Dividend Growth Stocks Dividend growth stocks are one of the more favored classes of stocks that investors want to hear about.

Heightened market volatility has led to misconceptions about credit, in our view. We dispel four of them here.

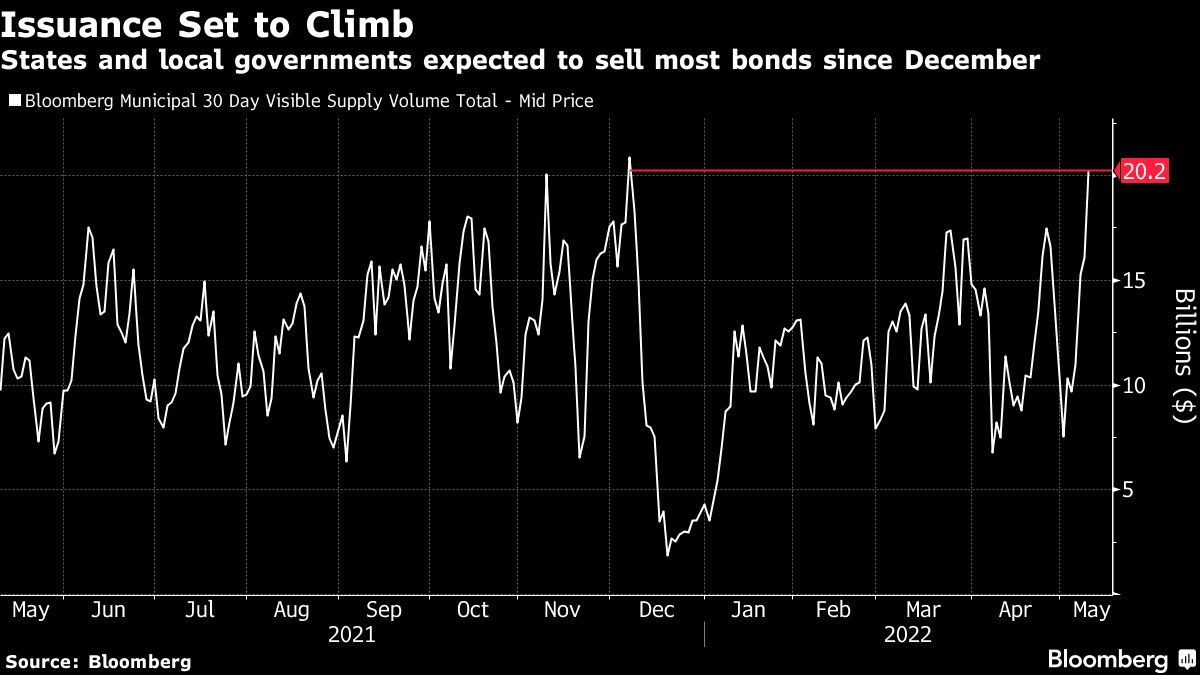

The nation’s local governments are expected to sell $20.2 billion of debt over the next month, the most since early December, according to a Bloomberg index that tracks municipal bond sales announced for the next 30 days. The gauge doesn’t represent the full tally of what actually hits the market, as many deals come with less than a month’s notice.

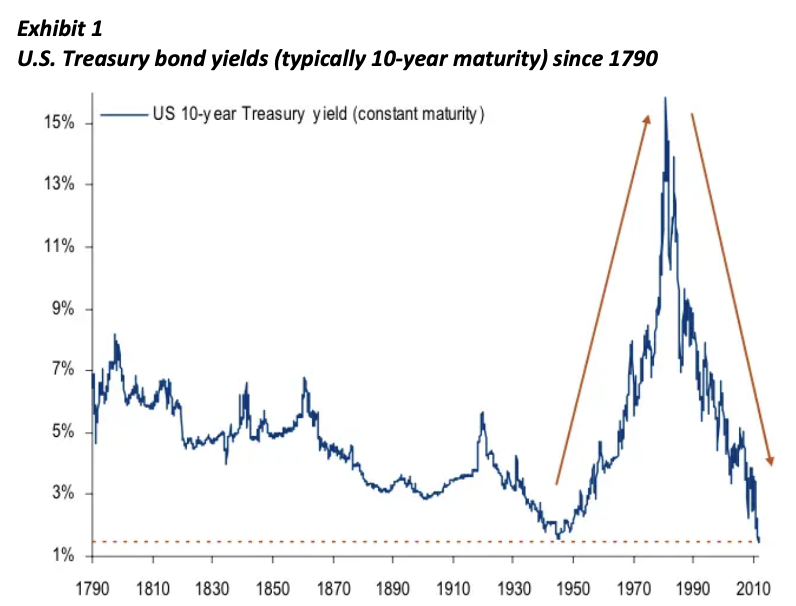

There was a time, some 12 years ago, when I bowed to no one in my enthusiasm for bonds. Longer-dated government debt yields had surged after the global financial crisis. Yet for various reasons, inflation was likely to remain subdued, I argued. US Treasuries and even German bunds yielded about 3.5% at the time. Although headline inflation waxed and waned, it consistently came in below forecasts for the next 10 years.

Pre-retirees are facing the perfect storm of risks. Inflation is spiking, yields are low, markets are volatile, taxes are unpredictable – all while Americans are reaching new peaks of longevity. You can’t predict what’s going to happen next. But you can help investors prepare. Join us for a discussion on innovative structured strategies using Defined Outcome Funds. These strategies can help you better control investment outcomes – providing a unique return profile distinct from traditional stocks and bonds, offering clients upside agility, downside protection, and substantial tax advantages.

To achieve its mission of reducing inflation, the Fed will keep raising rates, according to Albert Edwards, and won’t stop before the S&P 500 hits 3,000.

U.S. investment-grade debt sales have missed Wall Street estimates for two consecutive weeks with issuers choosing to sit on the sidelines instead of braving volatile markets. Bond sales were expected to pick up this week amid a growing backlog, but seven potential issuers opted to stand down amid broad volatility on Monday.

U.S. stocks suffered another day of losses Monday, as the market continued to weigh the risk that the Federal Reserve’s aggressive anti-inflation campaign could push the economy into recession.

Until recently, inflation and interest rates had been on a secular downtrend after peaking in the early 1980s.

