Want to read more by Ashmore Group? Visit their Featured Firm page here

Does 9 times higher yield in EM than in US bonds make for an attractive investment proposition? The Weekly lays out the arguments. The Mexican government puts forward a market-friendly pension reform proposal. Hungary lands a few new swap lines. Hong Kong launches a new tech index. Brazil spends more on education as inflation continues to surprise to the downside.

Emerging Markets

There is plenty of speculation about how coronavirus may change the world permanently, and it may well do so, but the pandemic is unlikely to have anything other than a transitory impact on markets. Coronavirus will be priced in to markets as a new fact of life, if not immediately then gradually, perhaps in fits and starts, until, finally, it ceases to move markets. On this view, it is clear the Emerging Markets (EM) bond, stock, and currency markets over-reacted in March. March, as it turned out, was the bottom and EM markets have rallied ever since. As of this morning, EM currencies are 8.0% up versus the Dollar since late March, while the EM broad sovereign and corporate bond indices have now both moved in to positive territory for the year (0.1% and 1.6%, respectively). EM equities have recovered about 40% since March. In short, the 2020 ‘Triple Shock’ – health, commodities, and financial conditions – looks more and more like a conventional buying opportunity for EM assets, just as nearly every other global shock has done over the past couple of decades.1

Still, EM bond yields appear unusually high compared to yields in developed markets (DMs) despite the months-long rally. The unusual yield differential between EM and DM bonds likely reflects lingering uncertainties about how the pandemic will evolve, fears of continuing economic weakness in many parts of the world, and the escalation of America’s witch hunt against China in the run-up to November’s presidential election.2 It seems reasonable to expect markets to continue to experience volatility going forward, given less than confidenceinspiring fundamental economic and political circumstances.

However, the act of investing is not something that only happens during periods of calm and tranquillity. Indeed, without volatility there would be no reward for investing at all as the future would be known with certainty. Investment decisions boil down to a simple question of whether investors are being compensated adequately for risk and in principle there is a level of expected return, which justifies investing at almost any level of risk.

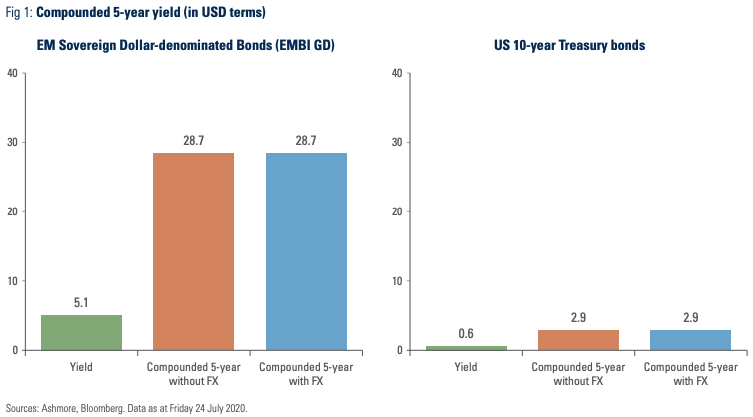

As Figure 1 illustrates, investors are currently being paid 9 times higher yield for an EM sovereign Dollar-denominated bond than for the US 10 year bond, which has roughly the same duration. Specifically, assuming that yields ‘freeze’ at current levels the compounded yield for EM sovereign external debt will be 28.7% over the next five years compared to just 2.9% for holders of the US 10-year bond over the same period.

Is a 9 times higher yield (in USD terms) adequate compensation for switching from US bonds to EM bonds? Clearly, the answer to this question is partly subjective as some investors will always feel that investing in EM is too risky, while others will always view EM as a good risk-reward. However, the majority of investors will hopefully look at facts to help them make up their minds. What, then, do the facts reveal about the risk-reward for EM bonds today compared to US bonds?

First, it is likely that the return on EM bonds will be greater than that implied by the yield differential due to the current elevated level of spreads. Risk appetite usually normalises gradually after major risk-off episodes. If, as can be expected, the same happens after the coronavirus shock, then EM sovereign debt spreads should tighten significantly from their current elevated levels. When spreads return to the pre-coronavirus level of 300bps from 452bps today then EM sovereign bonds should benefit from at least another 6% return over and above the yield, taking in to account the gradual decline in yields.3 At the same time – and for the same reasons – the US bond yield should rise as so-called ‘safe haven’ demand wanes. If, say, the yield on the US 10-year bond returns to where it was at the start of 2020 then investors would suffer a one-off capital loss of about 10%, given the duration of the bond.

