When it comes down to it, there are a few key macro variables that are highly correlated with the relative performance of value vs growth – most of them measuring the reflationary impulse in the system in different ways.

Soros’ view on the pattern of bubbles is interesting because it changes the argument from a fundamental view to a technical view. Prices reflect the psychology of the market, creating a feedback loop between the markets and fundamentals.

A major new study based on a somewhat original methodology forecasts that global population will peak well before the end of this century. Although the usual caveats apply, the authors have offered fruitful new ways to grasp crucial policy questions.

As ETFs grow in number and complexity, it’s becoming more difficult and time-consuming for advisors to find the right ones. Discover how to build better ETF-based portfolios using a uniquely forward-looking rating system that helps you easily determine the best ETFs for your clients.

Join Marc Chaikin, Founder of Chaikin Analytics and creator of Chaikin Money Flow, as he walks you through cutting-edge technology that helps advisors make better investing decisions, accelerates the research process, enhances client engagement, and frees up time to grow your AUM.

Advisors will learn how to:

After the presentation Mark will be available to answer questions live.

Non-profit endowments, particularly those of elite academic institutions, have failed to deliver investment outperformance. Those colleges and universities have significantly underperformed a passive benchmark on an absolute and risk-adjusted basis.

To scale your business, you can’t rely on your personality alone to carry you through; you need to intentionally and systematically make sure more of your ideal prospects have the opportunity to get to know, like, and trust you every day.

Some emerging markets have been coping with the COVID-19 crisis better than others, and their economies are in different stages of recovery. Our emerging markets equity team highlights a few—and offers thoughts on why the pandemic has accelerated some existing fundamental and technological trends.

This week I did a complete re-read of Joel Greenblatt’s classic “The Little Book That Beats The Market.” For any of you that are not familiar with the book, Joel Greenblatt presents his magic formula for picking stocks that his research indicated will beat the market most of the time.

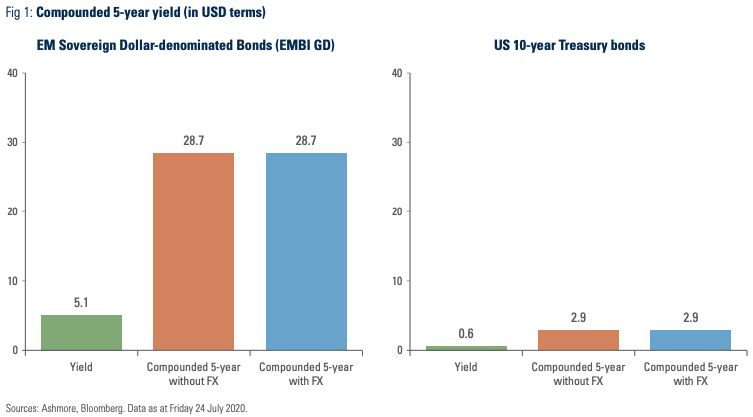

Welcome to the 9th annual review of the Emerging Markets (EM) fixed income asset class. Using new data from the Bank of International Settlements and other sources, we establish that the EM bond market has expanded by 12% in Dollar terms in the past twelve months to a size of USD 29.6trn, or 25% of the global fixed income universe as of the end of 2019.

Americans enjoy the economic prosperity and freedoms of its liberal democracy. But our elevated stature is threatened. As the U.S. recoils from the world, the era of U.S. dominance might be ending.

COVID-19 causes growth in government debt, liability risks, and stress for women.

For the week, airlines stocks increased 9 percent, its best weekly performance since early June. Wheels up!

As I file this letter Friday morning, people are reacting to the July jobs report. My own reaction: The headline report is absurd.

Gold could extend gains as governments and central banks respond to slowing growth with vast amounts of stimulus.

Several months into the Covid-19 era, Howard Marks takes a step back to consider the global health crisis, the economic fallout and the U.S.’s response to date. He also shines light on how one might – or might not – view the current circumstances in the framework of a market cycle.

These days, pretty much everything is hyper-political, including death rates from disease, wearing masks, opening schools, whether some demonstrations are "mostly peaceful" or "violent," and now GDP.

In 1832, Martin Van Buren helped Andrew Jackson decide precisely when he would end the charter for the Second Bank of the United States – the only American central bank of issue before the establishment of the Federal Reserve.

According to a new study by the left-leaning Roosevelt Institute, a universal basic income could permanently make U.S. economy trillions of dollars larger. While such socialistic policies sound great in theory, history, and data, show it isn’t the economic savior it is touted to be.

Record state budget gaps could reignite efforts by officials to reduce pension benefits, raise employee contributions or eliminate traditional pensions altogether.

As an advisor, effectively communicating with your clients is an integral part of maintaining and growing your business. In the current era of working from home and social distancing this task has been even more difficult as many face-to-face interactions have been replaced by phone calls and Zoom meetings.