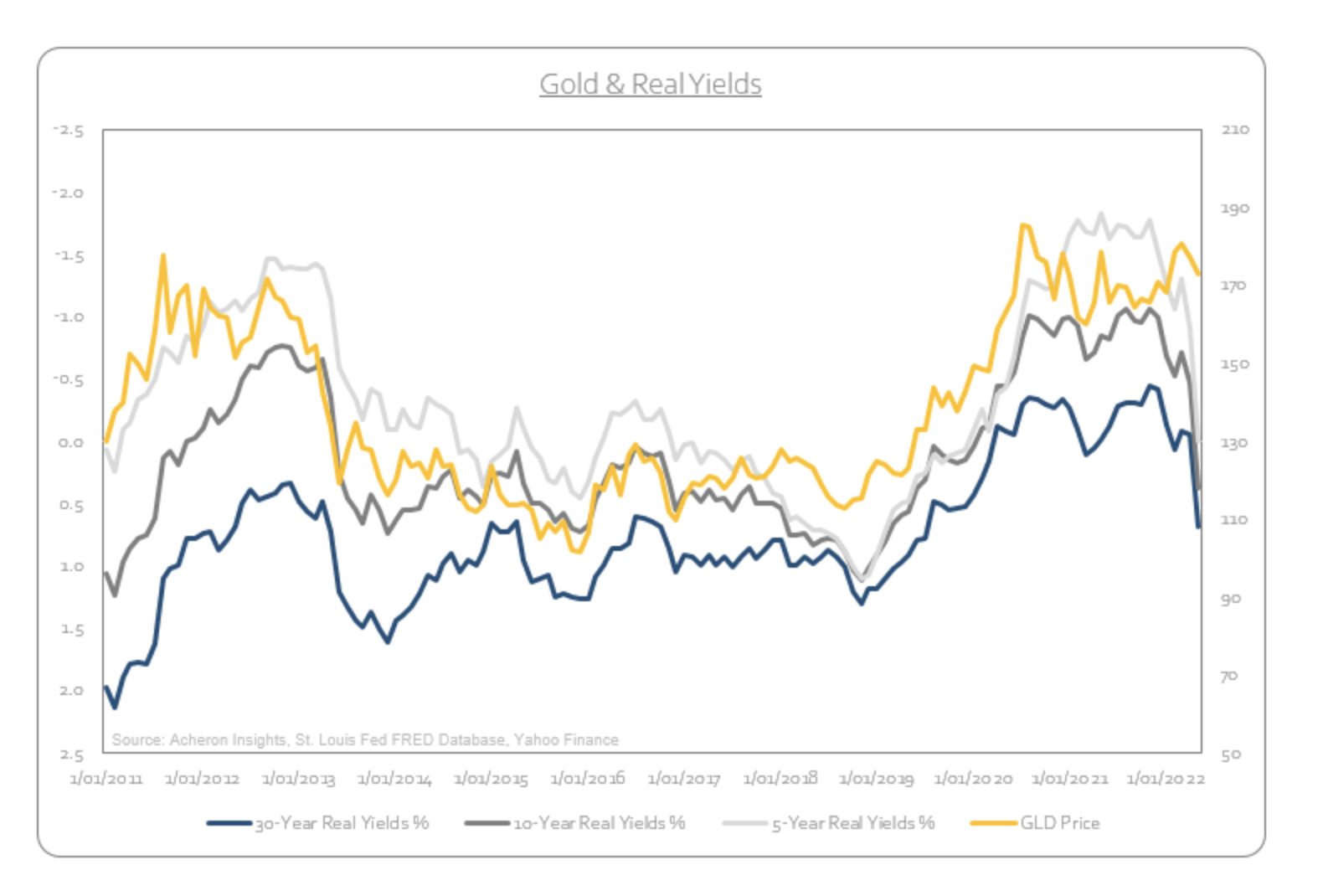

Through rising real yields, a slowing economy and poor seasonality, short-term headwinds remain for gold and precious metals.

The historical data has shown that the value premium is smaller for large-cap securities than for small caps. But new research shows that large-cap investors can increase the premium by pursuing an equal-weighted strategy.