Second, the fundamental outlook in EM and DM is different. Consider EM fundamentals first. Financial conditions are now steadily improving across the EM universe as markets slowly normalise. Asian data is also pointing to a decent economic upswing.4 The recovery from the pandemic is generally moving from East to West, so Eastern Europe is likely to be the next major EM region to recover with Latin America after that. Strong economic data is already beginning to emerge in some EMEA countries, such as Poland. For EM as a whole, the IMF forecasts less than half the contraction in growth in 2020 in EM compared to DM (-3% versus -8%, respectively). This makes sense. After all, EM countries have five times fewer coronavirus-related deaths per million of population than DMs due to younger populations and greater social distancing on account of larger rural populations and smaller services sectors. EM’s large informal sectors and low per capita income also mean that lockdowns are far less effective and hence less economically damaging. The IMF also expects EM economies to grow faster than DMs in 2021, despite the deeper trough in the latter in 2020.

EM’s growth outperformance relative to DMs is likely to become even more pronounced beyond 2021, when the broad business cycle dynamics, which prevailed in DMs and EMs prior to the coronavirus outbreak, are likely to resume. Prior to the pandemic, many EM countries were just coming out of a long economic downturn, while many DMs were approaching the end of their long cyclical recoveries, aided by Quantitative Easing (QE). The National Bureau of Economic Research, whose task it is to monitor business cycles, established that the US economy already went in to recession in February, that is, before the US began to take measures to control the coronavirus pandemic. Due to these contrasting business cycle dynamics, growth is likely to be skewed strongly in favour of EM in the 2022-2025 period. In fact, based on IMF data, EMs should contribute nearly 85% of all global growth by 2025 with about one third of all growth coming from China alone and about half of global growth emanating from non-China EM.

Third, investors must take account of the resiliency to shocks. So far, EM has only experienced a small number of defaults, despite the enormous global financial and economic shock. The small number of EM sovereigns to buckle have done so mostly due to weaknesses that were already present prior to the coronavirus outbreak. Indeed, so far only Ecuador’s restructuring can be directly attributed to the coronavirus outbreak itself. Meanwhile, in the EM corporate high yield space default rates remain below the long-term averages in all regions of EM, and, in fact, as noted above, EM corporates have outperformed sovereigns so far in this crisis.

Fourth, investors should examine financial conditions. Due to the general state of under-financing in EM, financial stress can have serious implications for fundamentals in EM and hence the case for investing. Remarkably, this crisis stands out from previous crises due to a near-complete absence of financial stress in EM local markets. This is critically important, because EM governments and corporates obtain more than 80% of their total financing from local markets. In March, the yield on EM external debt spiked from 4.7% to 8.0%, but the yield in local bond markets only rose, briefly, from 4.7% to 6.1%. The greater drawdown in external debt, even if temporary, illustrates two important points about financial conditions in EM right now. First, the greater spike in yields in external debt compared to local currency in March suggests that much of the selling was done by myopic and panicky foreign investors, who are disproportionately larger holders of external debt. Second, local institutional investors – which in many cases have information advantages about local conditions compared to foreign investors – did not panic. Indeed, they bought local bonds to the point, where EM local bond yields are today sitting at their all-time low of 4.4%. This drop in local bond yields enabled EM governments to run counter-cyclical monetary and fiscal policies to soften the impact of the coronavirus pandemic on their economies. A number of EM central banks even intervened in bond markets to stabilise curves, a kind of QE.5 If EM local bond markets now behave much like developed bond markets then why should EM local bond markets be treated differently?

As an aside, like external debt, EM local bonds still pay investors generously, despite the new low in yields. The yoy rate of index-weighted CPI inflation stands at just 2.3% in EM countries, which means that the real yield on a typical 5-year investment grade government bond in EM today is about 2.1%. This compares extremely favourably to the real yield on a US 5-year government bond of about -0.9%, implying a real yield pick-up of 3.2% (and an even greater pick up against even lower yielding European bonds). With the Fed funds rate now at zero, the negative carry of shorting the Dollar is also low.

Fifth, investors needs to bear in mind that the EM bond universe is rapidly becoming more diversified. In the year 2000, there were just 25 bond markets formally represented in the main EM fixed income benchmarks. Today, that number is nearly 10 times larger at 202 markets. This enormous increase in diversification means that the exposure to any individual markets is now far smaller, so when credit defaults occur they tend to inflict far less damage than, say, twenty years ago.

