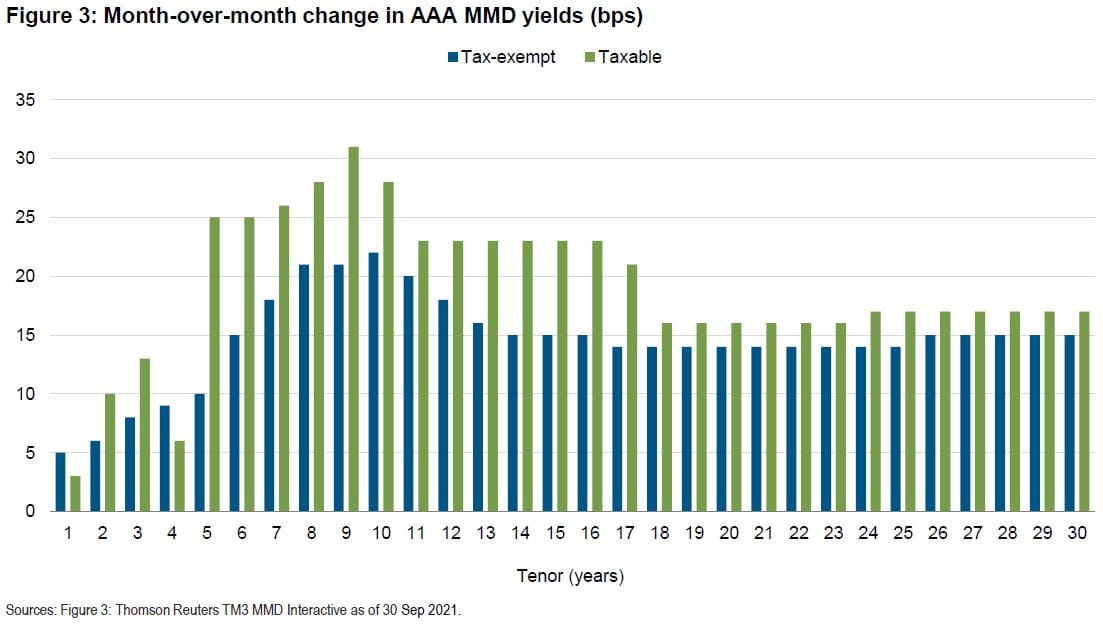

We believe the municipal markets should remain strong into 2022, although the good news may already be baked into high quality bond valuations.

Energy prices have surged to multi-year highs amid the global economic recovery from COVID-19, contributing to larger-than-anticipated jumps in measures of headline inflation. While some policymakers had suggested inflationary forces would prove “transitory,” today many are questioning that thesis.

Performance highlights from the third quarter of 2021, plus manager expectations for the final months of the year.

Like all rules on Wall Street, Bob Farrell’s rules are not hard and fast. There are always exceptions to every rule, and while history never repeats exactly, it often “rhymes” closely.

The bond market’s age-old measure of growth is flashing an ominous warning as the world’s central banks move closer to boosting interest rates from near record lows.

Today’s atmosphere is one that we rarely see as investors. This is not like junk bonds in the 1980’s or the run up in Valeant Pharmaceuticals and the other generic drug companies in the 2010’s. There is not a narrow way of looking at today. It is broad.

Treasury reported a federal budget deficit of about $2.8 trillion (about 12% of GDP) for FY21. Barring a major unforeseen event, the deficit will fall considerably next year. By itself, that will be a negative for GDP growth, but a further strengthening in private-sector demand should more than offset that.

By now investors are quite aware of the consequences of financial repression via negative real interest rate policies. Since interest rates on “risk free” government debt are too low to even compensate for inflation, it pushes investors out the risk spectrum in an effort to achieve a positive rate of return after inflation.

Cathie Wood’s flagship fund is still underwater for the year, even as its top holding soars to an all-time high.

John Vail, Chief Global Strategist at Nikko Asset Management, takes a deep dive into the firm’s 12-month outlook for the global economic recovery, and explains where he is finding the greatest investment opportunities.

I explore how estimated portfolio loss potential changes with different estimates of asset volatilities. Specifically, I compare portfolio loss potential calculated using Research Affiliates’ outlook for asset class volatility and return versus option-implied and historical volatilities.

Now nearly anyone will be able to convert their loose change into Bitcoin at their neighborhood Walmart. This week, it was being reported that Walmart quietly began installing special Coinstar machines at select locations that give customers the option to buy Bitcoin.

Bond traders are boosting expectations for U.S. inflation to levels not seen in over a decade amid concern supply-chain bottlenecks and resurgent consumer demand will keep lifting the cost of goods and services.

The investment grade market was relatively calm in the third quarter, but we are concerned about undercurrents lying beneath the surface. In particular, we feel the dual threats of persistent inflation and a less accommodative Fed have the potential to impact pricing over the near to medium term.

Interest rates are rising, and bond investors are worried about the potential impact on their portfolios. But they’re not entirely at the mercy of the markets.

