Today’s Speculative Mania

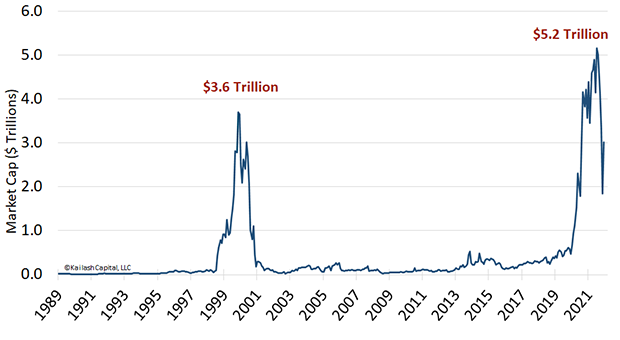

Total Market Cap of Stocks with Price to Sales > 20x

Source: Kailash Capital, LLC and Compustat. The chart above shows that the market cap of firms trading at over 20x sales has hit $4.7 trillion from 4/30/1989 to 3/31/2022. All indices are unmanaged. It is not possible to invest in an index. Past performance does not guarantee future results.

Warren Buffett wasn’t kidding when he said, “nothing sedates rationality like large doses of effortless money.” After a decade in which the Federal Reserve has kept interest rates at historic lows — and near zero — the stock market has been engulfed in a speculative frenzy rivaling the dotcom bubble of the late 1990s.

For those who don’t believe this market is like the tech wreck or other past manias — that “this time it’s different” — consider the following: At the peak of the dotcom bubble, the total market capitalization of companies trading at a price-to-sales ratio of more than 20 reached a record $3.6 trillion. (To put that lofty multiple in perspective, Apple today trades at around seven times sales while General Motors trades at a mere 0.5.) Yet recently, the total market value of stocks trading at more than 20 times sales shattered the dotcom-era record by more than 40% as shown in the chart above.

And while the late ’90s is synonymous with irrational exuberance over profitless companies, the percentage of initial public offerings involving profitless companies recently matched the all-time high set in the dotcom era. That’s not counting the rampant speculation on the 600 or so new special purpose acquisition companies (SPACs) on the market that are raising funds without having to report revenues or earnings. Nor does this account for the mania surrounding the more than 18,000 cryptocurrencies on the market today, which don’t produce a single cent of profits or dividends.

Common sense, thankfully, seems to finally be returning now that the Fed has commenced a new rate-hiking cycle and the “easy money” is going away. Already, there are signs that investors are being mindful of valuations again, with the ongoing resurgence in attractively priced stocks with real earnings, positive cash flows, and solid balance sheets. We believe we are in the early innings of this reawakening, which should start driving investors to small cap stocks. It was Ben Graham who urged investors to “buy not on optimism, but on arithmetic.” And right now, the math is telling us that small stocks are trading at their deepest discounts relative to large-cap stocks since the dotcom era.

© PIMCO

Read more commentaries by PIMCO