U.S. equities are mixed as investors await this week’s highly anticipated September inflation data.

It is as though the finance world decided to take a page out of the music industry's book by recycling a melody with only slight variations.

Everywhere you turn, the biggest players in the $23.7 trillion US Treasuries market are in retreat.

“Market instability” remains the most significant risk to central banks globally.

The worst may be behind gold mining stocks. Since hitting a 52-week low on September 26, they’ve risen about 18% and today notched their second straight week of positive gains.

Today I want to talk about why the labor market is so out of balance. Some of this is new and some has been brewing for many years. We will end with some commentary on yesterday’s unemployment report.

Review the latest Weekly Headings by CIO Larry Adam.

October will test the Fed’s resolve.

US employers continued to hire at a solid pace last month and the jobless rate unexpectedly returned to a historic low, indicating a sturdy labor market that puts the inflation-focused Federal Reserve on course for another outsize interest-rate hike.

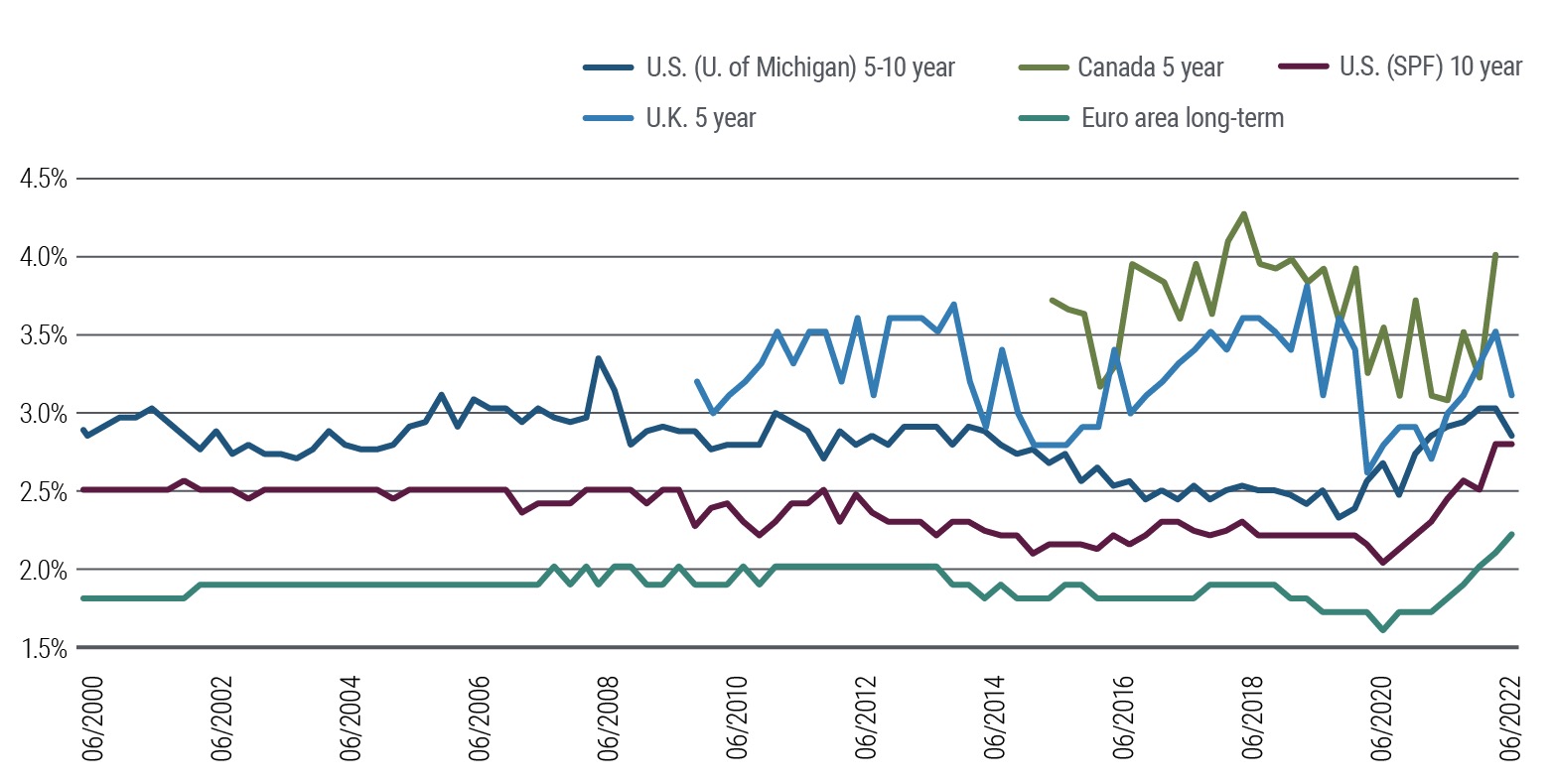

One of the themes I’ve discussed in recent months is the disconnect between a 40 year high in inflation and the lack of experience money managers have in understanding the monetary policy required to deal with such high inflation, including managers with 25 to 30 years of experience

Dip buyers wagering that the era of central-bank hawkishness has peaked got a reminder Wednesday that they are playing a dangerous game.