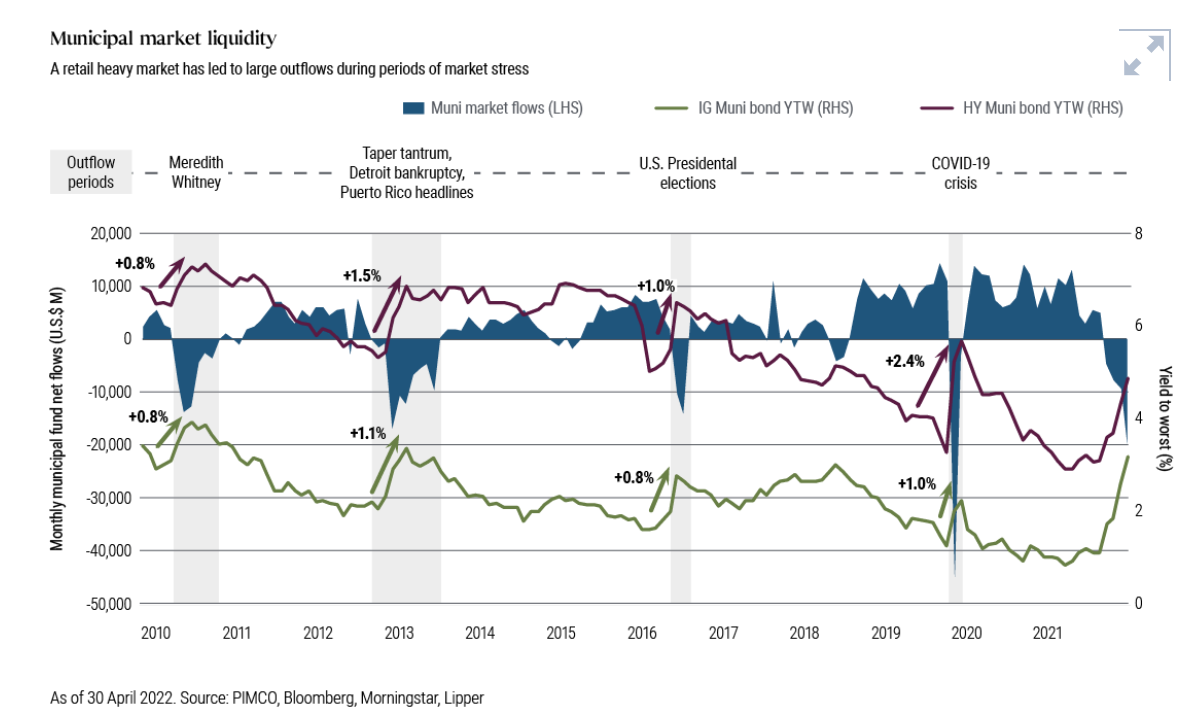

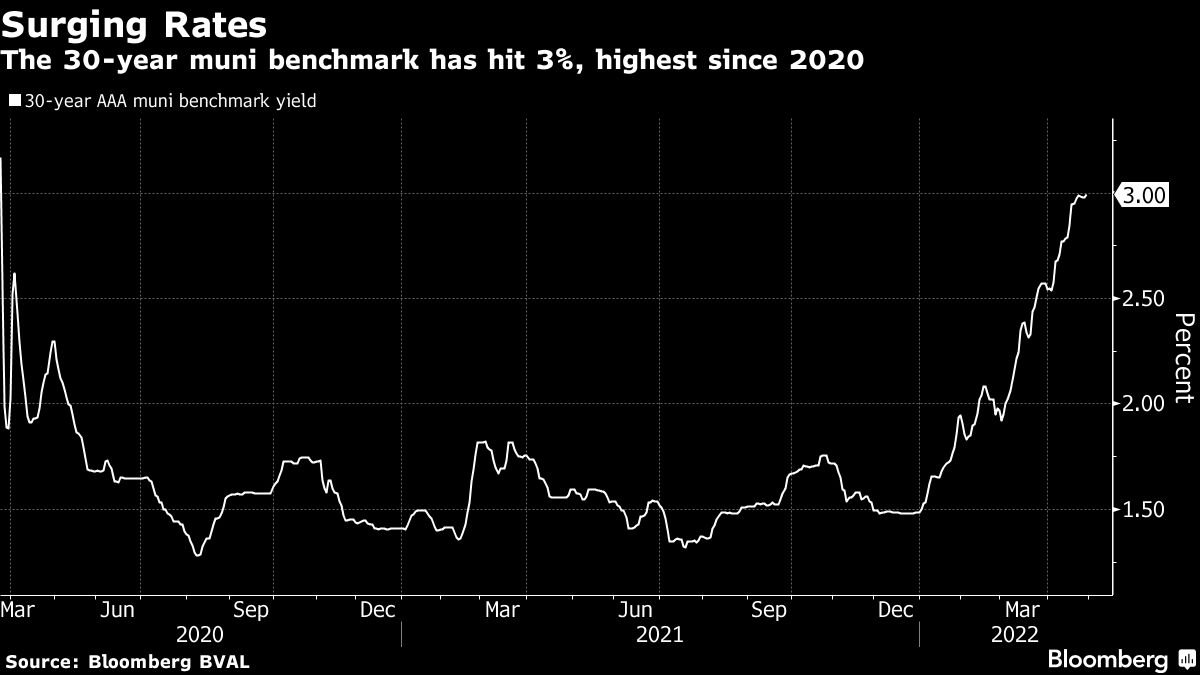

Higher yields, wider credit spreads, and other common market reference metrics suggest relative valuations for muni bonds have become attractive.

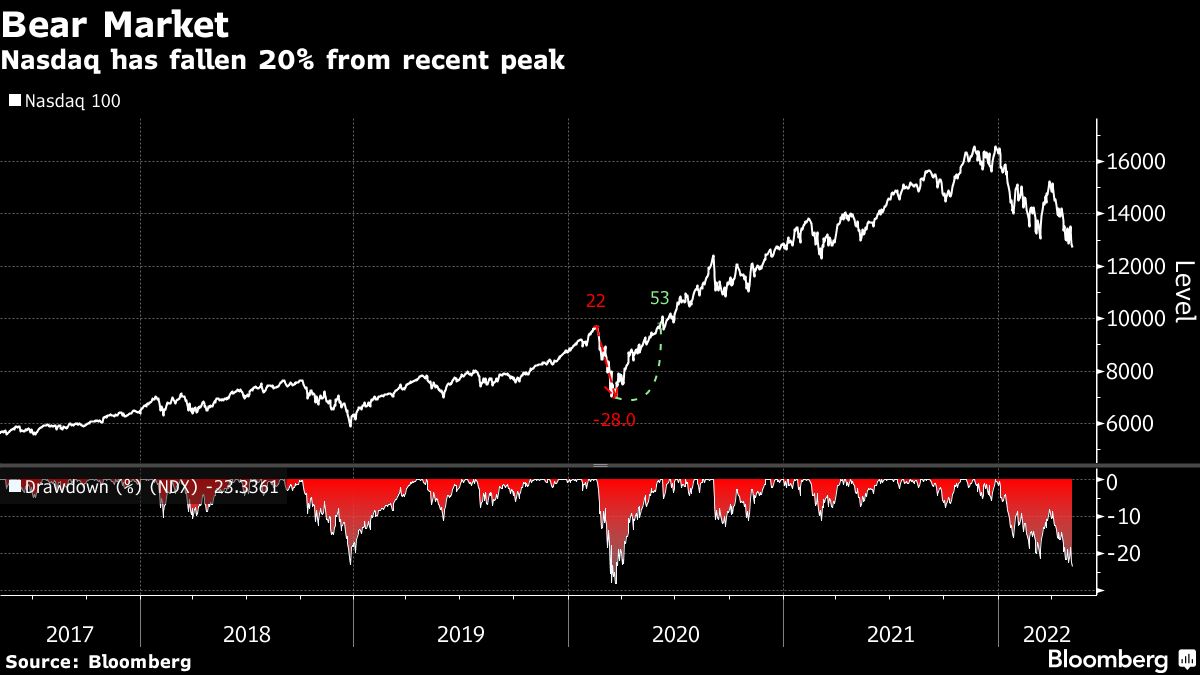

First it was a rout in the stay-at-home names that surged in the pandemic. Then speculative software makers with barely any earnings went south. Now the giant technology names whose sway on benchmarks has been decried by bears for years are dragging the market down.