Two companies in the metals and mining space I’m looking forward to hearing from are Ivanhoe Mines and Franco-Nevada. Both are scheduled to report next week.

Big things have been brewing in Europe. The same continent that two years ago I said was going through “monetary drug withdrawal,” is now set to outpace US growth by a wide margin. And US growth, which had led the world for years, now looks likely to lag it.

About two-thirds of this month’s comment is about COVID-19 and the risk of a second wave. This is not only for the sake of public health, which would be enough, and not only to contribute to a better understanding of the epidemic.

The U.S. dollar has fallen by about 7% against a broad basket of currencies since its mid-March peak. After a nearly decade-long bull market that saw it appreciate by more than 40%, we believe the dollar could be headed for a longer-term decline.

While the economic restart has helped put 7.5 million Americans back to work in May and June combined, payrolls are down more than 14.5 million from their pre-pandemic peak.

A common block I see in business growth is incongruence. What people say they want is not what they actually want (or believe is possible).

Thus far the market has shrugged off the recent rise in Covid cases, but the situation remains fluid. In our view, the best strategy is to invest in companies that are able to grow during this time of stress, either organically or by increasing market share as weaker competitors fall by the wayside.

Does 9 times higher yield in EM than in US bonds make for an attractive investment proposition? We lay out the arguments.

Three subtle biases in the way investors view historical equity returns lead to inappropriately high equity allocations.

Here we are in the dog days of summer, and the hot weather is not the only thing making us a little queasy. The darling stock market group since 2011, the Nasdaq 100 stock index, has soared a cool 20% this year and well into all-time high territory. Indeed, the height is making us queasy from vertigo.

Tesla’s market capitalization just crossed $300 billion. It’s the largest car maker in the world. Tesla’s market cap implies that its production will go up from the 400,000 cars a year it produces today...

I’ve long been a believer that markets are generally efficient (for large cap stocks in the U.S, at least). As such, I’m always skeptical of advisors that peddle their ability to select individual stocks that they claim will beat the market over the long term.

We all know that past performance is no guarantee of future results, but you can see in the chart below that the white metal could possibly be setting up for another epic run-up. At this stage of the bull market, silver’s current price appreciation is ahead of any previous rally.

The U.S. and EU deliberate how to disburse aid, China’s recovery carries risks, and U.S. mortgage rates find a floor.

We’ll start with a dozen or so charts showing the market is either very highly valued, or extremely overvalued, or merely stretched. But in general, you will see markets are indeed at the upper end of historical valuations. Then we’ll consider some reasons why this is so, and why stocks could even go higher.

European measures applied to mitigate the effects of the pandemic have contained the unemployment rate in Europe more than in the U.S. While recognizing economic risks from the rising number of COVID-19 cases in the U.S., our forecast sees this success ratio reversing before the end of the year.

With less than four months to go until Americans cast their votes for president, we’ve fielded an increase in questions from clients as to whether the U.S. presidential election poses a risk to markets and the economy. The short answer is yes.

European governments have agreed to pour money into everything from electric cars to renewable energy and agriculture.

How would Buffett be viewed if, instead of being the chairman of Berkshire Hathaway, he ran an open-end mutual fund by the same name?

It’s the built-in online tool you may have never considered a business advantage: Google My Business. Before you write it off, consider these statistics…

With the US dollar index recently having completed a so called “death cross”, we thought it would be a good opportunity to review the investment implications of a potential trend change in the USD.

Unlike passive investors, who buy at any price, active managers police markets to drive price discovery. But the active police has been defunded.

Automatic stabilizers prevented an economic breakdown, while trains are running empty and money stays parked.

Weeks before the S&P 500 bottomed, many millennial Robinhood investors began picking up coronavirus-impacted airline stocks. The buying spree continued even after Warren Buffett announced that he’d dumped his holdings.

Politicians love saying small businesses are important to the economy. In this case, it isn’t just rhetoric. The millions of little companies with a handful of workers are, collectively, more important than the few hundred large enterprises we see in the news.

China's V-shaped economic recovery continued for a fourth consecutive month in June, led by strong domestic demand. If COVID-19 remains under control, China can remain the world's best consumer story.

U.S. stocks have been fairly resilient lately, even as coronavirus hotspots flare up around the country. Although consumers and businesses are increasingly worried about rolling shutdowns, major stock indexes generally have moved sideways. How long can this continue? Much depends on the shape of the economic recovery.

In the era of social distancing, technology has become even more integrated into our personal and professional lives. We believe this trend will persist even after the pandemic passes, and we expect it will particularly benefit firms that support remote working arrangements and eCommerce, two areas where we anticipate accelerating adoption and sustained growth.

The first wave of the economic recovery has generally exceeded expectations, but the recent surges in COVID-19 cases could deliver a setback.