Is a Rejection of Classical Finance Justified?

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsEinstein’s theory of relativity advanced Newtonian physics. That did not mean Newton was wrong – only that his theories could be improved upon. In an ambitious new book, the economist Andrew Smithers rejects core “Newtonian” principles of economics, replacing them with radical departures from conventional wisdom.

But as I will explain, unlike Einstein, some of Smithers’ theories fail meet the standard of empirical verification.

Looking at the world from a different angle

Sometime in the early 1970s, the comedy troupe Firesign Theater recorded an album called “Everything You Know is Wrong.” It was a satire on “new age” thinking: Dogs flew spaceships! The Aztecs invented the vacation! Men and women are the same sex! Aliens are living like Indians in an Arizona nudist park.

You get the idea.

Smithers’s new book, The Economics of the Stock Market, presents bold and provocative theories that advance our understanding of financial theory. But there are moments that are reminiscent of Firesign Theater – at the extreme, leading one to believe that everything one knows about the stock market is wrong. Here’s Smithers channeling Firesign:

- The expected real equity return is stable, at 6.7%, no matter what is going on in the bond market.

- The risks of equities “fall sharply as the time horizon lengthens.”

- Bond yields fluctuate “within narrow ranges.”

- Companies don’t try to maximize profits.

It's easy to dismiss these sweeping statements that contradict our understanding of markets. But it’s not easy to argue with a man who “in 1956… went up to Clare College Cambridge to read economics,” and who has been thinking about economic principles and putting them into practice for more than 60 years. Smithers is eminently qualified to question the tenets of neoclassical economics as it has been applied to finance in those 60 years, and he does so in an exemplary way: no math, crystal-clear writing, and a rich vein of data graphics.

Classic finance is still correct and relevant – mostly

Smithers’ central thesis is that companies try to maximize their stock price, not profits. Because of the structure of top-executive pay – “pay them in stock,” the legacy of Harvard Business School professor Michael Jensen – companies almost certainly favor maximizing the stock price over some other measure of profit when there is a choice to be made. (I will argue that classic finance is correct in asserting that the stock price is usually the best measure of long-run profit expectations, so that paying executives in stock is appropriate – unless the pay levels get out of hand, a separate issue.)

Smithers then uses this observation to try to overturn classic finance, the work of Harry Markowitz, William Sharpe, Franco Modigliani, Merton Miller, Fischer Black, and Robert Merton.

He fails in that effort.

Smithers does what many critics have done when faced with evidence that their theory doesn’t fit the facts: He seeks to overturn the whole thing. In place of classic finance, Smithers proposes a blend of Keynesian thought (consistent with his Cambridge education) and behavioral economics.

It’s a seductive proposition but doesn’t quite work. As I wrote in a 2014 essay, “Read Your Sharpe and Markowitz,” published by the CFA Institute,

Some of [the] findings [of the long list of pioneering scholars] aren’t exactly right. [But] classic finance forms a base case or null hypothesis against which empirical facts, new theories, and conjectures can be tested. Without it, we are lost. With it, we have a set of very useful guideposts, a little like Newtonian…physics.1

Newton’s theory of gravitation ignored air resistance. That is not a bug but a feature. It says how gravity would behave in the absence of any complicating factors, air resistance being only one. It’s a point of departure for a richer physics that does account for air resistance and any other frictions you encounter in real life. Without Newton, Einstein would have gotten nowhere.

And, while we may adopt some of the ideas suggested by Smithers in crafting a practical model of investment markets that includes “air resistance” – the frictions of living in an imperfect world – the baseline theories of classic finance are correct. We should learn them thoroughly before trying to identify the relevant exceptions.

Why this book review is unconventional

I am not recommending that advisors read this book; it is too long, detailed, and technical for all but the most determined students of finance. But don’t ignore it! That’s what makes this an unconventional book review. Smithers’s ideas, good (so as to include them) and bad (so one can understand and critique them), need to make their way into investor education as a part of the whole picture. That can only happen if the top-level investment thought leaders – writers, economists, consultants, strategists, and chief investment officers – either read this book or what others say about it and grasp its merits and shortcomings.