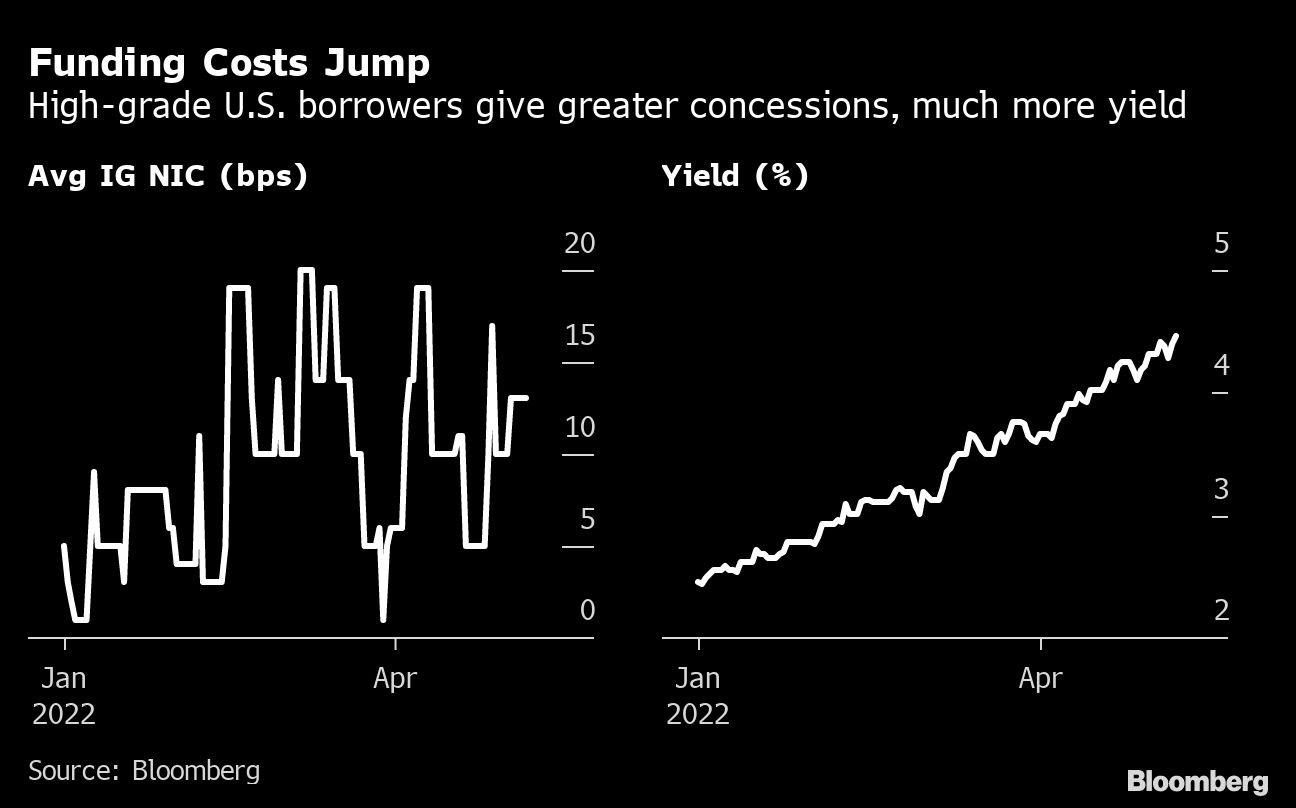

With volatile markets fraying investors’ nerves, companies are now paying the biggest premiums to sell new bonds since the height of the coronavirus pandemic two years ago.

U.S. Treasuries tumbled Monday, driving the yield on five-year notes to the highest level since September 2008 amid speculation persistent inflation will prompt the Federal Reserve to tighten policy more aggressively.

The nature of the economy is that there are always causes for concern in strong markets, just as there are reasons for optimism in weaker ones.

Today the Federal Open Market Committee raised the fed funds rate (upper bound) to 1% from 50bps.

A bull market in bonds is set to return with a vengeance as the Fed once again makes a policy mistake.

As expected, the Federal Open Market Committee (FOMC) raised the fed funds rate by 50 basis points, to a range of 0.75% to 1.0%.

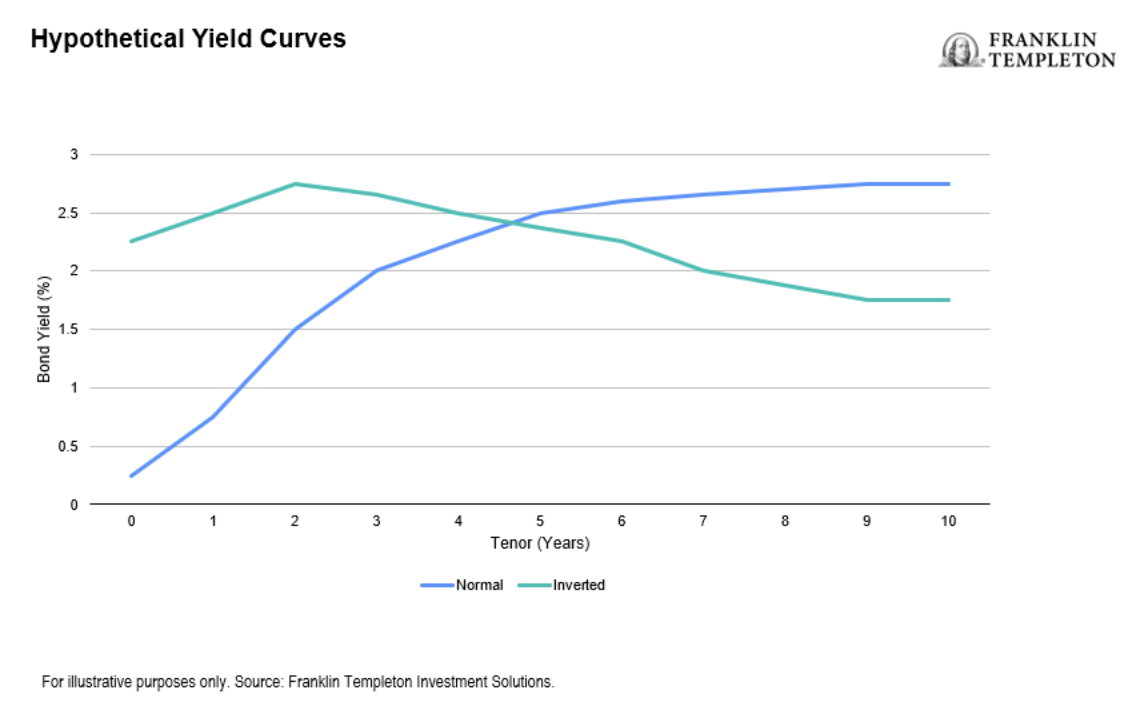

The US Treasury yield curve momentarily inverted.

