Taking Stock: Q4 2023 Equity Market Outlook

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsKey takeaways

Q4 for the win? 2023 has offered ample fodder for bears and bulls alike, with each quarter nudging toward the latter. Which will prevail in the year’s final months? As Q4 begins, we see:

- A slim output gap arguing for continued prudence

- Wider gaps in profitability and valuation favoring selectivity

- Artificial intelligence (AI) fueling dispersion, disruption and opportunity

Equity market overview and outlook

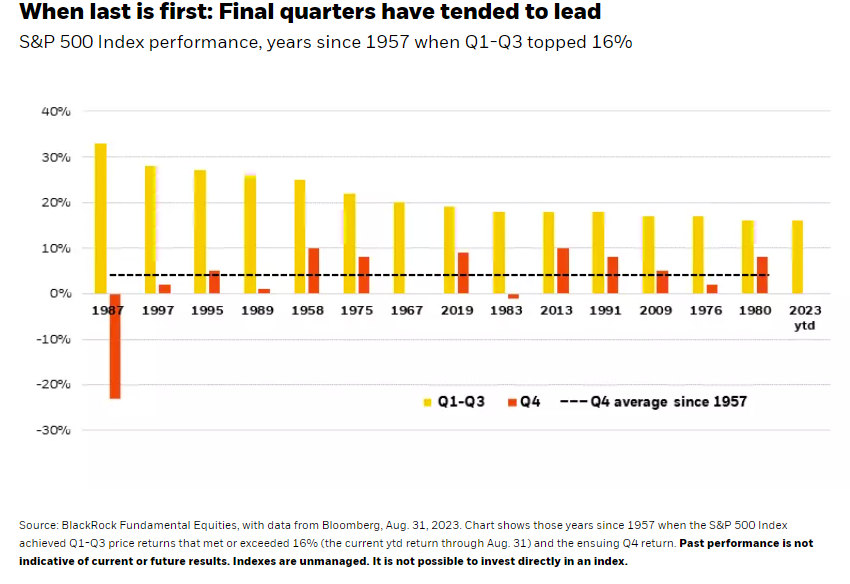

U.S. stocks typically post their best returns in the final quarter of the year. Our review of S&P 500 performance since the index’s inception in 1957 found an average Q4 uptick of 4%. (Q1 was next best at an average 2%.) In years when performance in the first three quarters came in at or above where we sit year-to-date, index moves in the final quarter were positive in all but three instances, with the October 1987 stock market crash making that year an outlier. See chart below.

We are cautiously optimistic for Q4 2023. The market has already defied expectations and the economy is operating on a slim output gap ― meaning all resources are running near full potential. This argues for a continued focus on resilience in equity allocations. Still, because much of the market’s return this year has been driven by a handful of mega-cap stocks in the “tech-plus” sectors, we believe there is opportunity to uncover those next-level stocks that have yet to be fully rewarded for their fundamentals.

Mind the (output) gap

Stock markets turned decidedly more upbeat in July as many strategists adjusted their projections away from recession and toward a “soft landing” scenario for the U.S. economy. While we do not foresee a deep recession, we maintain our view that this is still a late-cycle investing environment and, as a result, a focus on resilience is still warranted in equity portfolios.

The output gap of the U.S. economy, which represents the difference between the economy’s actual versus maximum potential output, is very narrow. The economy is making very efficient use of its existing resources to power the flow of goods and services, with little room to do more and take off running. A key variable is the labor picture, which is quite tight. The unemployment rate stood at just 3.8% as of August. Absent a burst of productivity, the U.S. lacks sufficient additional workers to increase the economy’s output beyond current levels without risking inflation.

GDP figures have held in, inflation readings are coming down and the economy has so far managed to avoid a recession. Yet we still see potential for waning excess consumer savings and the lagged effects of the Fed’s rate-hiking campaign to pinch economic growth and make it harder for companies to grow earnings in the near term.

