“It's difficult to make predictions, especially about the future.”

This quote has been attributed to everyone from quantum physicist and Nobel laureate Niels Bohr to Yogi Berra. I like to think it was Yogi Berra, because the old Yankee catcher had a knack for making nonsensical quips that were nevertheless full of wisdom.

The post-Covid era seems ripe for a Yogi-ism since economists and policymakers have been so wrong about the path of the economy and inflation. Yes, inflation is finally on a downward trend, but it has proven far stickier than the Federal Reserve and most economists predicted and remains above the Fed’s 2% target.

Headline CPI for August came in at 3.7%, up from 3.2% in July largely due to higher oil prices. Core inflation (excluding food and energy) fell month over month but is still above 4%. The Fed is making progress, but I can still hear Yogi’s voice in my head saying, “a nickel ain’t worth a dime anymore.” And don’t get me started on housing prices.

Almost there … but higher for longer?

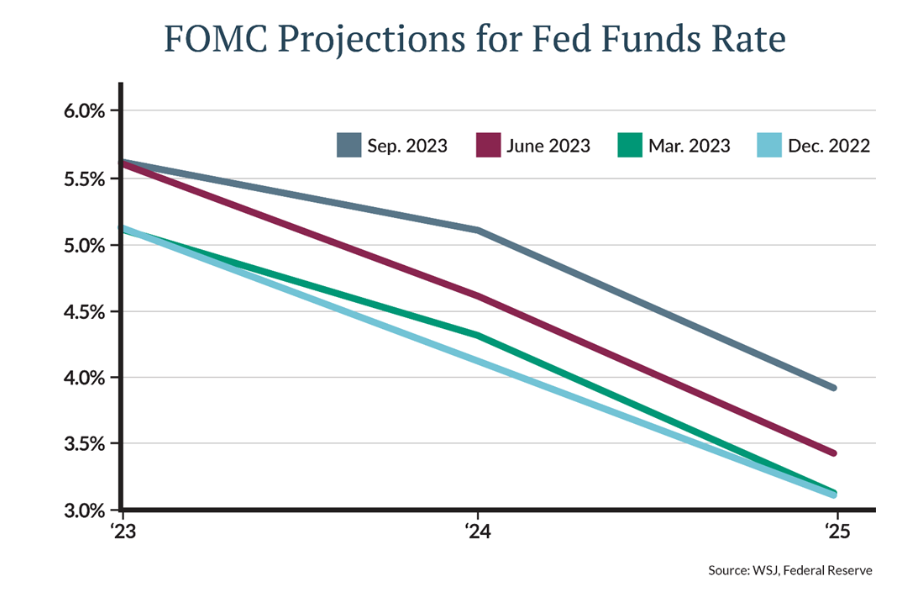

How much work the Fed has left to reach its inflation mandate is the central question now. Fed watchers are anxiously asking, “Are we there yet?” hoping that the Fed Funds rate may not need to rise above the current range of 5.25%-5.50% to get the job done. If the Fed’s predictions are to be believed, the answer is “almost.” Projections released after its Federal Open Market Committee (FOMC) meeting last week showed 12 of 19 Fed officials favoring raising rates one more time this year before beginning to cut rates in 2024.

But Fed Chair Powell’s rhetoric last week was measured. The Wall Street Journal noted his use of the word “careful” six times during the post-meeting news conference. That may explain why the FOMC’s projections in 2024 and 2025 reflect a “higher for longer” theme when compared to its projections at the last three meetings. Members expect to cut rates by far less next year than they thought earlier. They now forecast a federal-funds rate of 5.125% at the end of next year and 3.9% by the end of 2025. [Figure 1].

This “higher for longer” theme has resulted in long-term bond yields approaching 2007 levels in recent days, trimming some of the gains that bonds had enjoyed this year. Bond prices fall as interest rates rise.

The Fed will be carefully watching to see if the economic data begins to roll over in response to policy that can finally be considered restrictive. For our part, we are not trying to predict the future but are instead taking advantage of the opportunity set before us while positioning ourselves to benefit from both higher rates and a future Fed pivot.

Favorable Return Profile in Fixed Income Today

The great thing about today’s higher yields is that they offer fixed income investors a favorable return profile. To take an oversimplified example, let’s consider the impact of interest rate changes on a 5-year Treasury bond paying a 5% interest rate. If comparable interest rates rise an additional 1% from today’s levels, bond math dictates that the 5-year bond’s price will decline by a little less than 5%. But because the bond pays 5% in interest, the investor can expect a total return slightly above breakeven.

In contrast, if comparable interest rates fall by 1%, bond math tells us that the price of the 5-year Treasury will rise by about 5% even while we collect our 5% coupon payments, for a total return near 10%. Here’s the key point: today’s higher yields provide an income cushion to offset the price impact of higher interest rates while offering compelling upside should rates fall.