The Treasury Department said in a statement Wednesday that it will sell $103 billion of long-term securities at auctions next week -- down $7 billion from February. This marks the longest string of quarterly cuts since a 2014-2015 cycle. In a surprise for some dealers, it’s also trimming sales of two-year, three-year and five-year auctions in coming months.

Stocks come in all sizes, shapes, and flavors. Nothing could illustrate that better than the 31 stocks you asked to see last week.

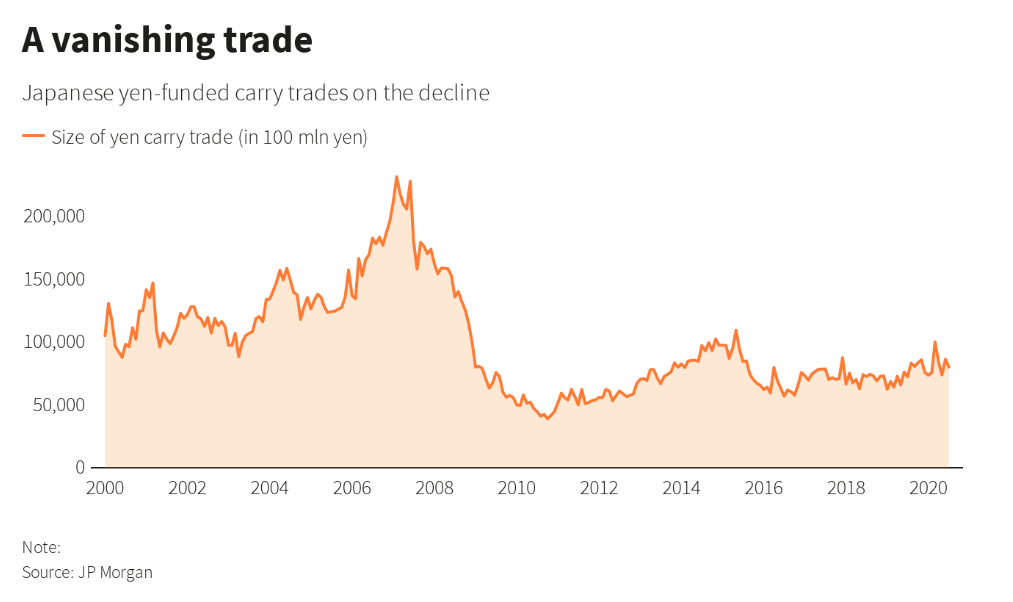

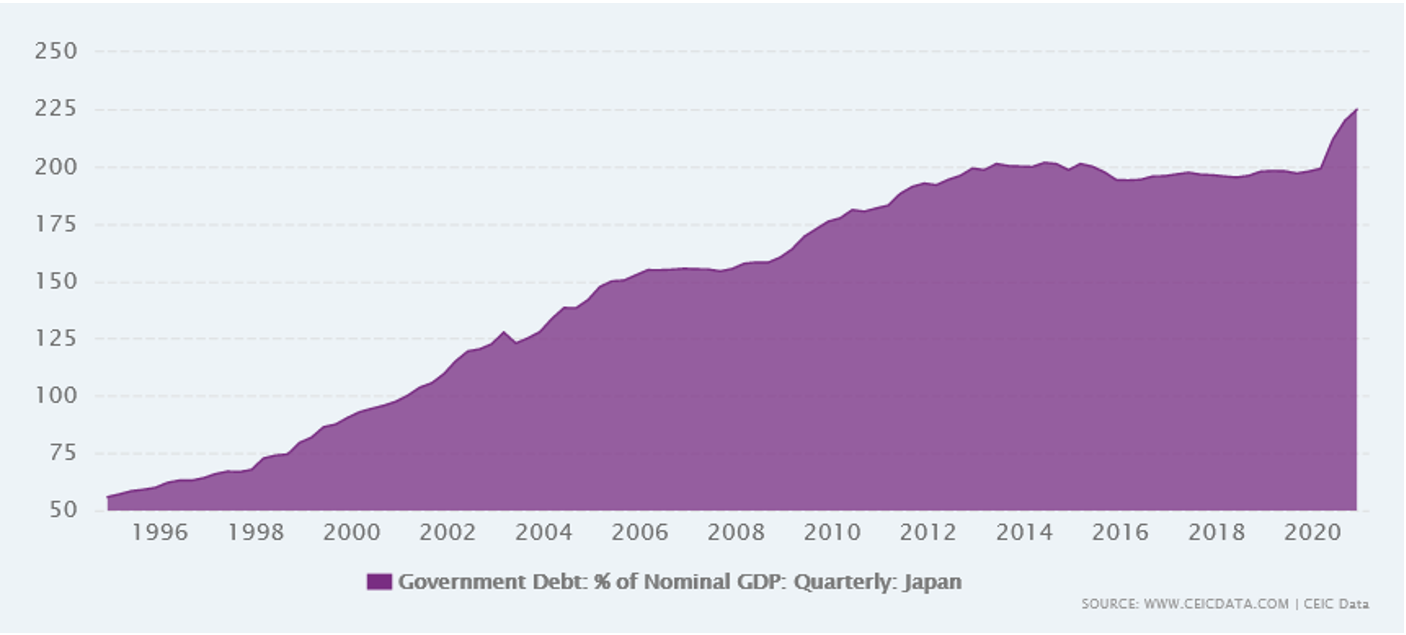

The BOJ is trapped. It is conducting unlimited QE to keep rates low and weaken the yen, which promotes inflation.