Finally, investors should consider the global backdrop. Here, the US outlook is particularly important due to the special importance of the US Treasury market to EM external debt and the importance of the Dollar for investors in local markets.6 The primary objective of US monetary policy has changed almost beyond recognition over the past two decades. From pursuing a near-laissez faire approach to financial markets under Fed Chairman Alan Greenspan, the Fed’s primary purpose today seems to be geared almost exclusively at preventing asset prices from falling. This shift began when former Fed Chairman Ben Bernanke introduced large scale asset purchases (QE) as bootstraps to lift the real economy out of the doldrums. Sadly, although fundamentals improved for a time they never caught up with asset prices and have since worsened again. This has precipitated a situation today, where asset prices are sitting well above where they ought to be, based solely on economic fundamentals. Indeed, if the Fed were to allow asset prices to return to fair value today there would be massive financial losses and associated negative wealth effects. In the face of renewed economic weakness, central banks, already long government bonds, are now extending their purchases of financial assets to an ever wider range of instruments, including mortgages, investment grade corporate bonds, high yield corporate bonds, and even equities.

In our view, this is a Ponzi scheme, but one that may not collapse immediately, because central banks can keep it alive by drawing upon an infinite lifeline of money printing. The long-term implications of the ever-expanding role of central banks are very negative, however. They include the slow death of markets as central banks insert more and more wedges between valuations and fundamentals in more and more markets. Developed economies are, in effect, drifting slowly towards some version state planning, wherein all key macroeconomic variables are centrally controlled by one government agency or another rather than by markets.7

This worrisome global backdrop has three clear implications for EM:

First, since the direction of travel in DMs is neither healthy nor sustainable it is likely that investor anxiety is likely to remain elevated. All else even, this should (irrationally) slow the flow of capital from DMs to EMs.

Second, there is very little likelihood of significant monetary tightening any time soon. In fact, more monetary easing in DMs seems far more likely. Since EM Dollar bonds trade as a spread over the US Treasury curve, it follows that if US rates are not going up anywhere soon then one of the most important sources of risk for EM investors is diminishing, justifying lower EM yields, particularly since EM bond yields currently appear to price in far higher policy rates in DMs.

Third, the Dollar is likely to decline. Foreign investors put USD 10trn in to bull market trades in the US, including stocks, high yield credit and leveraged loans over the past decade. In a gradually weakening economic environment, they will gradually take profits on these trades and repatriate funds, especially since bear market trades, such as going long US Treasuries, do not offer much in the way of return. The policy issue arising from foreign selling is that it would also lead to crashes in stock and credit markets. The way to prevent this from happening is that a new domestic buyer steps in to pick up the paper coming out of foreign hands. The only buyer with sufficient firepower to do this is the Fed. Of course, the Fed is already doing this, but investors should expect the Fed to become far more active in the coming years. The Fed action to prevent a collapse in domestic US asset prices increases the odds that the decline of the Dollar will be relatively gradual, assuming that the Fed does not commit a massive mistake (which would not be unprecedented).

The global backdrop of elevated risk aversion, low rates, and a declining Dollar should be fairly bullish for most EM asset classes. Money likes to move to where currencies are going up, so a lower Dollar should imply greater inflows to EM local markets. Given the tight financing constraints in EM, this should ease financial conditions and generate a pickup in domestic demand (70-80% of GDP in most EM countries). The recovery in domestic demand should in turn support company earnings and give a boost to EM equities. Currency upside is also supportive for local bonds in the initial stages, but in the latter stages of the cyclical upswing in EM one should expect inflation risks to rise, wherefore EM equities ought to outperform EM local bonds over the medium term.

Given all these considerations, we believe that EM bonds, which today look to pay at least nine times more yield than DM bonds over the next five years, offer a very good risk-reward proposition. The yield differential – and even greater return differential due to capital gains – is particularly attractive, since fundamentals also favour EM. EM will see stronger growth in the near-term as well as over the medium term. With zero stress in key local markets and only a very small chance of Fed hikes anytime soon there is little risk of crippling financial shocks, other than the usual brief ebbs and flows of risk appetite among fickle investors. The picture gets even more interesting when one adds the prospect of a weakening Dollar, which would imply further financial easing in EM.