The firestorm among UK pension funds is a wake-up call for their peers across the Atlantic. The end of an era of cheap money is exposing an industry that’s chronically underfunded and overexposed to market turbulence.

We are in the middle of a giant short squeeze, and it is going to get even bigger.

If one is watching CNBC to figure out where markets are headed, they will be better served looking to the bond market for direction.

U.S. stocks are trading modestly lower in pre-market action with the markets awaiting tomorrow's key September nonfarm payroll report.

A $200 billion corner of the hedge funds industry dominated by computer-driven algorithms has been making the most of wild swings in global markets, putting many of those funds on course for a record year of gains.

Bonds are typically considered safe investments. However, there were decades of negative real returns. Drawdowns reached 50% for U.S. Treasuries and Bonds.

Stocks extend yesterday’s gains as rates continue to ease.

As billions of fans eagerly await the 2022 World Cup, CIO Larry Adam draws parallels between the globe’s most popular sport and the current investing environment.

The list of assets that have risen year-to-date is both short and odd: energy, broad commodity indexes and the dollar.

Every year, Northern Trust Asset Management issues a multi-asset class, five-year investment outlook known as its Capital Market Assumptions Report. Per the recently released 2023 edition, Northern Trust is expecting market returns to be slightly below long-term historical averages. While they believe lower stock valuations may provide some support, upside will be limited by higher interest rates. They see a somewhat similar dynamic playing out with bonds, where returns will be supported by higher yields that will be capped by flatter global yield curves. Among the six investment themes they’ve identified as driving markets over the next five years are Slow Growth Transitions, which looks at such slow transitions across the globe as pandemic to endemic; globalization to regionalization; and fossil fuels to renewables. Here today to discuss CMA’s themes and forecasts is Chris Shipley.

This is a critical time for investors and policymakers alike.

This year's brutal market has investors across asset classes and international markets running for the exits. But where there’s panic and wreckage, there’s also arbitrage and opportunity.

Global bonds and stocks are rallying on hopes that the latest signs of weakness in the US economy will push the Federal Reserve to rethink the aggressive monetary policy tightening that some fear will trigger a recession.

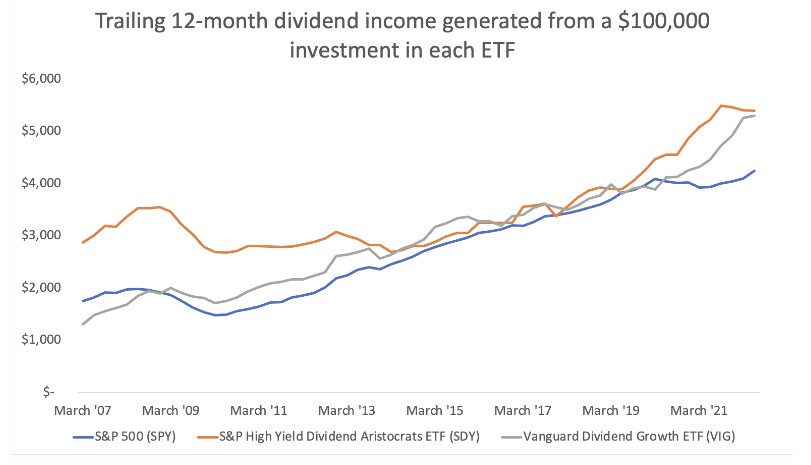

One investment with the ability to provide current income, inflation protection, and even the potential for capital appreciation has been largely overlooked – rising dividend stocks.

It’s thus troubling that the Treasury market has faltered at critical moments, raising fears of further disruptions as central banks end a long period of easy money.

Gold climbed higher, helped by a continued decline in Treasury yields, as traders weighed concerns that central banks’ monetary tightening will lead to recession and the possibility that bond rates may have reached a peak.

We have a long and proud history of investing thematically and believe you can remove a great deal of volatility in your portfolio, if you do so.

For most of 2022, the VIX been above its average, which historically has led to lower equity returns. I will review the risks that investors face, which explain the continued high level of uncertainty.

Unwavering profit projections. Benign chart patterns. Big hedges in the options market. All the things that bulls expected to put a brake on the worst equity selloff in 30 months have just summarily failed.