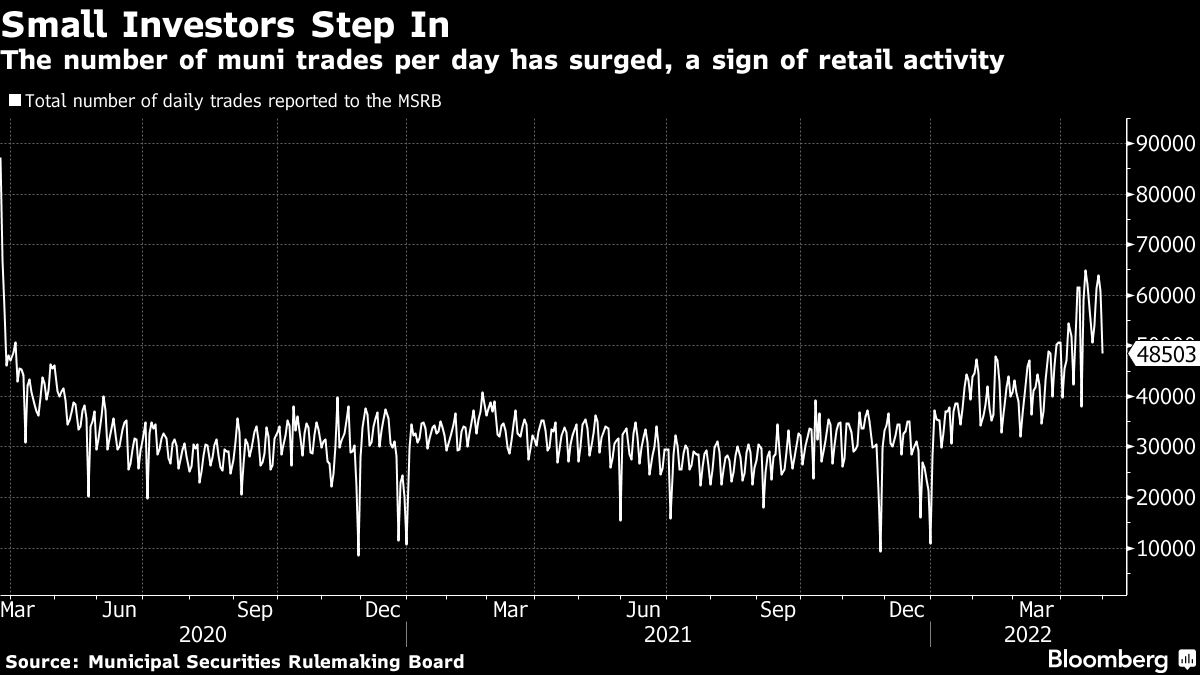

The number of daily trades surpassed 60,000 on a few days in late April, levels last seen during the 2020 pandemic-induced selloff. In March, that figure averaged around 42,600, according to trade data from the Municipal Securities Rulemaking Board.

The U.S. economy will be in recession in the second half of this year, according to David Rosenberg. Equity Investors should brace for a 30% bear market decline.

Even though the medium-to-long term US Dollar fundamentals remain unimpressive, due to a combination of large external imbalances, a continuous dependence on foreign investors’ inflows and the weaponisation of the currency, the Dollar became the least bad currency in G4 since the beginning of the Ukraine war

As we inch closer and closer to what might be the end of the longest business cycle in history, investors everywhere are looking for a safe harbor in which to protect their assets.

In an ambitious new book, the economist Andrew Smithers rejects core “Newtonian” principles of economics, replacing them with radical departures from conventional wisdom. But as I will explain, some of Smithers’ theories fail meet the standard of empirical verification.

Forward-thinking advisors have been searching for and employing analytics very carefully. This series will explore some of these metrics, along with their benefits and pitfalls. Today’s topic is capital markets assumptions.

Investors seeking higher yields and relatively low risk, and are willing to sacrifice liquidity, will find attractive opportunities in interval funds that invest in senior secured, middle-market loans, such as those offered by Cliffwater.

The U.S. stock market is very likely in a bear market that anticipates a recession will start later this year. This means the time is now to shift portfolios from risk-on mode to risk-off before the losses get even worse. But what worked in the past when hedging against a bear market may not work now, given the ever-changing economic dynamics. It’s also important not to fall for some old myths.

If you think it has been painful that the market has been down each of the past four weeks, your nest egg hasn’t seen anything yet.

Markets have already priced in a 50-basis-point hike on Wednesday, expecting the Fed will take a quicker approach in order to squash stubborn inflation. Accelerating U.S. labor costs and a resilient consumer are effectively giving the central bank the green light to raise interest rates by a half-point next week to tamp down price pressures.

Municipal bonds are heading for their worst start to a year on record, and fund managers say nailing the direction of the $4 trillion market from here likely has little to do with the fiscal health of U.S. states and cities.

The push-and-pull between centralization and decentralization is the great contest of our times. And decentralization is winning out.

The most challenging financial event for investors in the coming decade will be the repricing of securities to valuations that imply adequate long-term returns, following more than a decade of reckless and intentional Fed-induced yield-seeking speculation.

In a market environment of low bond yields and record high equity valuations, it’s time to look beyond simple asset-class diversification. A covered call strategy could provide clients with potential for growth, income and downside protection.

Recession warnings are clearly on the rise. Much of the initial media fervor focuses on the inversion of the yield curve.

In propping up Japan's economy and financial markets, its central bank indirectly provided liquidity to the world's financial markets. But the BOJ could unleash a liquidity vacuum felt around the world.

Our view is that the equity market is in a tug of war between a good earnings tailwind and a modest valuation headwind.

Sanctions on Russia’s foreign currency reserves will likely stymie the rise of the Chinese renminbi as a competitor to the U.S. dollar.