• Mexico: President Andres Manuel Lopez Obrador (‘AMLO’) has submitted a pension reform to parliament for approval. Unlike the recent pension reforms in Peru and Chile, AMLO’s reform is economically sound. The main purpose of the reform is to close the gap between pension income and wage income at the point of retirement. This will be achieved through greater contributions from the private sector. Workers and the government will not contribute more. The private sector is in support of the reform, which places the pension system on a sounder footing and reduces the pressure for the type of destructive reforms seen in Peru and Chile. The Mexican pension system is a defined contribution system. AMLO has so far defied expectations that he would be extremely populist. He has run a tight fiscal ship and this pension reform is the most ambitious reform in decades. In other news, mid-July core inflation was higher than expected at 0.36% mom versus the Bloomberg consensus of 0.33% mom. The Mexican economy, always sensitive to condition in the US, soften further in the month of May, when economic activity declined 2.6% versus -1.4% expected.

• Hungary: The National Bank of Hungary bought some insurance, just in case. It established swap lines with ECB along with other central banks. The ECB swap line of EUR 4bn is in addition to swap lines from BIS (EUR 2bn), China (EUR 2.5bn), and Fed (USD 2bn), which collectively increase NBH’s firepower by about 25%. Hungary’s FX reserves stand at EUR 30bn. Hungary’s EUR-denominated debt stock is about EUR 40bn. NBH also cut the main policy rate by 15bps 0.75%.

• China: The Hang Seng Tech Index launches today. The index, which is the Hong Kong equivalent of the Nasdaq index style, will track the 30 largest technology companies by market cap. The index will have 80% exposure to China compared to 55% for the conventional Hang Seng Index and 10% for Nasdaq. In economic news, industrial profit growth accelerate to a yoy rate of 11.5% in June after expanding at a 6% yoy pace in May.

• Brazil: The Lower House approved additional spending to education. The permanent spending increase will increase the fiscal deficit modestly. The government also submitted a tax reform, which increases tax efficiency by replacing two inefficient corporate taxes with one efficient value-added style tax. Mid-July CPI inflation was 0.30% mom versus 0.52% mom expected. This means that the yoy rate of inflation in Brazil is running at just 2.13%.

Snippets:

• Argentina: The monthly GDP proxy, EMAE, indicated that economic activity increased by 10% in May following a 17% mom decline in April. The fiscal deficit was 3.1% of GDP in H1 2020.

• Bolivia: The election authority postponed the presidential election to 18 October due to the coronavirus outbreak with a second round to be held on 29 November if no candidate wins in the first round.

• Chile: The Senate approved the bill to enable pension withdrawals, but introduced an amendment to the timeframe for withdrawal.

• Colombia: Business and retail confidence improved in June. The Constitutional Court ruled that a government decision to reduce pension contributions in order to support the economy during the coronavirus outbreak is illegal.

• Ethiopia: The Ethiopian government said that Ethiopia, Egypt, and Sudan have reached a common understanding to pave the way for de-escalation of tensions over a large Ethiopian dam project.

• Malaysia: Consumer prices went up 1% in June, taking the yoy rate to -1.9% versus -1.8% yoy expected.

• Nigeria: The Central Bank of Nigeria left the policy rate unchanged at 12.5%.

• Poland: On a yoy basis, retail sales declined 1.3% compared to market expectations of -3.0% yoy and last month’s print of -7.7% yoy.

• Russia: In seasonally adjusted terms, retail sales were up 15.2% in the month of June. Retail sales were down 7.7% on a yoy basis in June compared to -19.2% yoy in May and -23.2% yoy in April. The June yoy number was better than expected (-11% yoy). The central bank cut the benchmark interest rate by 25bps to 4.25%.

• Singapore: Industrial production (IP) increased by a modest 0.2% in the month of June. Core CPI inflation was 0% in June, leaving the yoy rate of core CPI inflation at -0.2%.

• South Africa: The South African Reserve Bank cut the repo rate by 25bps to 3.5%.

• South Korea: Q2 2020 GDP growth was -3.3 qoq versus the Bloomberg forecast of -2.4% qoq. Growth was also negative in Q1 2020, so South Korea is now formally in recession.

• Sri Lanka: The Reserve Bank of India extended a USD 400m currency swap facility to the Central Bank of Sri Lanka.

• Taiwan: Industrial production and export orders grew faster on a yoy basis in June than expected at 7.3% yoy and 6.5% yoy, respectively.

• Thailand: The trade surplus narrowed to USD1.6bn in June from USD2.4bn in May and April.

• Turkey: The Central Bank of Turkey left the policy rate unchanged at 8.25%.

