“I have a friend who has amassed a fortune in excess of $100 million. He taught me two basic lessons. First, if you never bet your lifestyle, from a trading standpoint, nothing bad will ever happen to you. Second, if you know what the worst possible outcome is, it gives you tremendous freedom. The truth is that, while you can't quantify reward, you can quantify risk.”

Larry Hite

Three subtle biases in the way investors view historical equity returns lead to inappropriately high equity allocations.

To understand those biases and their pernicious effect, let’s start by reflecting on how investors typically view risk and return.

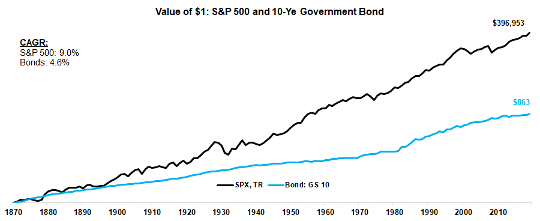

One of the mantras that Wall Street frequently promotes is that for investors with long horizons, equities are the best investment. The data supports that mantra. Figure 1 shows the progression of a dollar invested in the S&P 500 (proxy for equities) and U.S. 10-year government bonds (proxy for the so-called risk-free/safe assets) over the past 150 years. U.S. equities generated an annualized return of 9.0% and bonds 4.6%.

Figure 1: Nominal Value of $1 Invested in S&P 500 and US Govt Bonds Since 1870

Source: Data from Robert Shiller, MAEG’s calculations

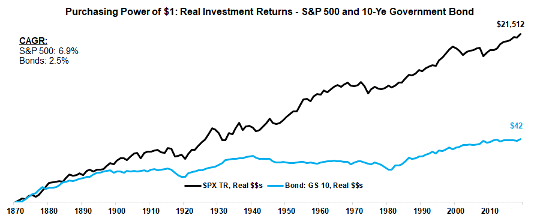

The returns shown above are nominal returns, i.e., they are not adjusted for inflation. However, as investors, our primary concern is with the ability to grow our wealth at inflation-adjusted rates, i.e., real and not nominal rates of return. A rate of return, no matter how high, that is below inflation, will result in a decrease in the purchasing power of the portfolio and thus is equivalent to real wealth destruction. Consider that Venezuelan equities are one of the strongest performing equity markets in 2020, with year-to--date return of 256%1. However, during this period, inflation in the country has averaged at 3,000% annualized2.

Figure 2 shows investment performance of the S&P 500 and U.S. 10-year bonds over the past 150 years adjusted for inflation. As is seen, equities, as evidenced by the S&P 500, have generated extremely healthy inflation-adjusted returns of 6.9%. Indeed, the equity portfolio value as shown by the black line, is extremely steady in its upwards march.

Figure 2: Real Value of $1 Invested in S&P 500 and US Govt Bonds Since 1870

Source: Data from Robert Shiller, MAEG’s calculations

These investment returns are why long-term investors are told to maximize their equity allocations. However, the numbers and charts presented thus far tell us nothing about the risk.

Let’s now turn our attention to the risk of investing in equities.

Risk: Standard deviations and skewness

Usually, when investors, investment advisors, and financial intermediaries evaluate investment strategies, the number that receives the most attention is the investment returns measured over preferred time periods, usually three to five years. As highlighted by Larry Hite’s observation, it is hard to quantify rewards. However, much of the industry focuses its attention on returns and not risk.

When they do talk about risk, it is largely discussed in terms of standard deviations and Sharpe ratios. In plain English, standard deviation is a measurement of the dispersion around the mean. The Sharpe ratio scales the investment return by the standard deviation3. In doing so, the Sharpe ratio purports to measure the excess return earned per unit of risk taken.

All that sounds nice and fancy, except for one minor red herring. Implicit in such risk definition is a rather important and incorrect assumption: investment returns are normally distributed. As is usually the case, real life situations are messier and trickier than academic models. Frequently, financial instruments are associated with asymmetric distributions and are positively or negatively skewed.

Before we proceed, we will make an effort to provide simpler explanations for two statistical terms offered in the last paragraph; normal distribution and skewed distributions. When at the beach, take lots of dry sand and make a sandpile. As you observe the sandpile, you will notice that from its peak, the sandpile spreads on all sides in a symmetrical fashion. That in a nutshell is the normal distribution. Now consider a mountain. While it may have a fairly steady slope leading up to its peak, it may not have the same kind of a slope on its other side. Clearly, you will not want to apply the same kind of trekking mechanism on both sides of this mountain, especially if it happens to have a cliff. The mountain with a cliff or a steeper other side represents the skewed distribution.