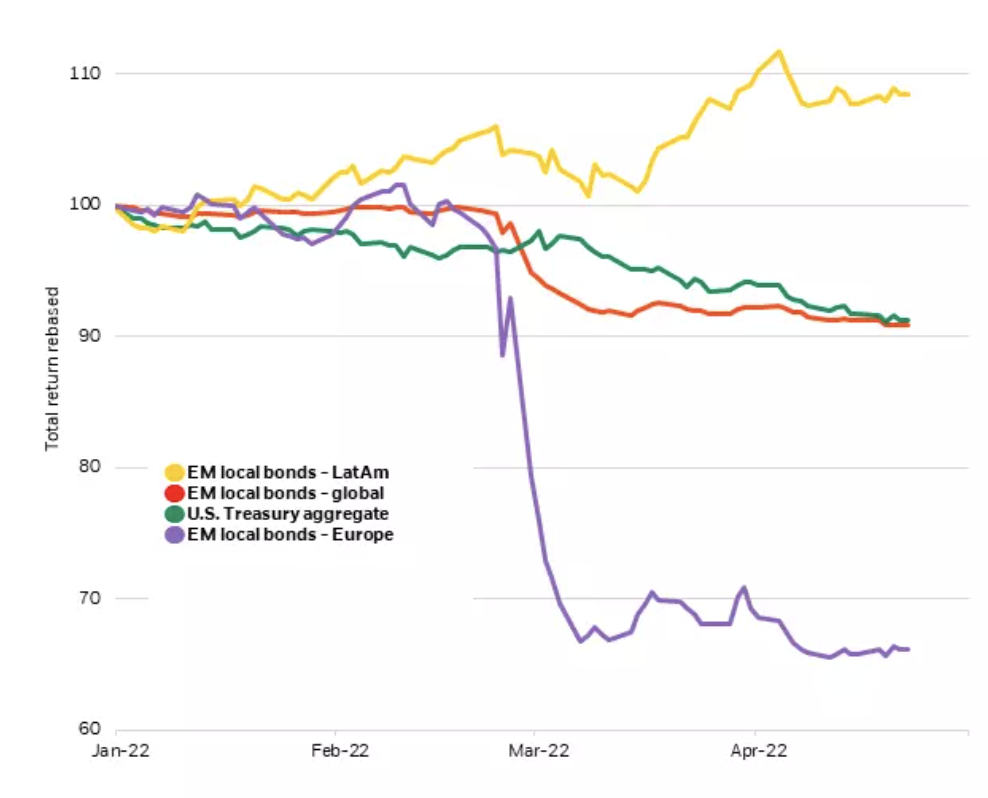

Inflation and hawkish central bank talk have spooked investors and led to bond losses not seen since the 1980s in developed markets (DMs).

ICYMI: In this roundup, we’re highlighting the five most popular pieces of content from the previous week.

U.S. cities and states are paying up to get muni deals off the ground as buyers gain more bargaining power -- a marked departure from the anything-goes market for sellers in the easy-money era.

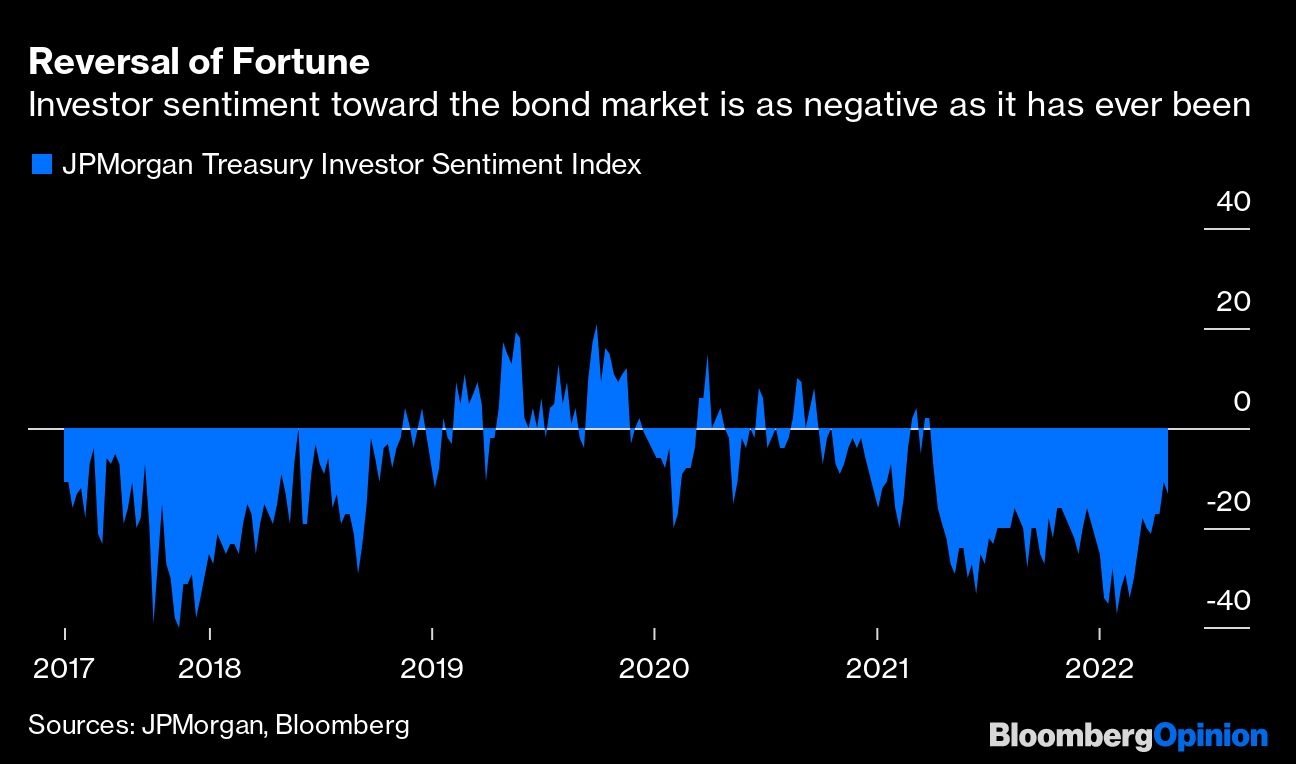

We are panicking over interest rates. Estimates of how high the Federal Reserve will raise its main rate to get inflation under control seem to increase daily. The yield on the benchmark 10-year U.S. Treasury note has surged 1.25 percentage points this year, inflicting historic losses on bondholders.

Stock prices and bond yields have been moving in opposite directions this year.

Disaster is a strong but appropriate word that applies perfectly to the state of U.S. monetary policy.

U.S. stocks fell Friday, extending a run of weekly losses into its third straight week, as investors reacted to a handful of disappointing earnings reports and the Federal Reserve’s increasingly aggressive language about future interest rate increases.