Late-cycle playbook

Against this backdrop, we believe it is prudent to stick with the late-cycle playbook in equities, as the economy has yet to embark on a new cycle of post-recessionary growth. This implies diversifying risk exposures and focusing on companies with solid balance sheets and durable business models. The key, and the complication after the market’s strong run year-to-date, is to find them at attractive valuations.

The good news is that the very narrow market that had prevailed in the first half, with the seven largest stocks dominating S&P 500 return, has started to broaden ― a healthy sign for the market and a good environment for stock picking. Year-to-date, some of the weakest performers with the most compressed valuations have been low-volatility, low-beta stocks.

"We see smaller reward in making bold calls on the big picture and much greater potential from making good calls on individual stocks."

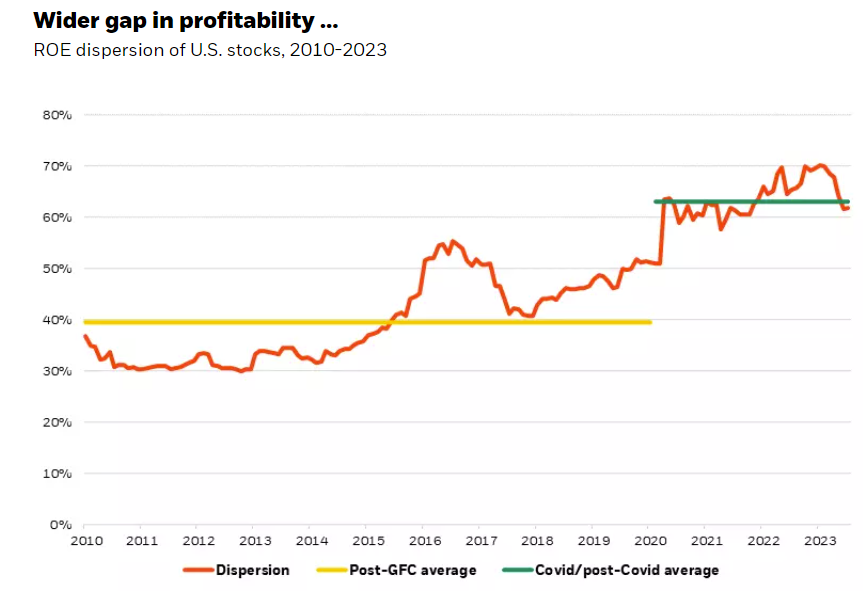

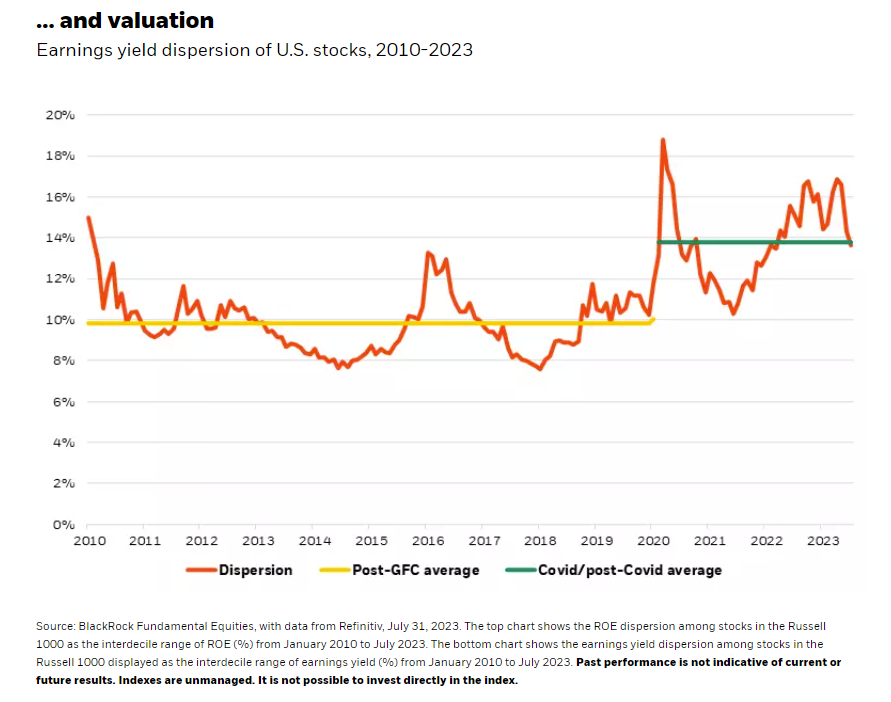

As noted in Equity investing for a new era: The return of alpha, we also observe a trend toward increased market dispersion. This is evident in returns ― a larger gap between top and bottom performers ― but even more so in the return on equity (ROE) and valuations across individual stocks, a phenomenon not isolated to the U.S. The charts below show the uptick in dispersion since the period of moderation (low rates, inflation and volatility) after the Global Financial Crisis (GFC) and the new investment regime in formation since the Covid crisis. Skilled stock pickers can capitalize on these growing gaps in seeking to identify and populate portfolios with shares of companies that demonstrate the fundamental wherewithal to deliver growing earnings across time.

Critical observations on generative AI

With anticipation around generative artificial intelligence (genAI) helping to power year-to-date stock market gains, this quarter we explore AI’s role in shaping tomorrow’s opportunity set. We offer a 3-by-3 analysis of reasons for excitement and awareness in our full Q4 commentary

The bottom line: We see generative AI on an improvement curve with prospects to transform businesses around the world, much like the internet has over the last quarter of a century. Yet it is precisely because genAI is new, exciting and evolving that we cannot take a static approach to the investment thesis.

Constant monitoring is required to assess whether expectations are aligned to the financial and fundamental realities. As fundamental-based stock pickers, we are continually fact-checking the investment case as the cycle around generative AI advances from peak expectations to enlightenment and productivity. The genAI story has only just begun and, we expect, will be written for many years to come.

