The yield on the benchmark 10-year Treasury is up 70 basis points this year, leading many to question the future direction of interest rates. Let’s look at the underlying causes of this and whether those conditions are likely to persist.

Offices in many of the world’s major cities are struggling to find workers to occupy them. The trend of remote working, triggered by the pandemic, is costing Manhattan “$12 billion a year,” “devastating America’s cities” and “killing London.”

The third quarter was a story of dashed hopes in emerging markets, with the unraveling of some of the most profitable trades in the asset class.

Preferred stocks are what’s known as hybrid securities, meaning the asset class displays both equity and fixed income characteristics.

The Chinese yuan has lost nearly 6% of its value against the U.S. dollar this year, while Shanghai-listed stocks are off about 8% from their 2023 high, set back in May.

U.S. stocks typically post their best returns in the final quarter of the year. Our review of S&P 500 performance since the index’s inception in 1957 found an average Q4 uptick of 4%. (Q1 was next best at an average of 2%.)

We believe a mild U.S. recession is more likely than not in 2024, although a soft-landing scenario cannot be ruled out. A recession is also likely in the UK and eurozone, but appears less likely in Australia.

It was the week that bond markets finally seemed to grasp what central bankers have been warning all year: higher interest rates are here to stay.

Rising real interest rates invariably trigger recessions. The residual impact of pandemic related behaviors delayed the impact in this cycle.

The Federal Reserve’s hawks have been back on the speaking circuit,and markets are abuzz that rates may have to move higher than previously expected. Someone apparently just took out a big short position premised on the chances that rates markets underestimate the odds of an increase in November.

The Bank of Japan met last night to cap off a week of central bank activity.

Despite the Fed’s aggressive monetary tightening and the regional banking crisis earlier this year, the U.S. economy has been surprisingly resilient. Bond yields continue to rise, with long-term Treasuries at their highest level since October 2007.

Gilt prices have been struggling this past year due to surging inflation and interest-rate increases. David Zahn, Franklin Templeton Fixed Income’s Head of European Fixed Income, shares his outlook for the UK economy and why he thinks now is a good time to consider investing in gilts.

Anyone who even casually pays attention to the financial media has likely become familiar with the current state of inflation as well as how high interest rates have risen over the past ~2 years.

The Federal Reserve’s preferred measure of underlying inflation rose at the slowest monthly pace since late 2020, helping to lay the groundwork for policymakers to forgo an interest-rate hike at their next meeting.

Quarterly commentary giving an overview of the markets and the importance of having and implementing a strategy when investing in the markets.

The post-Covid era seems ripe for a Yogi-ism since economists and policymakers have been so wrong about the path of the economy and inflation. Yes, inflation is finally on a downward trend, but it has proven far stickier than the Federal Reserve and most economists predicted and remains above the Fed’s 2% target.

Monetary tightening still continues in the form of quantitative tightening, bringing potential volatility, earnings pressures, and lackluster performance to stock markets.

I’ve been writing financial newsletters for 15 years. I have seen a few cycles. There have been good times and bad times, thrills and spills.

In our latest Quarterly Letter, Ben Inker and John Pease discuss the new economic regime, how investors can prepare for a recession, and the merits of combining high quality and cheap assets in today’s environment.

Few companies have felt the shock from soaring interest rates as much as those owned by private equity. But thanks to surprisingly resilient earnings and their deep-pocketed owners’ talent for financial engineering most are avoiding disaster.

Fed Chair Jerome Powell’s Sept. 20 remarks represented the first time the Fed leadership has sanctioned the idea that the equilibrium policy rate has risen this year; previously, Powell repeatedly avoided taking a view.

Evidence of China's slowdown is appearing in unexpected places.

Many advisors are finding their clients show little interest these days in how the markets are doing.

A financial crisis, following the 5.50% hike in Fed funds and similar increases in all bond yields, is virtually inevitable.

We have been given the mandate to show our capabilities by growing our books of business to “earn the right” to work with clients.

A key measure of how much bond investors are compensated for holding long-term debt turned positive for the first time since June 2021, reflecting steep increases in longer-maturity Treasury yields.

This stock market rally in the first half of 2023 was built on the back of technology stocks, as investors bet on a resilient US consumer and hype surrounding artificial intelligence to keep the shares soaring.

The stock market is buckling under the weight of a simple equation: cash earns more than equities.