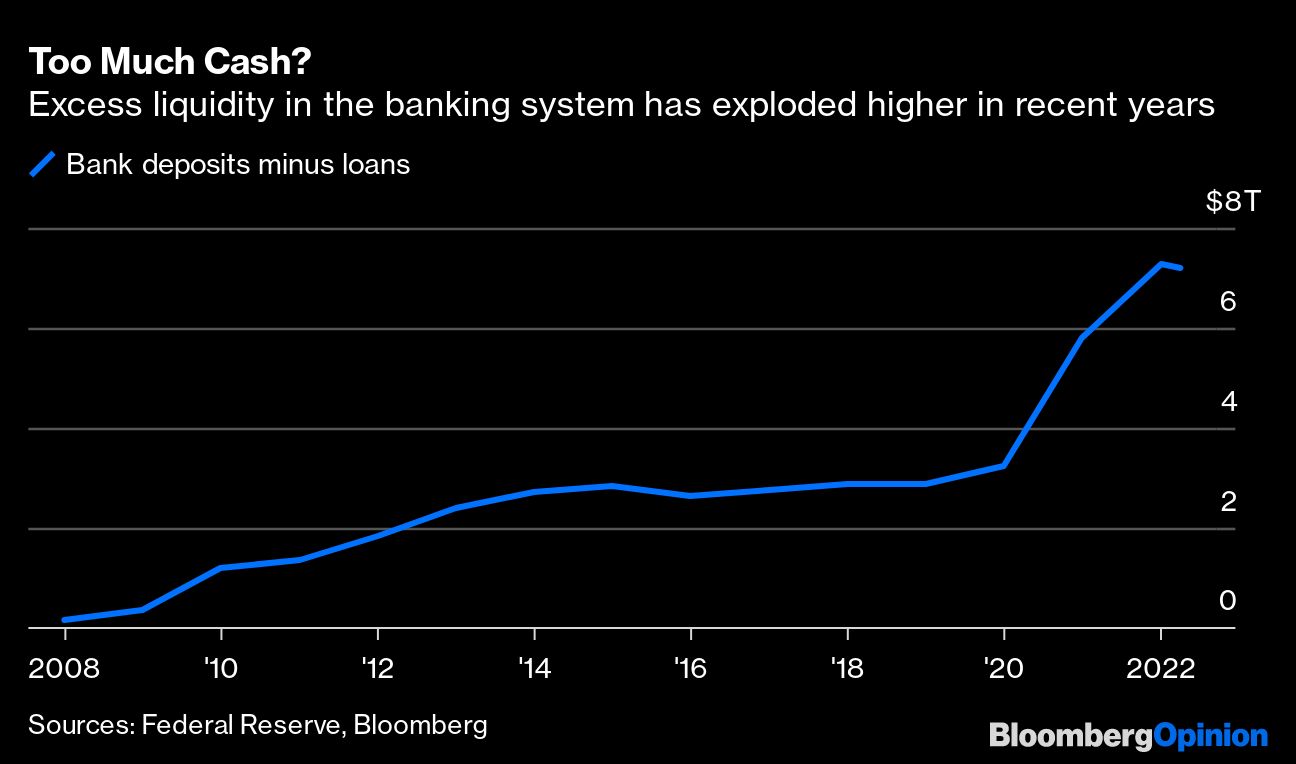

Savers are about to learn one painful and one surprising lesson about interest rates and banks. First, just because the Federal Reserve is raising rates doesn’t mean the rate investors earn on their cash will rise as much — if at all. In fact, the financial repression in the form of zero rates suffered for more than a dozen years by those who are ultra conservative with their savings isn’t going away soon.

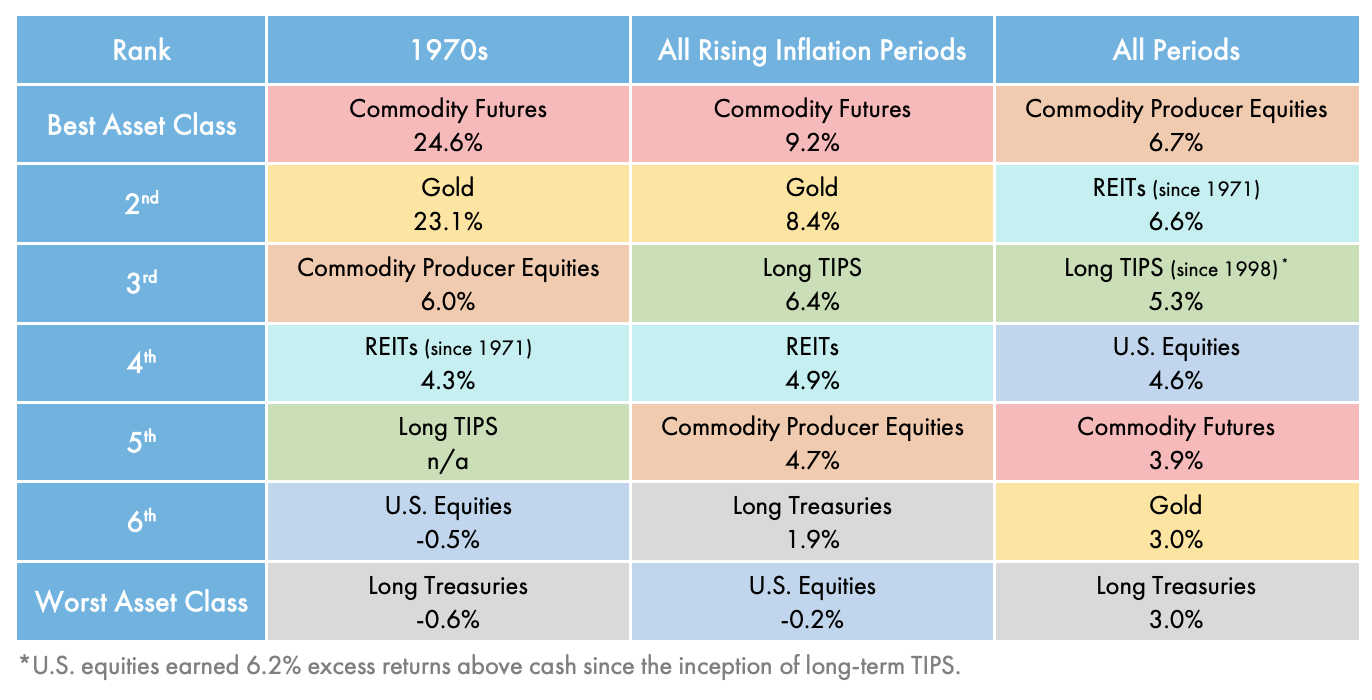

After a multi-decade pause, the winds of inflation have picked up. Only TIPS have been an effective hedge against inflation. Other asset classes have failed to varying degrees.