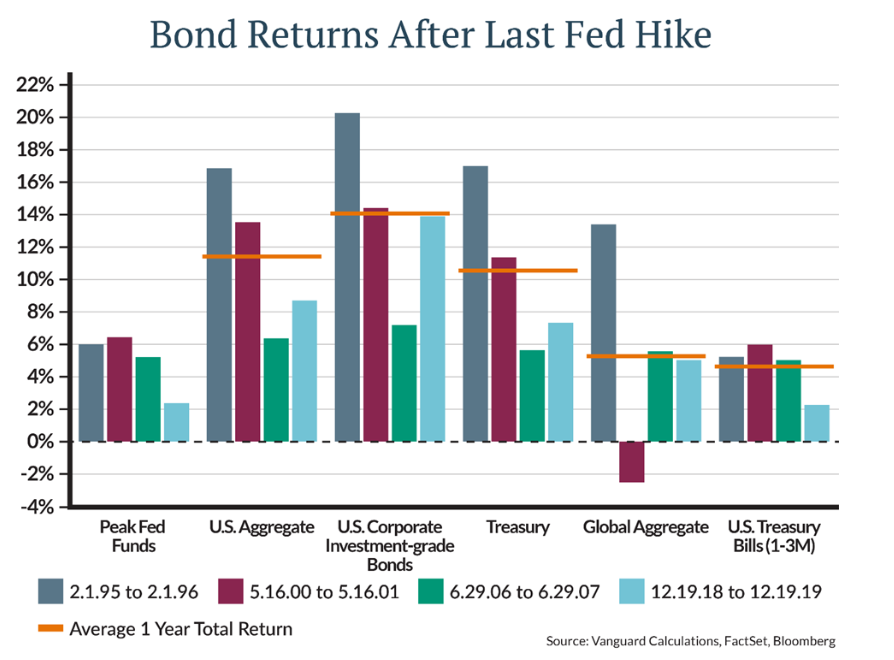

Looking farther into the future, we believe fixed income investors have history on their side. Our partners at Vanguard have looked at bond returns over the one-year period following the last rate hike over each of the last four interest rate cycles [Figure 2]. You can see that in each case, intermediate-term Treasury bonds and investment grade corporate bonds posted strong returns that exceeded cash (represented by short-term T-Bills).

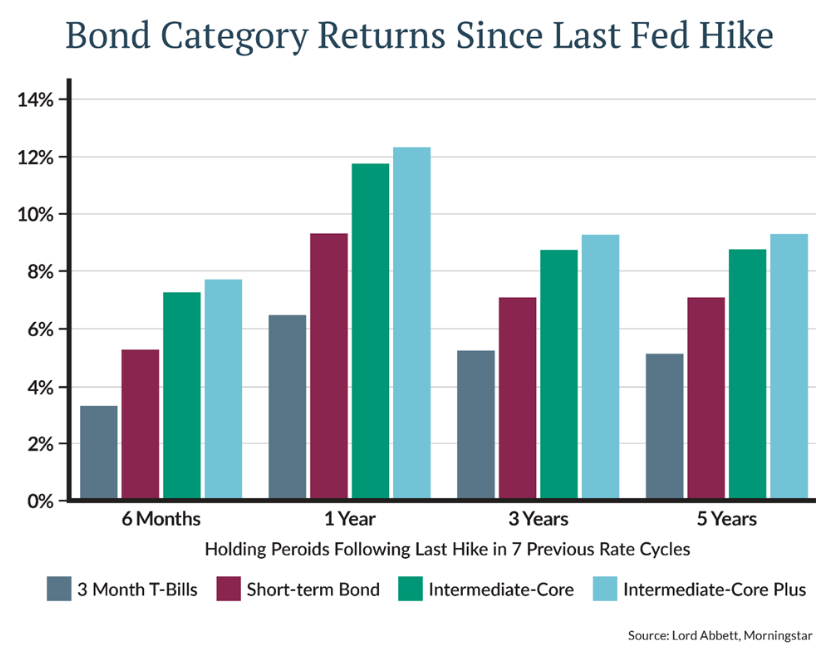

Mutual Fund provider Lord Abbett did a similar analysis comparing bond mutual fund performance after the last Fed rate hike. Its research shows that intermediate “core” and “core plus” fixed income mutual funds strategies outperformed cash over multiple time horizons after the Fed Funds rate peaked.

Credit quality up, average maturity longer

Johnson Financial Group offers both “core” and “core plus” strategies to help clients take advantage of the current opportunity set. Core strategies stick to treasuries, mortgage-backed securities, and investment grade corporate bonds, while core plus strategies have the flexibility to add to other sectors such as high yield and emerging market bonds when conditions warrant. At this point in the economic cycle, we have sought to increase credit quality in both strategies, while extending our average maturity to lock in today’s high yields for longer.

Whether rates are indeed peaking, or the Fed has more wood to chop, we think it’s an exciting time to be investing in bonds. Yogi might quip, “the future ain’t what it used to be.” For bond investors, we agree. It will be better.

Disclaimer

This information is for educational and illustrative purposes only and should not be used or construed as financial advice, an offer to sell, a solicitation, an offer to buy or a recommendation for any security. Opinions expressed herein are as of the date of this report and do not necessarily represent the views of Johnson Financial Group and/or its affiliates. Johnson Financial Group and/or its affiliates may issue reports or have opinions that are inconsistent with this report. Johnson Financial Group and/or its affiliates do not warrant the accuracy or completeness of information contained herein. Such information is subject to change without notice and is not intended to influence your investment decisions. Johnson Financial Group and/or its affiliates do not provide legal or tax advice to clients. You should review your particular circumstances with your independent legal and tax advisors. Whether any planned tax result is realized by you depends on the specific facts of your own situation at the time your taxes are prepared. Past performance is no guarantee of future results. All performance data, while deemed obtained from reliable sources, are not guaranteed for accuracy. Not for use as a primary basis of investment decisions. Not to be construed to meet the needs of any particular investor. Asset allocation and diversification do not assure or guarantee better performance and cannot eliminate the risk of investment losses. Certain investments, like real estate, equity investments and fixed income securities, carry a certain degree of risk and may not be suitable for all investors. An investor could lose all or a substantial amount of his or her investment. Johnson Financial Group is the parent company of Johnson Bank and Johnson Wealth Inc. NOT FDIC INSURED * NO BANK GUARANTEE * MAY LOSE VALUE

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent white papers.

© Johnson Financial Group

Read more commentaries by Johnson Financial Group