The Fed sent a strong signal that interest rates will remain higher for longer, as our Franklin Templeton Fixed Income CIO Sonal Desai has long predicted. The Fed also started to acknowledge that the natural real rate of interest is higher than it thought.

Investors that missed out on this year’s dizzying rally in Nvidia Corp. have an attractive entry point this month.

To judge by recent history, a US government shutdown won’t be a huge event for the bond market. If anything, it could even provide a little short-term relief, since Treasuries usually rally when investors need somewhere to hide.

It might be hard to believe after the crypto winter of 2022, but monetary tightening by global central banks could be supportive of Bitcoin upside.

Today, in a shock decision, the Bank of England (BoE) left its policy rate at 5.25% by the tightest possible majority vote of 5-4. All but one of 65 economists polled by Reuters had predicted that the BoE would raise the rate to 5.5%.

Wednesday’s Federal Reserve (Fed) decision to keep the federal funds rate unchanged wasn’t a surprise at all. Markets, as we argued last week, had predicted that the Fed was going to stay put and that is what it did.

A balanced portfolio needs assets with strong return potential and those that may provide downside mitigation. We believe direct lending can deliver both—a potentially valuable feature, particularly in today’s uncertain market.

Energy and Gold Produces Face Increasing Pressures, Crimping Supply.

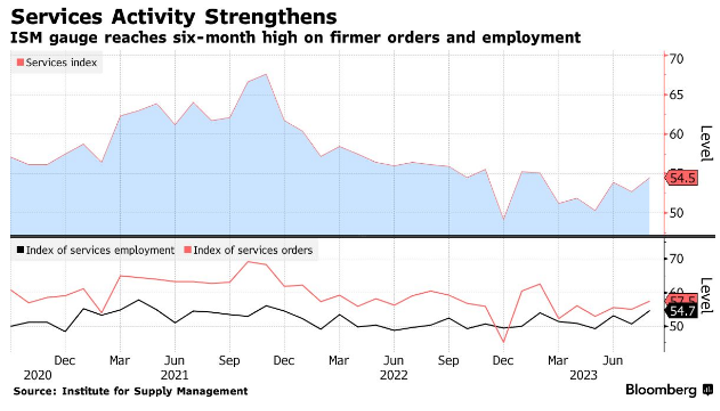

A string of CPI readings heading in the right direction. A labor market and consumer that are still intact. All of the sudden, the recession consensus has given way to a soft landing. Learn what may be in store for the equity market.

The hit TV series “That 70s Show” aired from 1998 to 2006 and focused on six teenage friends living in Wisconsin in the late 70s.

Some seven weeks ago, hedge fund investor Bill Ackman laid out his rationale for shorting long-term US bonds, and I took exception.

Bond investors face the crucial decision of just how much risk to take in Treasuries with 10-year yields at the highest in more than a decade and the Federal Reserve signaling it’s almost done raising rates.

Investment-grade credit is currently offering impressive yields, with relatively less risk than other fixed income sectors, according to Josh Lohmeier of Franklin Templeton Fixed Income. He makes a case for investing in the space today.

I, however, like all Kens, have always had a firm grip on the remote for 100% of the time but I decided to let her have her way just once.

Many of the speakers and attendees were bullish on the physical metal, pointing to gold’s resilience in the face of a very strong U.S. dollar and multiyear-high yields.

The Federal Reserve weighs the data while investors wonder: Is the rate-hike cycle over?

While some stocks may seem expensive, there are areas of opportunity that feature attractive valuations and growth catalysts, according to the Franklin Templeton Investment Solutions team.

Treasury 10-year yields rose above 4.5% for the first time since 2007 as a more hawkish Federal Reserve adds to concern the bonds face a toxic mix of large US fiscal deficits and persistent inflation.

Many view growth stocks, including tech stocks, as sensitive to rising interest rates. Last year confirmed this thesis. That script has been flipped for the better this year as technology ranks as one of the best-performing groups in the S&P 500 despite multiple rate hikes by the Federal Reserve.

Low interest rates can lead people to rationalize all sorts of bad ideas: investing in companies that will never make a profit, financing share buybacks with debt, spending billions on terrible streaming content, to name a few.

A bad week on Wall Street turned dismal Thursday after the relentless surge in Treasury yields sapped demand for risk assets. In the end, US stocks suffered the biggest drop in six months as investors recalibrate for a world where rates sit at levels not seen in a generation.