Just 18.5% of homes in Florida counties that were told to evacuate have coverage through the National Flood Insurance Program (NFIP), which is administered by FEMA. Most regular homeowners’ insurance policies don’t cover flood damage, which is why Congress created the NFIP in 1968. But at an average cost of $995 a year, according to Forbes, the insurance may be out of reach to many households.

Senior Sovereign Analyst Jon Levy looks at this week’s rate and currency shocks in the UK and shares what he believes is a root of the problem.

U.K. financial market volatility is likely to remain high, and the longer-term outlook likely depends on future monetary and fiscal policy.

Surveying the current condition of the financial markets, we presently observe a combination of still historically-extreme valuations, rising yet still only normalizing interest rates, measurably inadequate risk-premiums in both equities and bonds, and ragged, unfavorable market internals, suggesting continued risk-aversion among investors.

The massive debt levels provide the single most significant risk and challenge to the Federal Reserve. It is also why the Fed is desperate to return inflation to low levels, even if it means weaker economic growth.

A number of key technical, sentiment and flow based indicators are suggesting we could see a relief in selling pressure over the coming weeks, and perhaps a countertrend rally in risk assets.

Over the last few months, the Federal Reserve (Fed) has changed its angle of attack quite dramatically, in an attempt to battle surprisingly and stubbornly high inflation.

“Gold is no longer a safe haven.” “Gold isn’t an effective hedge against inflation.” “Gold is dead.”

In a year of volatile markets, the humble I bond has emerged as an unlikely star. Now, there’s a new way to buy them.

This week’s bond meltdown has sent the mean 10-year borrowing cost for Group of Seven countries to its highest in more than a decade, with the average yield surging above 3%. What happens next could set the tone for financial markets and the global economy for years to come.

In the midst of a historically rough year in the $4 trillion municipal bond market, investment managers see ample opportunity as surging yields provide a compelling entry point.

U.S. equities are higher in afternoon action following a recent plunge to lows not seen since 2020.

In the 1980s there was a famous TV ad for Wendy’s with the tagline “Where’s the beef?”.

If a long, ugly recession is in fact going to happen later this year, many investors will want to shift some additional money into cash. There’s good news: In July, yields on many cash-like investments, which means they're virtually risk-free and liquid, started soaring.

Monday brought a stark warning for Wall Street daredevils: Stocks are still in free fall and bearish sentiment is far from getting exhausted -- especially with hawkish central bankers rattling recession-obsessed markets like this.

Central banks haven't finished tightening and the U.S. Treasury yield curve remains inverted.

The municipal bond market has not been immune to bouts of volatility hitting the markets this year, but there are still pockets of opportunity, according to Franklin Templeton Fixed Income’s Director of Municipal Bonds, Ben Barber.

The U.S. dollar has been on a tear in recent months, bringing it to its highest valuation versus other major developed currencies in more than 35 years.

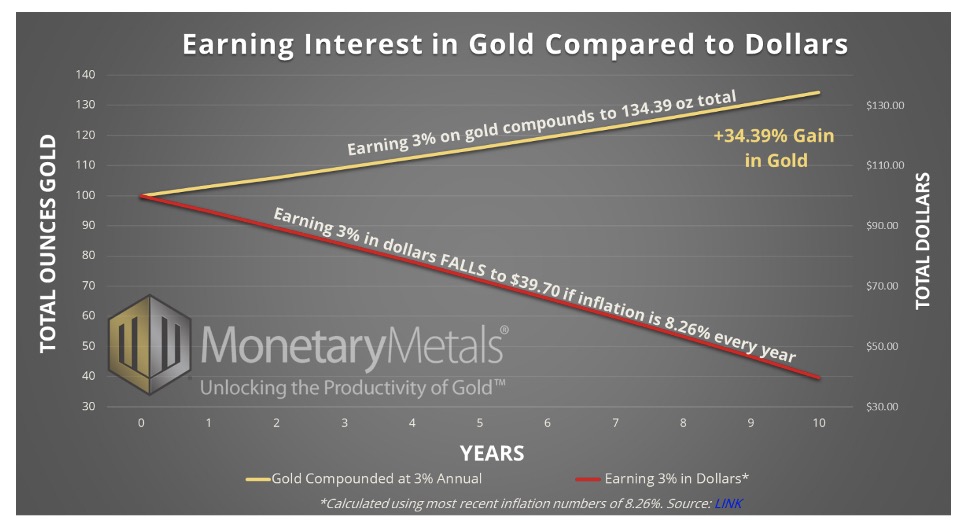

A yield on gold and silver is an attractive alternative to falling yields in dollars or the negative yield with costs of vaulting your precious metals. But are the yields high enough?

While 2022 has been a challenging year for nearly every segment of the capital markets, it comes with a silver lining for income investors: higher yields.