I’ll discuss Smithers’s central point, that public corporations maximize their stock price rather than “profits.” Smithers, along with many others, alleges that this behavior causes distortions: misallocation of capital, excessive risk-taking, and so on. I’ll evaluate this claim. Then I’ll poke at a few of Smithers’ more doubtful claims. I’ll close by praising his critique of macroeconomics.

Corporations maximize their stock price instead of “profits” – OK, maybe

In a book review written for Reuters, Edward Chancellor, himself a formidable commentator on economic and market matters, summed up Smithers’s corporate-profits view as follows:

[Smithers] lifts the corporate veil to reveal a world in which the managers of public companies put their own interests first and seek to maximise current share prices rather fundamental values.2

Not a big surprise. The important question here is whether we have a better estimate of fundamental value than the market does. Corporate insiders might; active portfolio managers think they do, but the track record of active management says they don’t.

Agency theory is the discipline that studies this issue. The theory, first discussed at length by Alfred Marshall (1842-1924), explores the consequences of hiring executives to manage the day-to-day affairs of a corporation that they do not own.3 This “separation of ownership and control” (principal and agent) sets up a wedge between what is best for the corporation (meaning its owners, the shareholders) and what is best for the executives personally.

To minimize that conflict of interest, Michael Jensen, whom we met earlier, recommended paying executive bonuses in stock or options. Fine. Accounting profits (earnings) are not the profits a company should be maximizing; economic profits are, and Jensen’s presumption was that the markets – in setting stock prices – estimate them more accurately than accountants and corporate CFOs do.

Smithers disagrees; let’s see why.

The practice of paying executives in stock can be abused. Companies can boost apparent profits (accounting earnings) by writing off all failed projects in one quarter, called a kitchen-sink quarter, so the losses don’t poison subsequent quarters’ earnings. If such actions fool the market enough to raise the stock price above fair value, executives who are paid in stock or options will benefit at the expense of shareholders. That should not be allowed.

Another abuse is to time stock buybacks to maximize executive stock- or option-based compensation. While this practice may run afoul of insider trading laws, it happens. This, too, hurts shareholders.

These critiques resonate at an emotional level – how dare they? It’s my money! Let’s look a little deeper. If active managers could add alpha by observing and reacting to these abuses, as well as the many other opportunities to take advantage of corporate folly, their success would show up in the data. It doesn’t. According to a 2014 article in the Chicago Booth Review, “Before costs and fees, active managers on average beat their benchmarks by 5 [basis points]. After costs and fees, they underperform the benchmarks by 5 [basis points].”4

Although the debate on whether active management adds value will never end, the study referenced in the Booth article is one of many documenting that stock prices, while never perfectly fair, are fair enough that they measure profit – specifically, the present value of all expected future profits – better than any accounting-based measure available to analysts. Pay executives in stock, and make sure they obey all applicable laws because the economic reward for cheating is so large.

Smithers’ argument that companies maximize stock prices “instead of” profits is unconvincing. They try to maximize stock prices by maximizing profits. They do not always get it right. That is very different from saying that are trying to achieve the wrong goal.

On to Smithers’s more Firesign Theater-like claims.

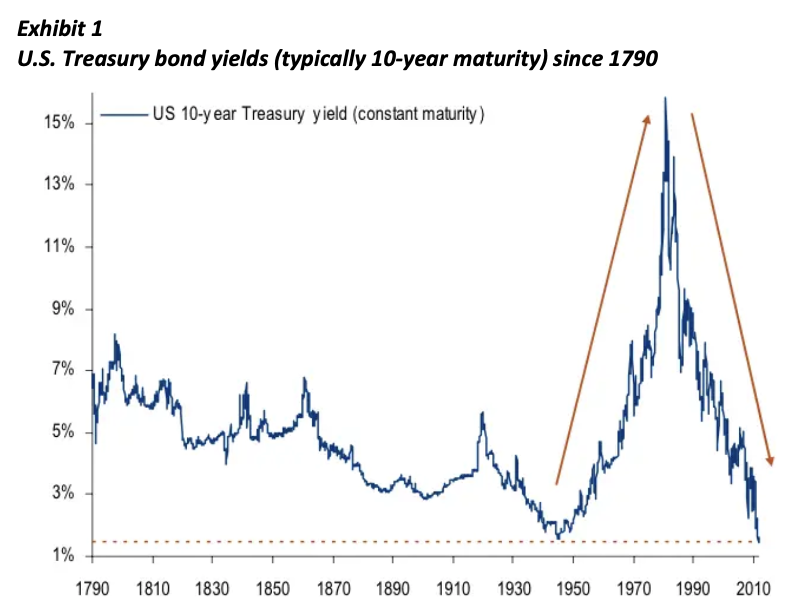

Bond yields fluctuate within narrow ranges – not!

