A balanced portfolio needs assets with strong return potential and those that may provide downside mitigation. We believe direct lending can deliver both—a potentially valuable feature, particularly in today’s uncertain market.

Investors in direct lending are well positioned to capture outsized risk-adjusted returns today, in our view, while benefitting from features that may reduce downside risk. That ability to play both offense and defense is especially appealing in the current macro environment and underscores the importance of private credit in diversified portfolios.

A Good Time to Play Offense in Direct Lending

On the offense side, we believe now is an opportune time for investors to consider adding direct lending exposure, because higher asset yields have boosted the return potential for the asset class.

A series of aggressive Fed rate hikes has resulted in higher market-wide base rates, which in turn have driven a sharp rise in yields for directly originated loans. Senior secured loans, which are typically floating rate, now yield more than 12%, far above the mid-7% yields seen as recently as mid-2022. In senior secured lending strategies that use portfolio financing, potential net returns now stretch into the low double digits to mid teens, notably above investors' long-term return assumptions. Fed tightening has also limited the credit available to firms of all sizes and altered competitive market dynamics in favor of lenders with available capital and conviction to act. Alternative lenders are well positioned to take advantage of these dynamics: traditional syndicated credit markets have been volatile, and alternative lenders have a longer-term capital base and the ability to execute flexible solutions for borrowers.

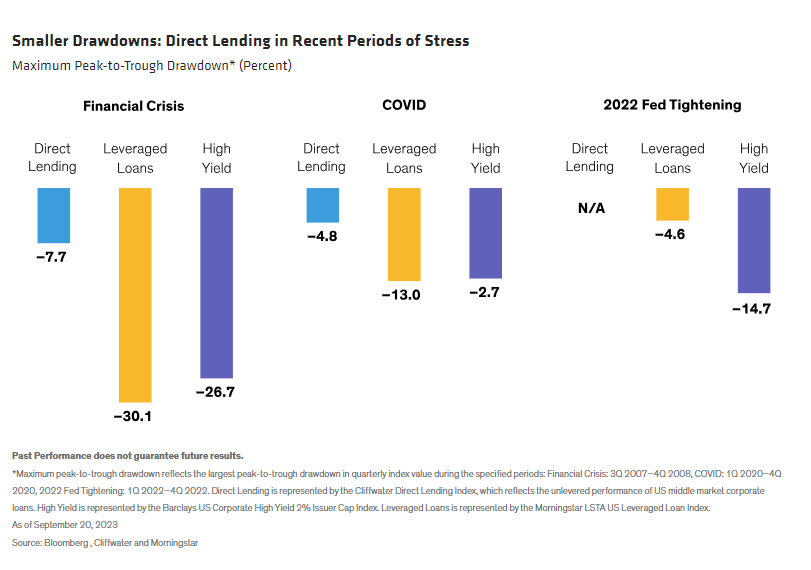

Defense Matters in Direct Lending, Too

In investing, as in sports, playing defense is important, too. Direct lending complements its strong offense potential with downside risk reduction potential. That’s important for investors in today’s macro environment, which presents fundamental pressures from inflation levels not seen for generations and a higher degree of uncertainty.

Over time, direct lending has excelled at providing stability during volatile economic environments or periods of market stress. For instance, drawdowns, which measure the decline from a market peak to its trough, were much more severe for public credit markets during the Global Financial Crisis and the COVID-19 pandemic than for direct lending. Since the Federal Reserve began its current tightening cycle in early 2022, direct lending has continued to generate positive returns. (Display).

The Game Plan for a Strong Defense

What explains the better track record of direct lending in downturns? We think it boils down to important structural advantages. With US interest rates likely to remain elevated for longer, these defensive features may reduce downside risk if the economy slides into a recession and volatility increases in the capital markets.

- A Buy-and-Hold Approach: Direct lending is a buy-and-hold asset class. Most investors access it through fund structures with multiyear commitment periods or other provisions that limit regular liquidity and the need to generate proceeds for redemptions. Also, managers generally don’t actively trade in and out of positions. Instead, they hold them until they’re repaid by borrowers. Because direct loans aren’t typically sold, the asset class is insulated from the sort of technical selling pressure that’s typical during down markets in more traditional, publicly traded assets.

- Senior Status, Significant Equity Cushions: Direct loans are often executed at the top of the capital structure, so they benefit from a large equity cushion below them to absorb potential declines in a borrower’s value. These loans also typically give lenders a priority claim on all of a borrower’s assets, including equity in the underlying business. In other words, a lot must go wrong before lenders incur a loss.

- Other Structural Protections for Lenders: Direct loans give lenders the ability to negotiate certain protective covenants, such as a cap on the amount of leverage or a required minimum level of liquidity. These covenants provide lenders with negotiating leverage to amend the loan terms in their favor if a borrower underperforms. These amendments can improve downside mitigation and may also compensate the lender for incremental risk.

- Strong Relationships: Direct lenders typically lend to companies on their own, or with a small group of like-minded lenders. That’s an important dynamic because it fosters regular communication among lenders, borrowers, and private equity sponsors. More frequent and more robust information flow lets lenders maintain a more current view on borrowers’ performance and outlook, which may help in proactively addressing any forecasted defaults. This degree of connectivity and coordination can be harder to achieve in broadly syndicated loan deals, which can involve 50 to 80 participants, and sometimes even more.

Along with higher loan yields, direct lenders also benefit from more conservative capital structures relative to those in recent years. Structures with lower leverage provide comfort that borrowers will be able to meet debt-service obligations despite the current, higher-rate environment. Meanwhile, enterprise values have been relatively stable, as quality assets remain in high demand, which results in continued healthy equity cushions.

Direct lending’s defensive characteristics may prove valuable if the US economy slips into recession. That potential outcome is still a close call, but we wouldn’t be surprised to see weakening in the labor market and slower overall growth as we move into 2024.

Growing investor demand for private credit has rapidly swelled the ranks of direct lenders. According to Preqin, private credit assets under management, which in addition to direct lending includes other private strategies, including distressed lending and opportunistic credit, now top $812 billion. But the opportunity set for direct lending continues to grow, because direct lenders are now competing directly with investment banks for opportunities to lend to upper mid-market borrowers.

Moreover, not all private lenders are alike. Investors should do their homework to identify managers with strong sourcing capabilities and deep underwriting and portfolio-management expertise—a formula that we think increases the potential for strong performance across diverse economic environments.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams. Views are subject to change over time.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent white papers.

© AllianceBernstein

Read more commentaries by AllianceBernstein