Financial investments are usually of the skew variety and can have a positive or a negative skew. There are investment strategies where one risks dollars to win a succession of pennies (negative skew), and there are strategies where one risks pennies to win dollars (positive skew). What is interesting about the two type of investment strategies is that while the second variety appears to be the better risk, it is the first variety that receives much of investor interest.

As is usually the case, this anomaly is driven by our behavioral biases. Our brains prefer situations where there are a greater number of positive reinforcements than the number of negative outcomes. Whereas in financial matters it is the relative size of gains and losses that is important, our brain treats all losses as just that: losses. As negatively skewed distributions are comprised of lesser number of negative occurrences, the tendency to avoid losses then results in a preference for negatively skewed investment strategies.

An important attribute of negatively skewed distributions is that they are associated with a greater number of positive outcomes. However, the negative outcomes, while fewer in number, are significantly larger in their magnitude than is suggested by a normal distribution, i.e., they have fatter tails to the left. This not very different from many real-life situations with asymmetrically large negative risks, e.g., cocaine, smoking, or binge drinking. The addict experiences a greater number of positive outcomes. The negative outcomes, while having a much lower probability of occurring, are of much larger magnitude.

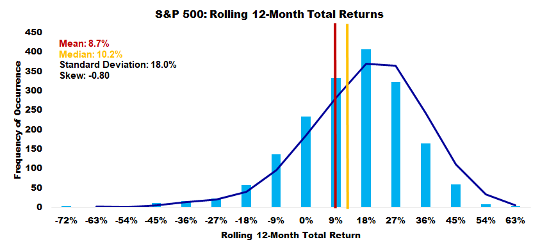

Distribution of total equity returns: Rolling 12-month return over the past 150 years

Figure 3 shows the distribution of rolling 12-month total returns for the S&P 500 over the past 150 years4. As is seen, the distribution has a moderate negatively skewed profile. More than half (54%) of the 12-month returns are greater than the average return with 72% of the periods registering positive returns. In keeping with the profile of negatively skewed distributions, just about 2% of occurrences result in a large negative outcome of -40% or worse.

Figure 3: Distribution of rolling 12-Month Equity Returns Since 1870

Source: Data from Robert Shiller, MAEG’s calculations

If the distribution of equity returns was normal, i.e., if standard deviation was an accurate definition of risk for investment portfolios, only about 0.34%5 of those observation would have been -40% or worse as against nearly 2% of them.

Is it different this time? The perennial question

Every period of a lasting bull market gives rise to the idea that it is different this time. The reason why we end up with this idea in each cycle is driven by another attribute of skewed distributions – it takes considerably longer to appropriately assess the true properties of a skewed distribution than is the case with a normal distribution6. With only about 2% of the returns associated with extremely negative outcomes, equities can have extended time periods during which the risk embedded in the distribution is not revealed.

Whenever you hear the assertion that it is different this time or that equities have reached a permanently high plateau, ask yourself whether the lookback period was long enough to allow for an appropriate assessment of the true properties of a distribution that is likely negatively skewed.

Bill Gross and the man in the mirror

One of the most important investment readings, and one that we will point to anyone with the slightest interest in understanding investment returns and investment gurus, was penned by Bill Gross7. As Gross pointed out, even the best of the track records including his own and that of legends like Buffett and Soros, shaped up during the most attractive of the time periods – an epoch that has been continuing for 40--plus years. As he stated, “Perhaps, however, it was the epoch that made the man as opposed to the man that made the epoch.” Such is the impact of negatively skewed distributions – a trend, no matter how irrational, can continue for far longer than the statistician will surmise.

US equity returns as the proxy for equity returns: A biased view – Looking forward in history

The analysis thus far was based on U.S. equity markets. We used U.S. equities as the proxy for equity returns. Indeed, much of the investment industry bases their investment return expectations and allocations on the past U.S. equity returns.

However, when we use past U.S. equity returns for estimating prospective returns, be it for domestic U.S. or international investors, we are engaging in an activity that requires perfect foresight. Such an analysis, if it can be called that, assumes that investors in the past had knowledge of the outsized strong performance that the U.S. economy and its financial markets were going to enjoy over the next century.