This claim is so silly that every experienced investor will see through it immediately. The 10-year U.S. Treasury bond yield has more than doubled just in the past year!5

Fortunately, he later changed the story to “real yields fluctuate within narrow ranges,” which is more accurate but still wrong.

When you look at the long sweep of history, high volatility in bond yields isn’t even rare. Let’s stick with nominal yields. A hypothetical “consol” bond issued in the distant past (it doesn’t matter when) with a par value of $100 and a coupon rate of 3% would have been worth a measly $20 when long-term-bond yields peaked around 15% in the early 1980s.6 In 2020, when yields reached rock bottom, it would have been worth $303. So much for nominal bonds staying within relatively narrow bounds.

Source: https://www.businessinsider.com/10-year-us-treasury-note-yield-since-1790-2012-6, drawing on Michael Hartnett’s report “The Longest Pictures,” Merrill Lynch Equity Strategy Group, 2012.

Source: https://www.businessinsider.com/10-year-us-treasury-note-yield-since-1790-2012-6, drawing on Michael Hartnett’s report “The Longest Pictures,” Merrill Lynch Equity Strategy Group, 2012.

The volatility of the bond market in Smithers’s home country, the United Kingdom, was even greater:

Source: https://www.businessinsider.com/british-bond-market-1730-2012-6, drawing on Michael Hartnett’s report “The Longest Pictures,” Merrill Lynch Equity Strategy Group, 2012.

Source: https://www.businessinsider.com/british-bond-market-1730-2012-6, drawing on Michael Hartnett’s report “The Longest Pictures,” Merrill Lynch Equity Strategy Group, 2012.

(That little blip around 1776 had to do with some unpleasantness in the colonies. The next, larger blip around 1800 was the Napoleonic War. World War I shows up distinctly, and the much larger mountain after that is the great inflation of, roughly, the 1970s.)

You may say “no fair” to the consol example because almost nobody invests in such long instruments. But Smithers said that yields on both bonds and cash fluctuate within narrow ranges. Cash yields in the United States fluctuated almost exactly as much as long bond yields – from 13.99% in March 1982 to 0.01% in early 2021. Real yields on cash also fluctuated widely, although not nearly as much as nominal yields. Case closed.

Smithers is a distinguished and very senior economist. I hope his claim that “yields” (implying nominal) was just an editing mistake. He knows that bond yields fluctuate, causing great disruption. If it is no more than a typo, he will get an apology; either way, you just got a history lesson.

Do equity returns mean-revert, reducing risk for long-term investors?

A great deal of ink has been spilled on this question. My answer is complex. While equity returns may mean-revert, investors with long holding periods do not face less risk than short-term investors; they may even face more. Let’s explore.

Every market will exhibit apparent mean reversion over some time frame, as long as that market was not destroyed by war or some other force. That doesn’t mean the market is safe and that low returns will be followed by high ones – it means that a market survived because it was safe and low returns were followed by high ones. That’s what survival is. If you can’t know for certain that a market will survive, you should not count on mean reversion.

And some of the world’s most promising markets – Germany, Austria-Hungary, Japan, Russia, China – did in fact fail. Although the U.S. and U.K. would have looked pretty good to a global investor in, say, 1900, so did all those countries that lost a war or suffered a Communist takeover. The fact that some markets later rose out of the ashes and succeeded (I am thinking of China – it’s not clear what will happen to Russia) did not help the 1900 investor, who was wiped out. Those markets did not become safer with longer holding periods!