• Ukraine: The National Bank of Ukraine left the policy rate unchanged at 6.0%.

Global backdrop

The US is good at ‘private sector’ and Europe is good at ‘government’. In normal states of the world, this admittedly simplistic statement goes a long way towards explaining why the US grows and innovates faster, while Europe tends to lag behind somewhat. However, in periods of crisis, where strong centralised government action is required, such as during a coronavirus outbreak, Europe shines. The coronavirus pandemic has exposed major failings in the US government in terms of its ability to contain the crisis, not dissimilar to the failing exposed at a much smaller level following Hurricane Katrina in August 2005. However, Europe has also started to look better than the US in other areas recently. With the approval of a large fiscal stimulus, the European Union (EU) has finally embarked on the path towards fiscal federalism. The EU itself will for the first time become a major issuer of bonds. Over time, EU bonds will slowly displace individual nation state bonds markets to create a truly enormous and hyper liquid bond markets to challenge the US Treasury market. European economic data is also looking better, consistent with the view that the recovery from the pandemic comes from East and moves West. Euro area composite PMI improved by 7.3 points to 54.8, which is a 25-month high.

By contrast, the news out of the US is less than stellar. The most important data release last week was initial claims, which went up to 1.4m claimants from 1.3m claimants last week. This is the clearest indication yet that the mishandling of the coronavirus outbreak (there are now more than four million cases) is now going to inflict renewed damage on America’s already struggling economy. Manufacturing activity picked up a bit, but services was weak. Leaders of Congress also pushed back against prospect of an imminent new fiscal stimulus bill due to big differences between Republicans and Democrats. Enhanced unemployment benefits expire at the end of July.

To make matters worse, President Donald Trump’s weak poll numbers means that he needs a scapegoat for America’s woes, so he has now ordered an escalation in attacks on China. That is why Secretary of State Mike Pompeo is on a European whistle stop tour to try to drum up support for a Trumpian “them versus us” narrative with calls for an “alliance of democracies” against Chinese “designs on hegemony”. The US is clearly trying to force other countries to choose between US and China. This is obviously a false choice, which many countries will wisely stay well clear of, except, of course, the UK. US-China tensions were also ramped up by the closure of China’s Houston consulate, which triggered, soon afterwards, a Chinese demand that US closes its Chengu consulate. Our view is that US-China relations will get so ugly that, once the election is out of the way and the need for an external scapegoat diminishes there will be political mileage in the next US Administration reaching out to China to mend fences. For now, however, US tech stocks have responded negatively to the worsening mood, while Intel, a large US chip producer, signalled last week that it may stop producing chips, potentially ceding this critical activity to Asian firms.

Benchmark performance

1 Ashmore argued that the Triple Shock would prove a buying opportunity as early as 28 February 2020 – see: ‘It is here again - the VIX spike!’, Market Commentary, 28 February 2020.

2 See: ‘The China Witch Hunt’, The Emerging View, 10 June 2020.

3 Valuations as at Friday 24 July 2020.

4 See: ‘Strong support for the ‘First-in, First-out’ thesis in Asia’, Weekly investor research, 20 July 2020.

5 In contrast to QE in DMs, EM QE interventions are mainly aimed at countering temporary irrational volatility rather than artificially propping up overvalued assets.

6 Most EM external debt trades as a spread over Treasuries and most liquid EM currency crosses are versus the Dollar.

7 See: ‘When market valuations become too high to fall’, Market Commentary, 2 June 2020, and ‘Macroeconomic control regimes’, Market Commentary, 15 May 2020.

No part of this article may be reproduced in any form, or referred to in any other publication, without the written permission of Ashmore Investment Management Limited © 2020.

Important information: This document is issued by Ashmore Investment Management Limited (Ashmore), which is authorised and regulated by the Financial Conduct Authority. The information and any opinions contained in this document have been compiled in good faith, but no representation or warranty, express or implied, is made as to accuracy, completeness or correctness. Save to the extent (if any) that exclusion of liability is prohibited by any applicable law or regulation, Ashmore, its officers, employees, representatives and agents expressly advise that they shall not be liable in any respect whatsoever for any loss or damage, whether direct, indirect, consequential or otherwise however arising (whether in negligence or otherwise) out of or in connection with the contents of or any omissions from this document. Past performance is not a reliable indicator of future results. This document does not constitute and may not be relied upon as constituting any form of investment advice and prospective investors are advised to ensure that they obtain appropriate independent professional advice before making any investment.