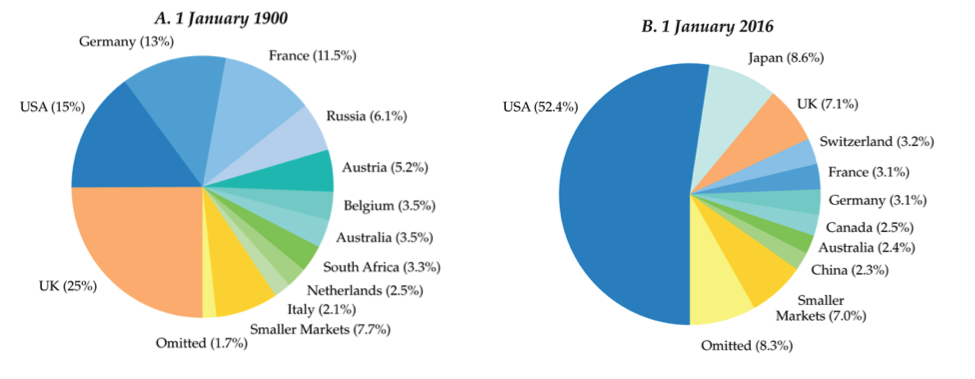

Consider that in the year 1900, the largest equity market globally, was that of the UK; a market that is now relegated to a far distant third position. On the other hand, the U.S. equity market accounted for about 15% of the global equity capitalization at that time. As of January 2016, driven by the superior performance of its financial markets, the U.S. equity market accounted for greater than 50% of the global equity capitalization.

Figure 4: Relative sizes of word equity markets, 1900 vs 2016

Source: Financial Market History, Reflections on the Past for Investors Today, 2016

Of the financial markets on which we had data at the start of the last century, at least two of those markets, Russia and China, resulted in a complete loss for equity investors whereas Austria saw catastrophic losses for investors. Basing expectations on the performance of U.S. equities makes an implicit assumption that investors in the year 1900 had the foresight that the U.S. will be one of the best performing equity markets globally. If only it was that easy to make the correct assessment for the next 100 years!Source: Financial Market History, Reflections on the Past for Investors Today, 2016

Summary

Three important points drive a realistic assessment of investment risk and returns. The equity market return that the average investor realized was lower than is evidenced by U.S. equity returns8. The average equity investor likely experienced higher volatility than is evidenced by U.S. equity return volatility. And, lastly, the distribution of equity returns was likely even more negatively skewed than is seen in Figure 3, an assertion that is supported by complete losses in Russian and Chinese equities.

When appropriately accounted for, these factors call for much lower equity allocations than is suggested by the standard mean-variance optimization tools.

Baijnath Ramraika, CFA, is a cofounder and the CEO & CIO of Multi-Act Equiglobe (MAEG) Limited and is the Executive Director at Sapphire Capital. As a portfolio manager, he manages the Global Moats Fund, the Global Select Value Fund, and the India Moats Fund. Contact him at [email protected]. Baijnath’s thoughts and ideas can be read at his blog at www.symantaka.com

Prashant K. Trivedi, CFA, is a cofounder of MAEG and the founder and chairman of Multi-Act Trade and Investments Pvt. Ltd.

MAEG is an investment manager and manages the Global Moats Fund, an investment fund that invests in a global portfolio of high-quality businesses with sustainable competitive advantages.

Sapphire is an investment manager and manages the India Moats Fund, an investment fund that invests in a portfolio of Indian high-quality businesses with sustainable competitive advantages.

1 As of June 30, 2020. Source: https://tradingeconomics.com/venezuela/stock-market

2 Source: https://tradingeconomics.com/venezuela/inflation-cpi

3 Usually, the risk free rate of return is reduced from the return of the strategy with only the excess return divided by the standard deviation.

4 Logarithmic returns.

5 http://onlinestatbook.com/2/calculators/normal.html - supply a mean of 8.7, standard deviation of 18.0, and choose below -40 to see the probability of such outcomes.

6 Sometimes you will hear that if we have 30 observations or more, if we have a reasonable sample size. For one, there is nothing magical about that number 30 so such generic advice should at best be ignored. However, when applied to distributions like investment returns, it may prove to be grossly inadequate.

7 A Man in the Mirror, Bill Gross, PIMCO, Investment Outlook April 2013

8 We will address global equity market returns in a follow up article. For our purposes here, the fact that the US equities went from 15% to 50%+ of global equity capitalization is evidence that global equity returns were lower than that of the US.

Read more articles by Baijnath Ramraika, Prashant K. Trivedi