While the U.S. is a good bet for survival, nothing is guaranteed. We should invest as though risk expands with the holding period – Paul Samuelson said that “time spent recovering from crashes is also time spent waiting for more crashes”7 – and then hope that the opposite happens.

Are equity and bond expected returns co-determined?

This is a toughie, so I saved it for last. “Co-determined” is just econo-nerd talk for “determined by the same underlying factors, so that they move in a somewhat parallel fashion.” If they are not co-determined, there is no direct connection. The latter is what Smithers believes.

The expected return on equities cannot be directly observed, so it must be inferred from other information. There are as many ways of doing this as there are financial economists. With a colleague, I am compiling a book on the subject: Equity Risk Premium Forum 2021, to be published by the CFA Institute Research Foundation.

To say that equity and bond expected returns are co-determined means accepting the Ibbotson and Sinquefield analysis: The expected return on an equity index equals the riskless rate (that is, the yield on Treasury bonds or cash) plus a risk premium for bearing the additional risk of equities as compared with bonds or cash.8 The risk premium may be variable (the currently popular view) or stable.

To say that equity and bond expected returns are not co-determined means that the market arrives at them independently, driven by unrelated processes. In his construct, the stock return (on average over time) is equal to inflation plus 6.7%, a simple process if ever there was one. The bond return, according to Smithers, is determined as follows:

[S]avings and investment are equated by movements in the short-term interest rate and corporate leverage is balanced with the preferences of the owners of financial assets by variation in the bond yield.

Got that? It sounds complicated, but it’s standard Keynesian stuff, taught in school.

Stock and bond expected returns are co-determined

In a proof by contradiction, I now provide evidence that stock and bond returns are inherently related. Real rates wander all over the place, so if equity and bond returns are determined independently then there is an opportunity to make money by market timing.9 When real rates are negative or positive but very low, you borrow to buy equities because they will earn “real 6.7%” at a time when your borrowing rate is “real something-much-less.” When real rates are high, you do the opposite: Sell stocks short or just not buy them.

This strategy “worked” in the recent past. The further real interest rates fell in 2008-2022, the higher the stock market went. When real rates were higher, from about 2000 to 2008, the stock market did poorly (it fell in half, then doubled, then fell in half again).

But, over longer periods of history, the strategy is worthless. Negative real rates in the 1970s would have had you buying stocks, which performed terribly. Large positive real rates in the 1980s would have caused you to avoid the stock market during one of the great bull markets of all time.

We cannot know whether the next period will be like the 1970s and 1980s or like the 2000s and 2010s. You cannot be assured of making money with a real-rate strategy of timing the stock market.

The hypothesis that stock and bond expected returns are independent, or “not co-determined,” is unsupported by the evidence.

Macroeconomics needs a facelift

I promised to point out an area where Smithers’s book is very valuable. It’s in his critique of mainstream macroeconomics. Remarkably, modern macro ignores the financial sector. The financial sector doesn’t exist in... wait for it... dynamic stochastic general equilibrium (DSGE) models of the economy, which are the ones used by most macroeconomists.

Why not? Mostly because it makes the math easier, but there is an underlying view among macroeconomists that financial markets are irrelevant because they are just claims on real economic assets, when only the real economy (of factories and trucks and software and patents and labor contracts) counts. Smithers argues that macroeconomists believe it’s acceptable to omit the financial sector from their models because markets are efficient and prices are fair, causing financial aggregates to cancel each other out; I am not qualified to evaluate that claim.

We don’t need a “new finance” to account for the failures of 2008 and other rocky periods in markets, or for recessions and depressions. We need a new macroeconomics. People at the frontiers of knowledge in the field are working on it. Smithers is not a lone voice crying out in the wilderness.

Conclusion

Smithers has given us a lot to chew on. He proposes a revolution in many fields: corporate finance, security analysis, and macroeconomics, to name just a few. I propose an evolution. Our institutions and theories are not perfect, nor are they ready to be discarded. We advance, Thomas Kuhn reminds us, by making incremental changes in our ways of thinking until overwhelming evidence persuades us that we are barking entirely up the wrong tree. At that point we engage in what Kuhn calls a paradigm shift.