This material is provided for educational purposes only and is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of September 2023, and may change as subsequent conditions vary. The information and opinions contained in this material are derived from proprietary and nonproprietary sources deemed by BlackRock to be reliable, are not necessarily all-inclusive and are not guaranteed as to accuracy. Past performance is no guarantee of future results. There is no guarantee that any forecasts made will come to pass. Reliance upon information in this material is at the sole discretion of the reader. The material was prepared without regard to specific objectives, financial situation or needs of any investor.

This material may contain “forward-looking” information that is not purely historical in nature. Such information may include, among other things, projections, forecasts, estimates of yields or returns, and proposed or expected portfolio composition. Moreover, where certain historical performance information of other investment vehicles or composite accounts managed by BlackRock, Inc. and/or its subsidiaries (together, “BlackRock”) has been included in this material, such performance information is presented by way of example only. No representation is made that the performance presented will be achieved, or that every assumption made in achieving, calculating or presenting either the forward-looking information or the historical performance information herein has been considered or stated in preparing this material. Any changes to assumptions that may have been made in preparing this material could have a material impact on the investment returns that are presented herein by way of example.

Investing involves risk. Equities may decline in value due to both real and perceived general market, economic, and industry conditions. Diversification does not ensure profits or protect against loss. Investments in technology industries may be affected by limited product lines, markets or financial resources. Technology industries are rapidly changing and stocks of these companies may be more volatile than the stock market in general.

You should consider the investment objectives, risks, charges and expenses of any BlackRock mutual fund carefully before investing. The prospectus and, if available, the summary prospectus contain this and other information about the fund and are available, along with information on other BlackRock funds, by calling 800-882-0052 or from your financial professional. The prospectus should be read carefully before investing.

Prepared by BlackRock Investments, LLC, member FINRA

Not FDIC Insured | May Lose Value | No Bank Guarantee

© 2023 BlackRock, Inc. or its affiliates. All Rights Reserved. BLACKROCK is a trademark of BlackRock, Inc. or its affiliates. All other trademarks are those of their respective owners.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our podcasts.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All