Expectations of the Fed’s liftoff in short-term interest rates have continued to inch forward and bond yields have moved moderately higher. However, investors remain optimistic, looking beyond recent concerns (the delta variant and supply chain and labor issues).

Despite multiple headwinds, including increasing inflation, rising rates, and tight labor markets, our view is that the U.S. economy is in good shape. Markets may experience higher volatility as the Fed begins to taper its bond buying program, but we expect that to be a short-term issue.

Reducing exposure to equities and bonds to accommodate non-correlated assets or alternative strategies may reduce risk, but at the expense of lower potential returns and painful tracking error. We introduce a novel investment concept, accessible to all investors, which is designed to seek higher returns with less risk and low tracking error by using new products which, in combination, can provide more than $1 of exposure for every dollar invested. The proposed solution harnesses the full potential of traditional portfolios plus the opportunity for higher returns and risk reduction from non-correlated investments. We show how to maximize “Return Stacking™” opportunities by choosing alternative fund managers already engaging in capital-efficient strategies.

Among the illusions encouraged by every speculative bubble is the idea that wealth is embodied in the prices of securities – that higher prices inherently represent greater “wealth.” The fact is that every security is, at base, a claim to some future stream of cash flows that will be delivered into the hands of investors over time.

Three transformative trends will lead the world into a radically different macro environment over the secular horizon. Read our long-term outlook and implications to consider when investing.

After beginning the quarter on a relatively upbeat note, familiar themes returned as fears of inflation, ambiguity over the end of the pandemic, and uncertainty about the future of Chinese capitalism raised concerns for investors.

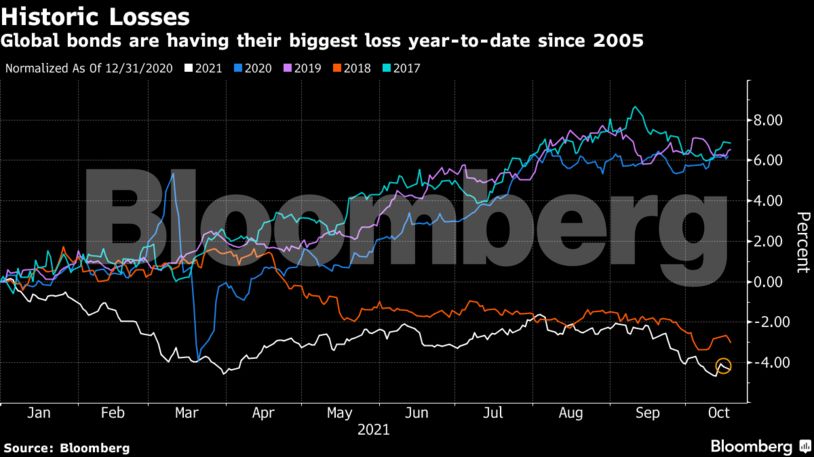

Global bond investors face an old enemy -- inflation -- and the universe of fixed-income assets doesn’t look to offer much in the way of shelter.

We are in uncharted waters on many fronts, so no one can really answer that inflation/deflation question with any degree of certainty. We can however, look to the technical condition of commodity markets for guidance, since they have usually, acted as a barometer for more generalized swings in inflationary and deflationary pressures. Commodity prices look poised to signal a new secular bull market, which would likely broaden out to result in the highest more generalized inflation rates since the 1970’s.

The age of abundance has given way to an age of scarcity, while the pro-cyclical version of inflation may have given way to the counter-cyclical version.

New projections of the labor force growth rate by the US Bureau of Labor Statistics show the US labor force growth accelerating in the 2020s for the first time since the 1970s.

Volatile, pandemic-riven markets for stocks and bonds has Wall Street ready — again — to declare the traditional 60/40 portfolio split a dead strategy. The prospect of a low-growth, high-inflation economy (stagflation) dims the prospects of both investment categories, and certainly demands a rethink of where to stash your savings.

Demand is so strong for green bonds, or debt that funds environmentally friendly projects, that investors are accepting lower yields for securities that are harder to trade, according to Barclays Plc.

The Fed's more hawkish stance at September’s FOMC meeting, rising upside inflation pressures, and near-term volatility drove Treasury yields higher at the end of the month.

We’re all familiar with inflation. But did you know there’s another form of inflation that’s just as corrosive on our purchasing power and yet is nearly impossible to measure? Read on to learn more.

September closed with a whimper (from folks hoping the seven-month stretch of positive performance months for the S&P 500 would make it to eight). The month also held true to the history of September being the worst month for performance on average since the index’s inception in 1928.

As Mark Twain might have put it, the demise of debt’s value within the long-favored 60-40 stock-bond diversified portfolios is greatly exaggerated -- when you adjust for risk.

The strong economic and market trends of the first half of 2021 wavered during the third quarter. The coronavirus delta variant caught up with the US at the height of the summer, just as vaccinations slowed and concerns grew that inflation might flare and persist.

It’s taken just a few short months for stagflation to go from hobgoblin of cranks to a full-blown Wall Street obsession.