We are not at that point in investment finance or in the microeconomics of firms and their shareholders. We may be in macro. Smithers’s book, difficult and frustrating as it is at times, will spur much valuable discussion about all these issues. That is how we make progress. Thank you, Andrew Smithers, for providing that service.

Laurence B. Siegel is the Gary P. Brinson Director of Research at the CFA Institute Research Foundation, the author of Fewer, Richer, Greener: Prospects for Humanity in an Age of Abundance, and an independent consultant. His latest book, Unknown Knowns: On Economics, Investing, Progress, and Folly, contains many articles previously published in Advisor Perspectives. He may be reached at [email protected]. His website is http://www.larrysiegel.org.

1Siegel, Laurence B. 2014. “Read Your Sharpe and Markowitz.” CFA Institute Magazine (September/October). I confess that, on re-reading my description of the “Read Your Bible” and imaginary “Read Your Darwin” banners in the Scopes Monkey Trial courtroom, I find it very poorly worded. I have re-writing this article on my bucket list.

2https://www.reuters.com/breakingviews/global-markets-breakingviews-2022-04-14/

3See Marshall, Alfred, 1890, Principles of Economics. Adam Smith [1776, Wealth of Nations, bk. V, ch. I, pt. III, art. I] had an inkling of it. Gardiner Means (1931) called it the separation of ownership and control, and this terminology became standard, as did “principal-agent conflict.” Means’s work prefigured extensive research in the second half of the last century by a series of superstars including George Stigler, Eugene Fama, and Michael Jensen. I call it agency theory. Smithers’s book is in this tradition and is a strong contributor to it.

4https://www.chicagobooth.edu/review/why-active-managers-have-trouble-keeping-up-with-the-pack. The study referenced in the article is not just another active management performance study. It is the now-classic study by the Booth-Wharton team of Luboš Pástor, Robert Stambaugh, and Lucian Taylor, “Scale and Skill in Active Management,” published in the Journal of Financial Economics in April 2015. (I’ll note, and then set aside, their implication that fees and costs add up to only 10 basis points; typically they are much larger.) More recent data indicate that average manager alphas have gotten worse, not better.

I owe it to my good friend Ted Aronson, who is himself an active manager and who is co-publishing this article, to note that while the average manager is not very good, the best managers are excellent, adding a lot of value over time. See Siegel, Kroner, and Clifford (2000).

5In fact, it very nearly tripled. Intraday low of 1.127% on August 4, 2021; intraday high of 2.981% on April 20, 2022.

6A consol bond is one that never matures, but pays its initial coupon rate forever. The bond can be sold to another investor. Consol bonds were traded in the U.K. from 1730 to 2014, as Exhibit 2 shows. The data were collected by Michael Hartnett. The word “consol” is short for “consolidated annuity.” In 2014 the bonds were “called,” that is, redeemed whether the investor liked it or not. This did not violate the bond covenant because a call provision was written into the covenant, as it is for many bonds. (You should be skeptical of government promises to do anything forever, but the British government acted pretty responsibly in this episode.)

7Quoted in Siegel, Laurence B. 1997. “Are stocks risky? Two lessons,” Journal of Portfolio Management (Spring).

8Ibbotson and Sinquefield’s analysis begins with the Fisher equation, which defines the real riskless rate, as the nominal short-term (Treasury bill) riskless interest rate, , minus inflation. It is due to Irving Fisher of Yale, the nice man who said that the stock market in 1929 had reached a permanently high plateau. He was a great economist. Really. (See Fisher, Irving. 1907. The Rate of Interest. New York: Macmillan, 1907; Mansfield Centre, CT: Martino Publishing, 2009.) The real expected return on bonds is then plus a horizon premium for bonds over bills; an equity premium for stocks over bonds; and so forth in a building-block manner.

Smithers’ proposition, however, relies on the closely related but not identical Fisher effect, which is not a definition but a testable hypothesis: that nominal interest rates change to follow changes in the inflation rate. In this model of interest-rate determination, the difference, the real interest rate, is exogenous (determined somewhere else in the economy, specifically by the supply and demand for money and other capital). I believe this hypothesis is correct.

9The hedge fund crowd would call this “risk arbitrage.” It is not a real arbitrage.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All